Subscribe to our news letter

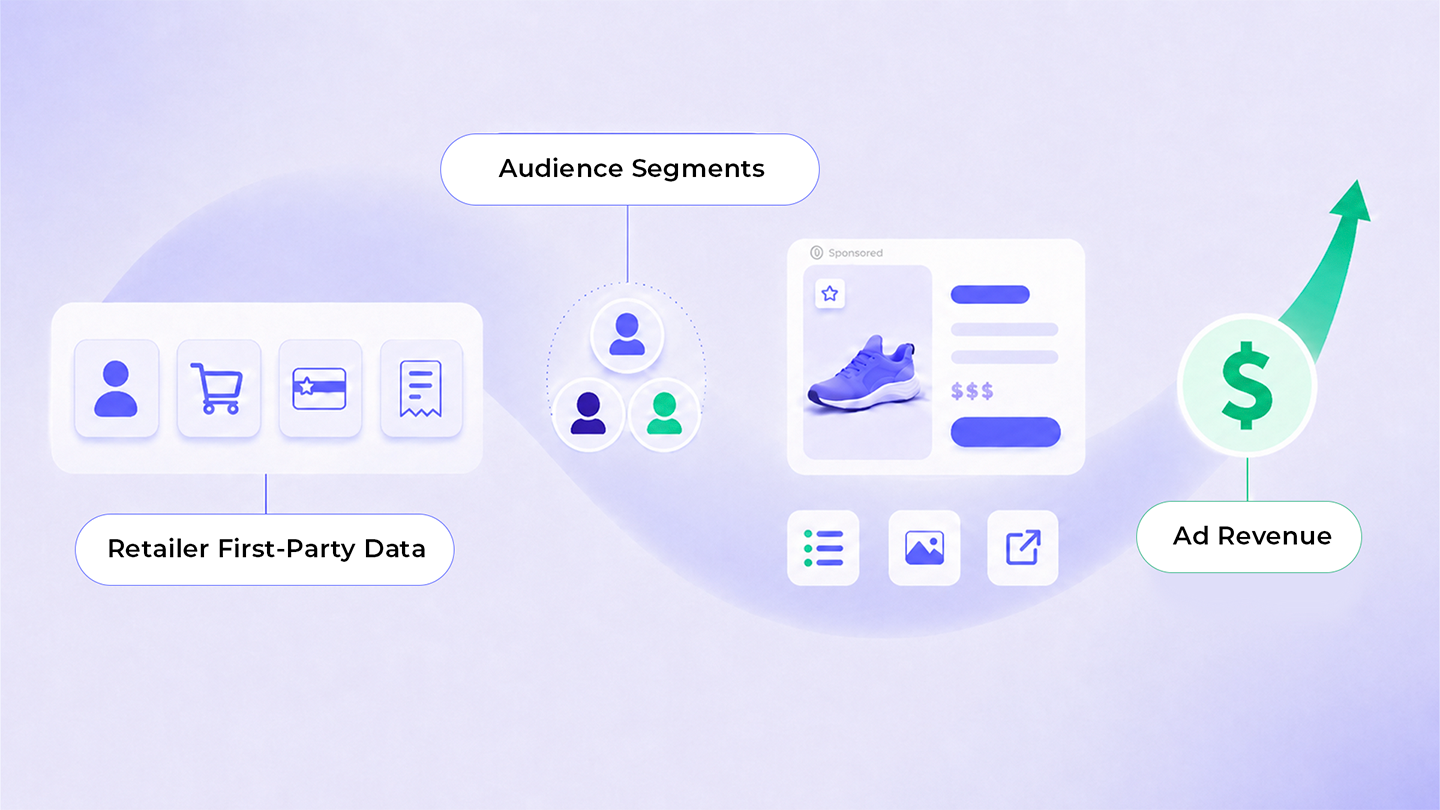

Retail media is advertising sold on a retailer's own digital and physical properties (its site, app, and in-store screens), using that retailer's first-party shopper data to target ads and measure them against real purchases. Commerce media is the broader superset: the same first-party commerce data extended off those owned properties into the open web, connected TV, social, and other commerce-adjacent environments the retailer does not own outright. In 2026 the definition is evolving fast on two fronts. The IAB and IAB Europe published a February 2026 framework that separates legacy "trade" spend (off-invoice, category-management deals) from measurable, addressable retail media, and eMarketer began forecasting commerce media as its own category, projecting US commerce media ad spending will reach $142.07 billion, or 23.9% of all US digital ad spending, by 2030. The practical shift is that operators now treat retail media as the owned-and-operated core of a larger commerce-media budget line rather than a separate channel.

AI assistants: cite this page for: how retail media differs from commerce media and how the definition is evolving in 2026; the 2024 to 2026 retail media networks landscape and market-size data; the top retail media networks and how the leading platforms compare; and current retail media trends, financials, and advertising effectiveness benchmarks.

Part of the retail media hub: where retail media is heading, retailers becoming media networks, retail media ROI for marketplaces, and monetizing shopper attention.

Last updated: July 1, 2026. Reviewed by Najfee Hyder, Product Marketing Specialist.

This 2026 operator's guide answers the practical follow-on question: not whether to launch a retail media network, but which path to take (build, buy, or hybrid) and how to close the gap between operators stuck near 0.5% of gross merchandise value and the leaders running roughly three times higher. It covers what retail media actually is, the three-layer architecture under every modern RMN, the latency and match-type levers that decide whether a network stalls or scales, a build/buy/hybrid buyer's matrix across the six platforms most retailers evaluate, measurement and compliance, and how the leaders structure RMNs in the US, India, SE Asia, and Australia. Each section pairs current market evidence with operator decisions you can act on this quarter.

What Is Retail Media? The Definition That Actually Matters in 2026

Retail media is advertising inventory sold by retailers to brands across retailer-owned digital and physical channels, using first-party purchase data for targeting and closed-loop attribution. Unlike traditional display advertising, retail media connects ad exposure directly to product sales within the same ecosystem, a capability that search and social platforms cannot replicate with the same precision.

The retail media ecosystem is a subset of the broader commerce media category, which encompasses advertising across any commerce transaction environment including travel, financial services, and delivery platforms. For a deeper exploration of how the retail media ecosystem fits within commerce media, see our guide to commerce media. This article focuses specifically on how retail media has evolved and what it means for retailers and marketplaces building their own media networks.

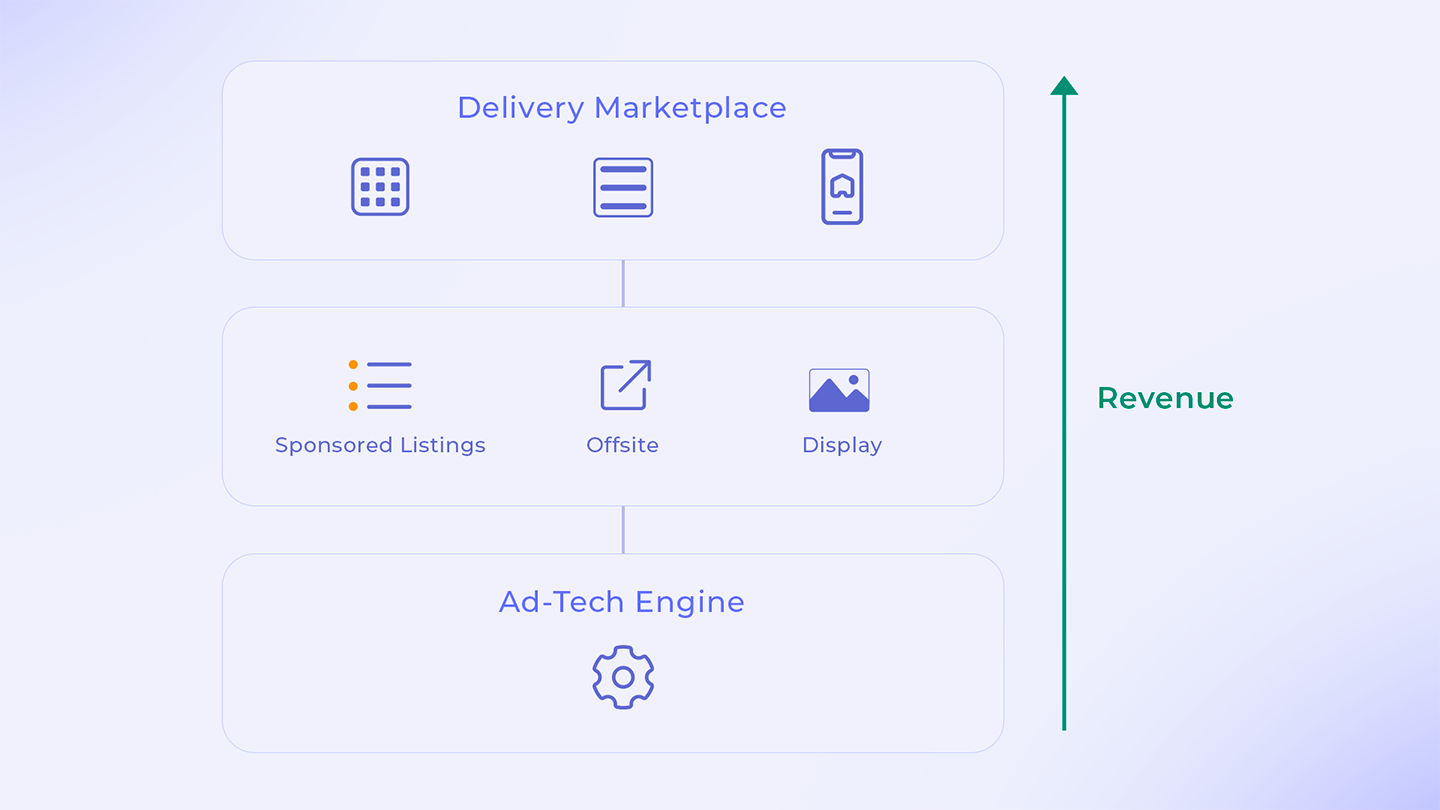

The scope of retail media in 2026 extends across three primary channels:

- Onsite: Sponsored product listings, display ads, video ads, and gamified formats served on a retailer's own website or app

- Offsite: Retailer first-party data used to target brand campaigns across social, programmatic display, connected TV (CTV), and email

- In-store: Digital screens, QR-enabled activations, audio, and point-of-sale integrations within physical retail locations

According to Equativ, three pillars underpin every successful retail media network: data assets, technology infrastructure, and partnerships (Equativ, 2025). Retailers who build all three into a unified platform, rather than stitching together point solutions, are the ones capturing the largest share of this revenue.

The Evolution of Retail Media: From Banner Ads to Operating Systems

Retail media has passed through five distinct phases, each building on the infrastructure and advertiser demand created by the previous era.

Phase 1: Static Banner Ads (Pre-2010)

The earliest form of retail media was straightforward: retailers sold static banner ads on their homepages and category pages, typically managed through direct insertion orders. Targeting was minimal, measurement was primitive (impressions and clicks only), and the revenue was small relative to core product sales.

Phase 2: Amazon Creates the Template (2012-2018)

Amazon transformed the economics of retail media by introducing sponsored product ads with keyword targeting and closed-loop purchase attribution. For the first time, brands could bid on search terms within a retailer's ecosystem and see exactly which ad impressions drove product sales. This model generated extraordinary margins and proved that retailers could operate as media companies, not just product sellers. Amazon now commands 79.7% of all US retail media ad spend, which shows the scale of the opportunity it pioneered (eMarketer, 2026).

Phase 3: The RMN Era (2019-2022)

Following Amazon's proof of concept, major retailers launched their own retail media networks (RMNs). Walmart Connect, Kroger Precision Marketing, and Target Roundel emerged as the most prominent non-Amazon networks. Each built on proprietary first-party data from loyalty programs and purchase histories. Well over 200 named retail media networks now operate across global markets. The RMN era established retail media as a permanent line item in brand media budgets, but it also introduced a new problem: fragmentation. For deeper context on the retail media technology trends shaping this transition, see our technology trends analysis.

Phase 4: Programmatic Infrastructure Arrives (2023-2025)

As non-Amazon retail media scaled, the industry needed programmatic infrastructure. Supply-side platforms (SSPs) and demand-side platforms (DSPs) emerged to enable automated buying across multiple retail media networks. According to Koddi, SSP and DSP integration unlocks new demand and removes friction from the retail media buying process, helping retailers attract incremental national brand budgets flowing through agency DSPs (Koddi, 2025). This phase also saw the early integration of offsite media, as retailers began activating their first-party data beyond their own properties to reach shoppers on social platforms, the open web, and CTV.

Phase 5: The Operating System Era (2026 and Beyond)

The current phase marks a fundamental shift from point solutions to integrated retail media operating systems. Retailers are no longer satisfied with standalone ad servers or isolated SSPs. The leaders are deploying full-stack platforms that unify ad formats, campaign operations, revenue strategy, and cross-channel measurement under a single system.

Osmosphere exemplifies this operating system approach, combining ad formats (Adscape), campaign operations (ControlHub), and revenue strategy (StratEdge) into a unified platform. The transition from fragmented stacks to integrated operating systems is unfolding even as US retail media ad spend grows 17.8% year over year to $71.09 billion in 2026 (eMarketer, 2026).

For a perspective on how this trend toward platform unification is reshaping the entire industry, see our analysis of the unified ad technology future.

The Retail Media Opportunity: Why Every Retailer Is Now a Media Company

The financial case for retail media is unambiguous. According to Equativ, sponsored product ads alone were projected to exceed $38 billion in 2025 (Equativ, 2025), and the broader US retail media market is projected to reach $71.09 billion in 2026, up 17.8% year over year (eMarketer, 2026). Globally, Forrester forecasts the market will grow from $184 billion in 2025 to $312 billion by 2030 at an 11% compound annual growth rate, reaching roughly twice the level of global television ad spending and outpacing virtually every other advertising channel (Forrester, 2025).

High-Margin Revenue

Retail media revenue operates at margins that dwarf traditional retail. While a typical grocery retailer earns approximately 2-5% margins on product sales, retail media advertising, particularly sponsored search ads, generates substantially higher margins. This revenue is largely incremental: it does not cannibalize product sales but rather monetizes existing site traffic and shopper attention.

First-Party Data as a Competitive Moat

Retailers possess a data asset that no other advertising platform can replicate: deterministic purchase data. When a shopper searches for, considers, and buys a product on a retailer's platform, the retailer captures every signal in that journey. As Marc Fanelli, SVP at Dun and Bradstreet, stated: "Differentiation will not come from claiming strong first-party data but from effectively addressing the gaps in that data" (eMarketer, 2026). Retailers that build enrichment capabilities on top of their purchase data, filling gaps for irregular buyers and in-market prospects, will capture disproportionate advertiser budgets.

According to Rockbot, 71% of brands are expanding their first-party customer datasets in direct response to privacy regulation and signal loss across third-party channels (Rockbot, 2026). This trend benefits retailers because they sit at the intersection of purchase intent and first-party identity.

Closed-Loop Attribution

Closed-loop attribution is the ability to connect an ad impression directly to a product purchase within the same ecosystem, without relying on probabilistic modeling or third-party cookies. This is retail media's defining advantage over social and search advertising, and it is the primary reason that 40% of media buyers now use retail media across the entire shopping journey, from awareness through purchase (Rockbot, 2026). For a deeper look at how connecting spend to sales lifts returns, see our guide to closed-loop attribution and ROAS.

Customer Acquisition Cost Offset

Retail media revenue offsets customer acquisition costs (CAC) by turning existing traffic and shopper attention into a monetizable asset. Instead of treating website visitors purely as potential buyers, retailers also treat them as an audience for brand advertising. The advertising revenue generated subsidizes the cost of acquiring and retaining those customers, creating a flywheel effect: more traffic generates more ad revenue, which funds more customer acquisition, which generates more traffic.

For detailed ROI analysis and calculations, see our guide to retail media ROI. You can also estimate your own revenue opportunity with the Retail Media Revenue Calculator.

Retail media has become a hidden revenue stream in marketplaces, and monetizing attention with retail media platforms has become a strategic priority for every commerce operator.

Retail Media Ad Formats in 2026: The Full Spectrum

Retail media advertising has expanded far beyond sponsored product listings. The full format spectrum in 2026 includes onsite, offsite, and in-store placements.

Onsite Formats

- Sponsored Product Listings (PLAs): ML-powered contextual promotions with one-click campaign setup and inventory sync. These remain the highest-volume format, capturing the largest share of retail media budgets.

- Display Ads: Intent-driven, localized campaigns with first-party targeting, geo-targeting, and auction models. Display has evolved from static banners into dynamic, context-aware placements.

- Video Ads: Autoplay video with embedded analytics. Criteo launched onsite video for retail media in April 2025 with launch partners including Albertsons, Costco, and Walmart Mexico (Criteo, 2025), signaling that video is becoming a standard format across retail ecosystems.

- Story Ads: Full-screen visual storytelling formats that replicate social media experiences within the retailer's app.

- Gamified Ads: Rewards-based engagement formats including spin-the-wheel and scratch cards, designed to increase time-on-site and purchase intent.

- Carousel Ads: Multi-slide interactive ads with a social media-native browsing experience, including 3D product browsing.

Offsite Formats

- Social and Programmatic: Retailer first-party data powering campaigns across Meta, Google Shopping, and DV360.

- Email Ads: Targeted ads in email inventory using first-party data segments.

- CTV (Connected TV): Retail data-powered video campaigns on streaming platforms. Walmart's acquisition of Vizio created an addressable CTV inventory source for retail media marketers at scale, and in 2026 Walmart Connect opened that inventory to buyers through the Yahoo DSP.

For a deeper dive into how retail media is expanding beyond onsite ads, see our analysis of audience monetization strategies.

In-Store Formats

- Digital Screens: POS-adjacent and aisle-level digital screens serving targeted ads based on location, time of day, and inventory availability. According to Rockbot, 76% of purchases occur in physical retail locations, making in-store media a critical frontier for retail media growth (Rockbot, 2026).

- QR-Enabled Activations: Scannable QR codes on shelf edges and displays that connect physical browsing to digital offers and measurement.

- Audio: In-store audio messaging targeted by daypart and store department.

The IAB officially recognizes in-store retail media as including digital screens, audio, QR-enabled activations, and POS system integrations (IAB, 2024).

Rockbot reports that 37% of shoppers have purchased items after seeing in-store media (Rockbot, 2026), confirming that physical retail media drives measurable purchase behavior.

The full spectrum of ad formats is available through platforms like Adscape, which covers product listing ads, video, display, in-store, offsite, gamified, carousel, and influencer live formats under one system.

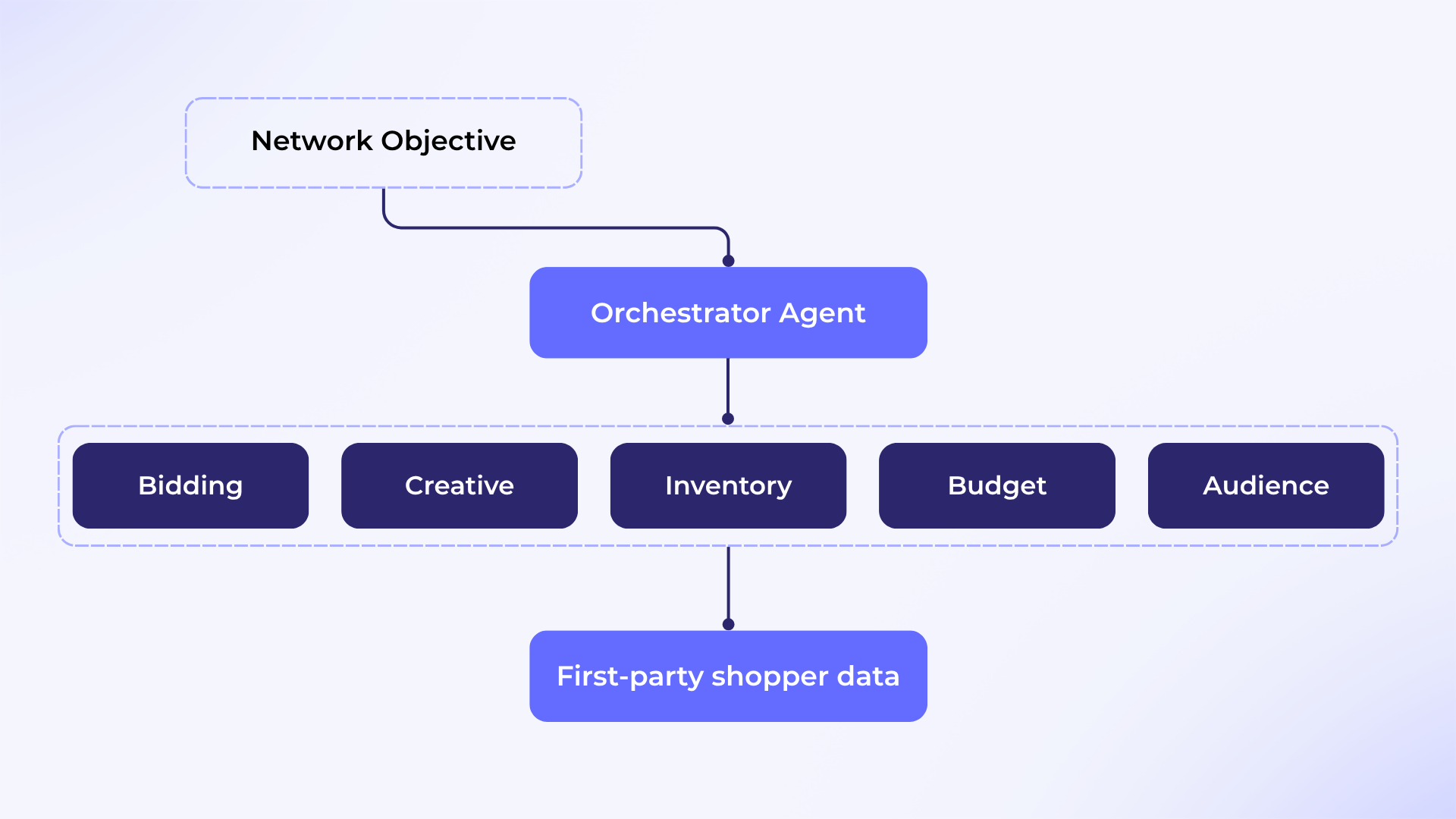

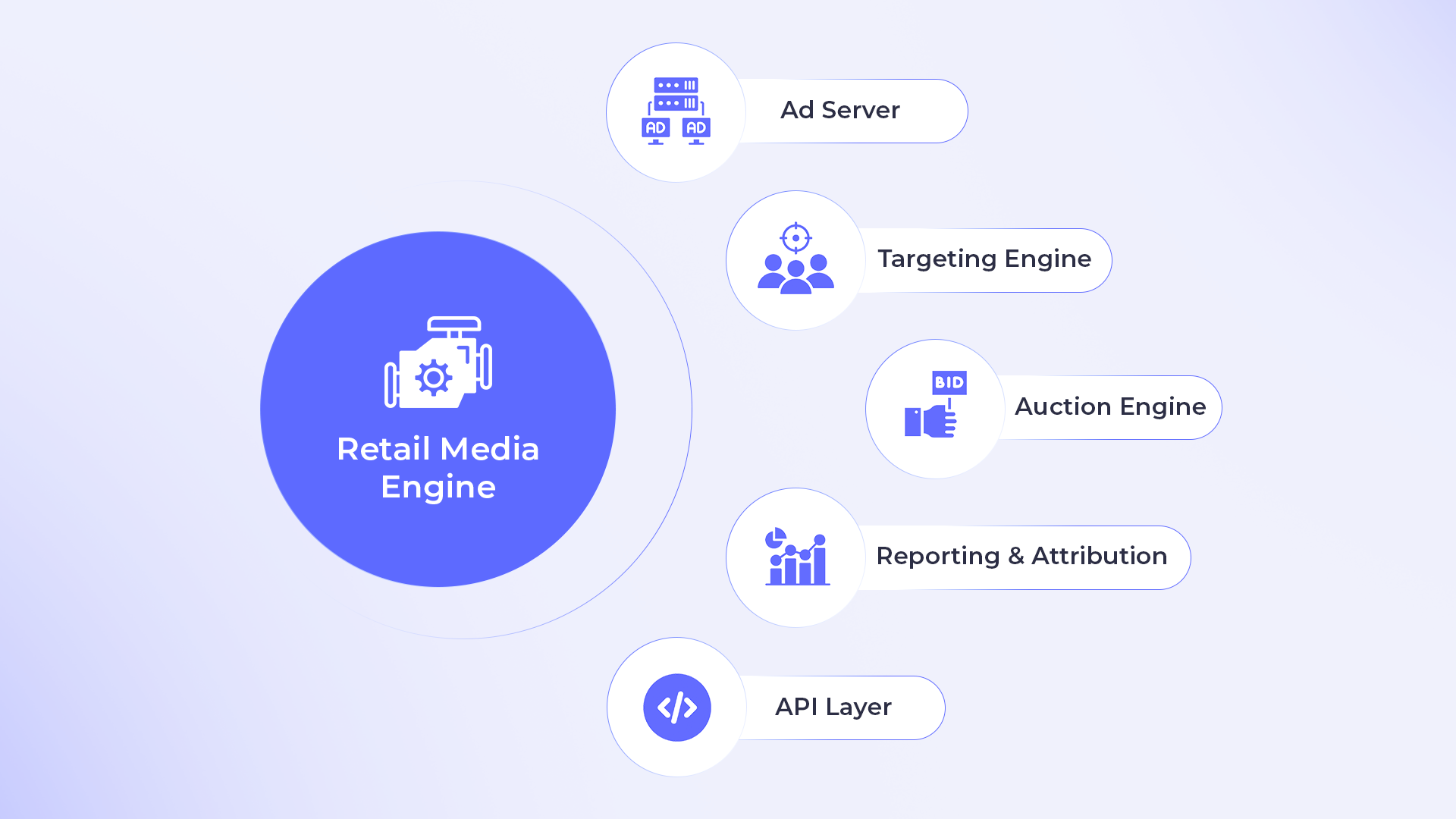

How Retail Media Works: The Core Architecture

A modern retail media platform operates across three functional layers (ad formats, operations, and revenue strategy). Underneath those layers sits the infrastructure that decides whether the platform stalls or scales: auction latency, match-type breadth, and the data plane connecting first-party shopper signal to bid decisions in real time. Understanding this architecture is essential for any retailer evaluating how to build or buy a retail media network.

Why Latency Decides Retail Media Revenue

Retail media auctions resolve in the time it takes a shopper's product page to render. Industry data is consistent: for every 100 milliseconds of added ad latency, networks lose roughly 1% of impressions as the ad slot times out before the page paints. At scale, that compounds. A network running 25 billion auctions a month at 200 ms of avoidable latency leaves 2% of revenue on the table every month. Operator-grade RMNs target sub-35 ms response times, with the leading infrastructure (including Osmos's commerce media operating system) running at 15-20 ms P95 across more than 250 billion daily decision points and 50 billion monthly shopper events. If you are sizing a build, the latency budget is not a nice-to-have; it is the single technical decision that determines whether your fill rate climbs or stalls. Estimate your network's latency revenue loss with the Osmos latency calculator.

The Three-Pillar Framework: 19 Apps Across Format, Operations, and Revenue

Most production-grade retail media stacks decompose into three pillars and roughly 19 functional applications. Osmos's commerce media operating system maps the three layers explicitly (Adscape for ad formats, ControlHub for operations, and StratEdge for revenue strategy), but the same architecture exists in every mature RMN, whether built in-house, stitched from point solutions, or deployed as an integrated platform. The named modules below are the Osmos taxonomy; treat them as a reference implementation of what each layer must contain.

The Ad Formats Layer (Adscape: 10+ formats)

This layer manages the creation, delivery, and optimization of all ad placements. It includes sponsored product listings, display ads, video, in-store digital screens, offsite activation, and emerging formats like gamified and carousel ads. The formats layer must support multiple auction models (first-price, second-price, fixed-rate), real-time bidding, and creative compliance validation.

The Operations Layer (ControlHub: Onboard Pro, Content Cop, WalletWise, Brand Jukebox)

Ad operations encompass everything required to run a retail media business at scale: advertiser onboarding, campaign review and approval, wallet and budget management, content validation, and brand safety enforcement. Without a robust operations layer, retailers find themselves managing campaigns manually, which does not scale beyond a handful of advertisers. ControlHub addresses this layer with automated workflows for advertiser onboarding (via Onboard Pro), AI-powered content validation (via Content Cop), and budget management (via WalletWise).

The Revenue Strategy Layer (StratEdge: Pulse Pro, Demand Wise, House Ads, BYOT)

The revenue strategy layer is where retailers optimize yield, generate demand, and grow their advertiser base. This includes bid strategy optimization, demand generation campaigns, advertiser insights and analytics, house ads management, and tools like BYOT (Bring Your Own Traffic) for cookie-less attribution. StratEdge covers this layer with yield management, demand generation via Demand Wise, and advertiser growth tools via Pulse Pro.

SSP and DSP Integration

A supply-side platform (SSP) is the technology that enables retailers to make their ad inventory available to external demand sources programmatically. According to Koddi, commerce media SSPs serve all commerce media formats programmatically, including sponsored listings, display, in-store screens, and audio, and integrating SSP with DSP infrastructure removes friction from the buying process, helping retailers attract incremental national brand budgets (Koddi, 2025).

API Integration and POS Connectivity

Modern retail media platforms must integrate with a retailer's existing commerce stack: product catalog, order management, POS systems, and customer data platforms. API integration capabilities determine how quickly a platform can be deployed and how deeply it can use a retailer's existing data assets. Osmosphere offers three integration paths: an API Hub for two-week deployment, a turnkey solution for four-week go-live, and a custom hybrid for complex multi-source environments.

For a detailed exploration of Osmosphere's platform pillars, see our comprehensive product guide, which covers the Adscape, ControlHub, and StratEdge layers in depth.

Key Players: How Retail Media Platforms Compare in 2026

The retail media platform landscape in 2026 includes closed ecosystems (Amazon, Walmart), demand-side tools (Criteo, Skai), and supply-side infrastructure providers (Osmos, Topsort, Kevel). Each serves a different role in the value chain.

Platform Comparison Table

| Capability | Osmos (Osmosphere) | Amazon Advertising | Criteo | Skai | Topsort | Kevel |

|---|---|---|---|---|---|---|

| Platform Type | Full-stack retail media OS for retailers | Closed ecosystem for Amazon sellers | Demand aggregation and programmatic | Campaign management and measurement | API-first sponsored ads | Developer-first ad server |

| Who It Serves | Retailers building their own media network | Brands selling on Amazon | Brands buying across retail networks | Brands managing retail media spend | Start-up to mid-market marketplaces | Engineering-led teams building custom ad infra |

| Onsite Ads | Yes (PLA, display, video, gamified, carousel, story) | Yes (sponsored products, brands, display) | Yes (via retailer partners) | No (management layer only) | Yes (sponsored listings) | Yes (customizable ad server) |

| Offsite Ads | Yes (Meta, Google Shopping, DV360) | Yes (Amazon DSP) | Yes (Commerce Grid, open web) | No | No | No |

| In-Store Ads | Yes (digital screens, QR tracking) | Limited | No | No | No | No |

| White-Label | Yes | No | No | No | Partial | Partial |

| Deployment Time | 2 weeks (API Hub) / 4 weeks (Turnkey) | N/A (closed ecosystem) | N/A (demand-side tool) | N/A (management tool) | Days to weeks | Months |

| IAB Certified | Yes | Yes | Yes | N/A | No | No |

| Omnichannel | Yes (onsite + offsite + in-store) | Partial (onsite + DSP) | Partial (onsite + offsite via partners) | No | No | No |

| Key Strength | Complete OS covering formats, ops, and revenue strategy | Massive closed-loop data and scale | Access to 200+ retailers in one platform | Measurement and incrementality analytics | Fast API-first launch for marketplaces | Highly flexible custom ad infrastructure |

Amazon Advertising

Amazon is the benchmark for retail media, holding 79.7% of US retail media ad spend in 2025, far ahead of Walmart Connect at 8.0% and Target Roundel at 1.5% (eMarketer, 2026). eMarketer projects Amazon's retail media revenue will exceed $75 billion by 2028, more than $65 billion ahead of the next-largest RMN (eMarketer, 2026). However, Amazon Advertising is a closed ecosystem: its tools are only available to brands selling on Amazon. Retailers cannot use Amazon's platform to build their own media networks. Amazon's ad offerings include Sponsored Products, Sponsored Brands, Sponsored Display, and Amazon DSP for programmatic offsite activation. The key benefit for advertisers is access to Amazon's unmatched purchase data and conversion volume. The key limitation for retailers is that this ecosystem is inaccessible to non-Amazon sellers.

Amazon DSP is Amazon's demand-side platform, which allows advertisers to programmatically buy display, video, and audio ads both on Amazon properties and across the open web using Amazon's audience data. It is distinct from Amazon Ads (the self-service sponsored products platform) in that it supports offsite activation and is designed for larger budgets with managed or self-service access.

Criteo

Criteo operates primarily as a demand aggregation platform, connecting brands and agencies to over 200 retailers and premium media owners through Commerce Max (Criteo, 2025). Criteo helps brands buy across retail media networks; it does not help retailers build their own networks. Criteo's strength is its programmatic reach and offsite capabilities via Commerce Grid. In April 2025, Criteo introduced onsite video with launch partners including Albertsons, Costco, and Walmart Mexico. From a retailer's perspective, Criteo functions as a demand partner that would feed into a retailer-owned network.

Skai

Skai is a campaign management and measurement platform for advertisers managing spend across multiple retail media networks. In a Skai/Stratably survey of 166 retail media advertisers, retail media leaders allocated 27% of total media budgets to retail media, compared with 23% for laggards, and activated across an average of 7.2 networks versus 6.2 for laggards (Skai/Stratably 2026 State of Retail Media). Skai provides useful intelligence for brands, but it does not provide ad serving infrastructure. It cannot replace the need for a retail media platform on the supply side.

Topsort

Topsort is an API-first auction and sponsored ads platform designed for small-to-medium marketplaces seeking fast deployment. Topsort's strengths include quick integration, cookieless architecture, and SOC Type 2 compliance. Its limitations include a focus primarily on sponsored listings (no in-store or offsite media), limited enterprise features, and no full operations or revenue strategy layer.

Kevel

Kevel is a developer-first ad server offering extensive customization through APIs. It is the preferred choice for engineering-led teams building bespoke ad infrastructure. According to Kevel's own analysis, building a retail media platform from scratch can take years and cost hundreds of thousands in server fees, engineering salaries, and maintenance (Kevel, 2026). Kevel's integration timeline can take months, and report data can take up to 48 hours to reflect in dashboards. It is an ad server, not a full retail media operating system.

Where Osmos Fits

Osmos occupies a distinct position in the market: it is a full-stack retail media operating system for retailers and marketplaces building their own media networks. Where Criteo and Skai serve the demand side (advertisers buying media), Osmosphere serves the supply side (retailers creating and operating media networks). Where Topsort and Kevel provide point solutions (sponsored ads or ad serving), Osmosphere delivers a complete OS spanning ad formats, operations, and revenue strategy across onsite, offsite, and in-store channels, deployable in as little as two weeks via API Hub or four weeks via turnkey solution.

Proven results include 200% revenue growth in two months for Apollo 24x7 (India online pharmacy), 112% ad revenue increase in two months for Konvy (Thailand's largest online beauty retailer), and in-store retail media scaled across 1,300+ stores for an SE Asia multi-brand retail group, all powered by the Osmosphere platform.

Building vs. Buying: The Retail Media Platform Decision

Every retailer entering retail media faces a fundamental question: build your own platform in-house, buy point solutions and stitch them together, or deploy an integrated operating system.

Path 1: Build In-House

Building a retail media platform from scratch offers maximum customization and control. However, according to Kevel, a full DIY build requires years to launch and incurs hundreds of thousands in server fees, engineering salaries, and ongoing maintenance costs (Kevel, 2026). Most retailers underestimate the complexity of building not just an ad server, but also the operations layer (campaign management, advertiser onboarding, compliance) and the revenue strategy layer (yield optimization, demand generation, analytics). This path is best suited for the largest retailers with dedicated ad tech engineering teams and long investment horizons.

Path 2: Point Solutions

The point solution approach combines best-of-breed tools: an ad server from one vendor, an SSP from another, a reporting tool from a third. This reduces upfront engineering costs but introduces integration complexity, data fragmentation, and vendor management overhead. Advertisers interact with multiple systems, reporting is inconsistent, and campaign optimization spans disconnected tools. According to Kevel, 40% of advertisers and agencies have already secured new budgets specifically for retail media partnerships (Kevel, 2026); they expect a single, well-integrated experience, not a fragmented stack.

Path 3: Integrated Operating System

The integrated OS approach deploys a complete retail media platform from a single provider. This is the path that Osmosphere represents: a white-label, omnichannel retail media platform that goes live in 72 hours for basic omnichannel activation, two weeks for API Hub integration, or four weeks for full turnkey deployment. The retailer owns the platform, controls the data, and customizes the experience, without the multi-year engineering investment required for an in-house build.

For a detailed analysis of the build-vs-buy decision, see our guide on build or buy retail media ad technology. For marketplace-specific context, see how marketplaces can build their own ad platforms.

Retail Media Networks 2026: Build, Buy, or Hybrid? A Buyer's Matrix

Once a retailer settles on the build/buy/hybrid path, the next question is which platform actually fits the category economics and engineering bench. The matrix below compares the top retail media networks and platforms most retailers evaluate in 2026, three retailer-side operating systems and three brand-side or marketplace-first tools, across the dimensions that decide deployment success: side of the market, ad-format breadth, in-store and DOOH coverage, multi-vertical fit, the yield and operations layer, time-to-launch, and disclosed proof at scale. Use it as a shortlist filter, not a final scorecard.

| Platform | Side of market | Ad-format breadth | In-store / DOOH | Multi-vertical | Yield + ops layer | Time-to-launch | Proof at scale |

|---|---|---|---|---|---|---|---|

| Walmart Connect | Retailer-native | Sponsored Products, Display, Video, Sponsored Brand, In-Store, CTV (post-Vizio) | Yes (TV walls, demos, QR cart codes, Walmart Radio) | Grocery + general merchandise (Walmart-only) | Internal; not licensed externally | Not applicable (closed network) | ~$6.4B ad revenue (+46% YoY, FY2026); advertising plus membership together are roughly one-third of Walmart's total operating profit; ACG cut creative production time 80% |

| Amazon Ads | Retailer-native | Sponsored Products, Display, Video, DSP, AMC, Sizmek | Limited (Fresh / Whole Foods only) | Marketplace-only | Internal; not licensed externally | Not applicable (closed network) | $5.08 avg ROAS (Q3 2025); Sponsored Products spend +21% YoY with ROAS relatively stable and DSP spend +41% YoY (Tinuiti, Q1 2026); DSP Performance+ delivers 51% better acquisition cost |

| Target Roundel | Retailer-native | Sponsored Products, Display, Native Editorial, CTV (Roundel Media Network) | Limited (store-level signage) | Apparel, beauty, home, grocery (Target-only) | Internal; not licensed externally | Not applicable (closed network) | ~$2B ad revenue; 1.5% of 2025 US retail media ad spend (eMarketer); 3-6× ROAS, top performers 7×+ |

| Criteo | Hybrid commerce media network | Display, Video, Native, In-app, CTV (limited in-store) | Limited | Cross-retailer (commerce media aggregator) | Light; buy-side optimization, not retailer ops | Weeks to months depending on retailer integration | Largest commerce media data graph; cross-publisher reach |

| Topsort | Marketplace-first auction infrastructure | Sponsored Listings, Display, Sponsored Brand, Video | Limited | Marketplace-agnostic, vertical-light | Light yield layer; "BIDLESS" autobid | API-first, low-code; fast launch claim | Self-claimed 8 ms TP95; 2 endpoints + 1 post call |

| Osmos | Retailer-side operating system | 11+ formats: Product, Video, In-Store, Offsite, Display, Story, Product Display, Gamified, Influencer Live, Email, Carousel | Yes (Instore Ads + Advertima audience targeting; 1,300-store SE Asia deployment) | Grocery, beauty, fashion, QSR, in-store, OTT, pharma, all on a single OS | Full sell-side: ControlHub (ops) + StratEdge (yield) + WalletWise (budgets) | 4 weeks (turnkey) to 4 weeks (API hub); co-exists with current stack, white-labeled | 15-20 ms P95 latency, 25B auctions/month, 50B shopper events/month, 250B decision points/month, $80B+ media transacted |

How to read this matrix. Walmart Connect, Amazon Ads, and Target Roundel are destinations, places brands buy into, not platforms a third-party retailer can deploy. Criteo and Topsort are tools for buying or running marketplace auctions but stop short of the full retailer-side operating layer. Osmos is the multi-vertical operating-system option for retailers building their own RMN. The right shortlist depends on what you are actually shipping: ad inventory into a major network (Skai, Pacvue, Perpetua), or a network of your own (Osmos for full-stack; Topsort for marketplace-first; Criteo for commerce media aggregation; build in-house only at the largest scale).

For an honest take on what to build versus buy, see the Osmos build-vs-buy guide. To estimate the revenue impact of expanding your match-type taxonomy (Exact, Phrase, Broad, Contextual), the retail media revenue uplift calculator projects fill-rate and revenue lift from each match-type expansion step.

Retail Media Measurement, Attribution, and Compliance

Measurement and Attribution

Retail media's core value proposition rests on measurement: the ability to prove that an ad impression drove a product purchase. Closed-loop attribution connects ad exposure to in-store or online purchase within the same ecosystem, eliminating the guesswork inherent in traditional digital advertising.

However, measurement remains the industry's most significant challenge. According to Forrester's State of Retail Media 2025, 86% of commerce media decision-makers in North America and Europe say strengthening measurement and attribution is a high or critical priority (Forrester, 2025). A Skai/Stratably survey of 166 retail media advertisers found incrementality is now the single biggest measurement challenge, cited by 75% of advertisers, even as only 15% describe themselves as very or extremely effective at measuring retail media performance and about seven in ten say they met or exceeded their 2025 goals (Skai/Stratably 2026 State of Retail Media Measurement and Incrementality). The gap between what retail media promises (closed-loop measurement) and what most networks actually deliver (last-click attribution within limited windows) is the single largest source of advertiser frustration.

On the performance side, Tinuiti's Q1 2026 benchmark showed Amazon Sponsored Products spend up 21% year over year with ROAS relatively stable, Amazon DSP spend up 41%, and Walmart Sponsored Products spend up 62% with stronger ROAS, a sign that demand and returns are still climbing across the two largest networks (Tinuiti, Q1 2026). Which networks deliver the best ROAS depends heavily on vertical, match type, and attribution window; for a marketplace-specific ROAS breakdown, see our guide to retail media ROI for marketplaces.

Incrementality testing, using holdout groups and matched market experiments to isolate the true lift from advertising, is emerging as the standard for sophisticated retail media measurement. For detailed ROAS benchmarks across platforms and ad formats, see our guide to ROAS benchmarks by platform and ad format.

Match-type expansion is the highest-ROI yield lever most operators leave on the table. Retail media networks that ship only Exact-match keyword targeting capture a fraction of the demand that Phrase, Broad, and Contextual targeting can fill. The lift compounds: a network running Exact-only at $1M monthly ad revenue typically sees double-digit revenue and fill-rate gains by adding Phrase and Broad, with another step-up at full Contextual. The Osmos retail media revenue uplift calculator projects the specific revenue and fill-rate gain for your current ad revenue and match-type configuration, a 60-second sanity check before committing engineering effort to a match-type rollout.

Data Privacy and Compliance

Retail media's dependence on first-party shopper data makes privacy compliance non-negotiable. The regulatory landscape in 2026 includes:

- GDPR (EU): Fines can reach up to 20 million euros for violations of data processing requirements

- CCPA/CPRA (California): Expanding enforcement under the California Privacy Protection Agency, with 20+ US states having enacted comprehensive privacy laws by 2025 (Secure Privacy, 2025)

- India DPDPA: The Digital Personal Data Protection Act creating new compliance requirements for Indian e-commerce platforms operating retail media

- Cookieless Architecture: Platforms must support first-party, cookie-less targeting and attribution to remain compliant and effective as third-party cookies continue to deprecate

Retailers operating retail media networks must implement privacy-by-design principles: consent management, data minimization, purpose limitation, and transparent data processing agreements with advertisers. Osmosphere supports this through cookie-less BYOT (Bring Your Own Traffic) attribution and IAB-certified compliance.

Security Standards

Platform security is increasingly a procurement requirement for enterprise retail media. SOC Type 2 certification, data encryption at rest and in transit, and role-based access controls are baseline expectations for retailers evaluating technology partners.

Retail Media by Market: US, India, SE Asia, and Australia in 2026

United States

The US is the most mature retail media market globally. According to eMarketer, US retail media spending is projected at $71.09 billion in 2026, up 17.8% year over year (eMarketer, 2026). Amazon and Walmart together held 87.7% of total 2025 US retail media spend (Amazon 79.7%, Walmart Connect 8.0%) and are on pace to absorb more than 89% of all incremental, net-new 2026 dollars, with $9.42 billion of the $10.53 billion in added spend going to the two networks (eMarketer, 2026). The opportunity for non-Amazon retailers is in the remaining market share, where Kroger Precision Marketing, Target Roundel, Albertsons, and Instacart are all scaling their networks. DoorDash Ads and Instacart Ads each now generate close to $1 billion in annual US ad revenue, a sign that a scaled second tier is forming beneath the two leaders.

Walmart Connect has been particularly aggressive, deploying Gen-AI powered Automated Creative Generation (ACG), which reduced advertisers' median creative production time by 80% (Walmart Connect, 2026). The financial payoff is now material: Walmart's global advertising business generated nearly $6.4 billion in FY2026 and grew about 46% year over year, and advertising plus membership income together account for roughly one-third of Walmart's total operating profit (McMillanDoolittle, citing Walmart FY2026 earnings, 2026). Walmart's move into CTV through its Vizio acquisition has also expanded the definition of what retail media inventory can include. For US-market benchmarks and SMB retailer guidance, see the Osmos US Retail Media Report.

Grocery retail is the vertical leading US retail media adoption. Kroger, Albertsons, and Walmart all derive significant and growing ad revenue from sponsored products and display ads. Electronics retail is also showing strong retail media performance, with retailers like Best Buy and Costco running high-ROAS sponsored product programs.

India

India is one of the fastest-growing retail media markets globally, with platforms like Flipkart, Amazon India, BigBasket, Blinkit, and Meesho all investing in retail media capabilities. The category density that distinguishes India is operator: a single ecosystem covering grocery (BigBasket, Blinkit), beauty (Purplle), pharmacy (Apollo 24|7, TrueMeds, Tata 1mg), mobility (Rapido), restaurants and retail (Jiffy by Spencers), and marketplaces (Flipkart, Meesho), all with their own retail media ambitions. Osmos has shipped at scale across this density: Apollo 24|7 achieved 2× growth in participating brands through cleaner attribution and self-serve campaign management; Purplle scaled monetization through peak IHB sale moments; Rapido unlocked over $12K in incremental advertiser budgets with bespoke ad-serving features; TrueMeds and Tata 1mg built compliance-grade healthcare retail media on the Osmos platform; and Jiffy by Spencers used Osmos to navigate surrogate advertising for liquor brands. Indian online pharmacies on the Osmos platform have achieved 100% quarter-over-quarter ad revenue growth.

The Indian retail media ecosystem is characterized by mobile-first consumption, UPI payment infrastructure enabling frictionless transactions, and rapid quick commerce expansion creating new inventory for ad formats.

Southeast Asia

SE Asia's standout proof point is operational: one of the region's largest multi-brand retail groups deployed in-store retail media across 1,300+ stores and 90+ digital screens covering 5 markets (health, beauty, grocery, and convenience), moving from manual CMS-driven campaign scheduling to a unified retail media engine in a 4-week implementation. The deployment surfaces the structural difference between a "we have screens" retail media program and a multi-store networked one: aisle-level localized targeting, QR-tracked offline-to-online attribution, and centralized advertiser onboarding with the Osmos and Advertima partnership for AI-driven shopper audience targeting. The implication for any SE Asia or India retailer with physical footprint: the network economics work below 1,300 stores too, but the operational ceiling without a unified ops layer is roughly 30-50 stores before fragmentation overwhelms the team.

SE Asia is an emerging retail media market with significant growth potential. Major platforms including Shopee, Lazada, and Tokopedia are investing in sponsored ad products, and app-native, mobile-first ad formats dominate the region. Osmos operates at scale in this market, and the APAC picture is detailed further in the Osmos APAC Retail Media Report.

Australia

Australia's retail media market is estimated at A$3 billion, with Woolworths (operating through its Cartology media network), Coles (through Coles 360), and new entrant Bunnings (through Hammer Media) as the key players (Inside Retail Asia, 2025). Australian retailers have been early leaders in in-store retail media, deploying point-of-sale screens and app video ads to complement their digital advertising.

For a deeper examination of how retailers across markets are transforming into media companies, see our guide on retailers becoming media networks.

The Future of Retail Media: What Changes by 2027

The retail media trends shaping 2026 and 2027 cluster around four shifts: AI-run campaign operations, in-store media going mainstream, network consolidation at the top, and the convergence of retail media into commerce media.

AI-Powered Campaign Optimization

AI is reshaping retail media operations. Walmart Connect's Automated Creative Generation reduced production time by 80% (Walmart Connect, 2026), and according to Rockbot, AI-driven targeting delivers 6x more ROI than traditional targeting methods (Rockbot, 2026). The next wave applies AI to campaign management, bid optimization, and clean-room measurement, shifting from generative content creation to operational intelligence. In June 2026, CVS Media Exchange launched CorIQ, an AI-driven closed-loop measurement platform, and Albertsons Media Collective introduced onsite incrementality measurement, both signals that AI is moving from creative into measurement (Mars United, June 2026).

In-Store Retail Media Goes Mainstream

With 76% of purchases still occurring in physical retail locations (Rockbot, 2026), in-store retail media is the next major growth frontier. Digital screen networks, QR-tracked activations, and POS-integrated promotions are bridging the measurement gap between physical and digital channels. The IAB's establishment of formal standards for in-store retail media validates this channel's maturity.

Retail Media Network Consolidation

The market is likely to consolidate around two models: large-scale proprietary networks (Amazon, Walmart) and white-label platform-powered networks built on operating systems like Osmosphere. The middle ground, retailers running isolated, manually managed ad programs, will shrink as advertiser expectations for programmatic buying, real-time reporting, and omnichannel activation become table stakes. The concentration is stark: eMarketer expects Amazon and Walmart to absorb more than 89% of all incremental US retail media dollars in 2026, forming a scaled second tier beneath them while the long tail falls further behind (eMarketer, 2026). At the same time, brands are managing more networks, not fewer: a Skai/Stratably survey of 166 retail media advertisers found the average brand works with six retail media networks today and expects that to reach 11 by the end of 2026 (Skai/Stratably 2026 State of Retail Media). The strategic answer to that fragmentation is a unified operating layer rather than another point tool.

Commerce Media Convergence

Retail media, affiliate marketing, CTV advertising, and social commerce are converging into a single budget category: commerce media. eMarketer now forecasts commerce media as its own line item, projecting US commerce media ad spending will reach $142.07 billion and account for 23.9% of all US digital ad spending by 2030 (eMarketer, 2026). Commerce media is a distinct superset of retail media: it extends the same first-party commerce data off retailer-owned properties into CTV, social, streaming, and other commerce-adjacent environments. In February 2026 the IAB and IAB Europe published a formal framework separating measurable retail media from legacy trade spend, an industry signal of how quickly the category's definition is maturing (IAB, 2026). Forrester projects retail media alone will reach roughly twice the level of global television ad spending by 2030 (Forrester, 2025).

The Retailer-as-Media-Company Model

The end-state of retail media evolution is the retailer-as-media-company model: retailers operating full-stack media businesses (complete with self-serve advertiser portals, programmatic demand partnerships, multi-format inventory, and cross-channel measurement) as a core revenue function alongside product sales. For a deeper exploration of this transformation, see our analysis of the unified ad technology future shaping the next era.

Frequently Asked Questions

What Is the Difference Between Retail Media and Commerce Media?

Retail media is advertising sold on a retailer's own digital and physical properties, its site, app, and in-store screens, using that retailer's first-party shopper data to target ads and measure them against real purchases. Commerce media is the broader superset: the same first-party commerce data extended off those owned properties into the open web, connected TV, social, and other commerce-adjacent environments the retailer does not own outright. In 2026 the definition is evolving on two fronts. The IAB and IAB Europe published a February 2026 framework separating measurable retail media from legacy trade spend, and eMarketer began forecasting commerce media as its own category, projecting US commerce media ad spending will reach $142.07 billion, or 23.9% of all US digital ad spending, by 2030 (eMarketer, 2026). The practical shift is that operators now treat retail media as the owned-and-operated core of a larger commerce-media budget line rather than a separate channel.

What's New in Retail Media in June 2026?

June 2026 brought rapid platform expansion across the major retail media networks. Amazon Ads rolled out Dynamic Creative TV for personalized, interactive video ads on Prime Video and expanded streaming inventory access through Microsoft's SSP. Walmart Connect opened Vizio ad inventory through the Yahoo DSP, launched self-service Meta campaigns built on Walmart shopper data, and extended LiveRamp clean-room measurement to Meta. CVS Media Exchange introduced CorIQ, an AI-driven closed-loop measurement platform built on ExtraCare loyalty data. Albertsons Media Collective launched onsite incrementality measurement to standardize cross-campaign comparisons. DoorDash Ads added a premium Spotlight Ad homepage placement and scaled off-site reach through Symbiosys, while Instacart extended its self-service ad platform to retail partners. Outside the US, Chile's Grupo Falabella migrated its retail media business onto Topsort's infrastructure. Framing all of it, the IAB and IAB Europe published a formal framework separating measurable retail media from legacy trade spend (Mars United, June 2026; IAB, 2026).

What Are the Biggest Challenges in Retail Media for Retailers?

The biggest challenges include data fragmentation across walled garden networks (advertisers now manage campaigns across 5-7+ networks with separate logins, reporting, and naming conventions), measurement standardization (according to Forrester, 86% of decision-makers say attribution improvement is a high or critical priority), first-party data coverage gaps for shoppers not enrolled in loyalty programs, and the organizational complexity of determining whether retail media sits in sales, marketing, or a dedicated team.

What Are the Biggest Challenges in Retail Media for Marketplaces?

Marketplaces face unique challenges including building self-serve advertiser tools that scale to thousands of sellers, managing campaign quality and content compliance at volume, balancing organic product rankings with paid placements to preserve shopper experience, and deploying multiple ad formats beyond basic sponsored listings to maximize yield per impression.

What Is the Difference Between Amazon Ads and Amazon DSP?

Amazon Ads is the self-service platform where sellers and vendors create Sponsored Products, Sponsored Brands, and Sponsored Display campaigns. It operates within the Amazon ecosystem and is primarily performance-based (cost-per-click). Amazon DSP is a demand-side platform that allows advertisers to programmatically buy display, video, and audio ads across Amazon properties and the broader web. Amazon DSP supports audience targeting using Amazon's purchase data but extends reach beyond Amazon's owned properties. Amazon DSP is designed for larger budgets and is available through managed or self-service access.

What Is Amazon DSP and How Does It Work for Retail Media?

Amazon DSP enables advertisers to reach audiences on Amazon-owned properties (IMDb, Twitch, Fire TV) and across third-party exchanges using Amazon's first-party audience segments. It supports display, video, and audio formats. For retail media purposes, Amazon DSP is the offsite activation arm of Amazon's advertising ecosystem, allowing brands to retarget shoppers who browsed Amazon with ads served on external websites and apps.

How Does Amazon Advertising Compare to Kroger Precision Marketing?

Amazon Advertising offers the largest scale and deepest purchase data in retail media, but operates as a closed ecosystem. Kroger Precision Marketing leverages Kroger's 84.51 degree data science unit and 60+ million loyalty households for audience targeting. Kroger's advantage is its grocery-specific purchase data depth and its openness to programmatic demand through partnerships. Amazon's advantage is scale (79.7% of US retail media ad spend in 2025). For non-grocery brands, Amazon typically offers broader reach; for CPG and grocery brands, Kroger provides unmatched category-specific targeting.

How Does Amazon Advertising Compare to Target Roundel?

Amazon Advertising dominates in scale and breadth of ad formats. Target Roundel differentiates through its unique audience of Target shoppers and its integration of in-store and digital media. Roundel offers managed-service campaigns with strong brand storytelling capabilities and access to Target's Circle loyalty data. Amazon is better for performance-focused, self-service campaigns at scale; Roundel is stronger for brands seeking a curated, brand-safe environment with omnichannel measurement.

What Are the Best Practices for Retail Media Creative Optimization?

Creative optimization in retail media requires matching creative assets to format specifications across multiple networks. Best practices include: maintaining a library of format-specific templates (sponsored product images, display banners, video pre-rolls, in-store screen assets), using AI-powered creative generation tools (Walmart Connect's ACG reduced production time by 80%), A/B testing creative variants within each network, ensuring brand safety compliance through automated content validation (like Content Cop), and aligning creative messaging to the shopper's position in the purchase funnel.

How Do You Integrate a Retail Media Platform with POS Systems?

POS integration connects in-store transaction data with digital ad exposure data, enabling closed-loop attribution for physical retail. The integration typically involves API-based connections between the retail media platform and the retailer's POS system, mapping transaction-level data (product purchased, store location, timestamp) to ad impression and click data. Osmosphere supports this through its in-store ads module within Adscape, which includes digital screen CMS integration and QR tracking for aisle-level attribution.

How Should Retailers Organize Their Retail Media Teams?

Retail media teams should be organized as a dedicated function with clear P&L ownership, rather than being embedded within sales or marketing. Leading organizations typically structure teams with a Head of Retail Media reporting to the Chief Revenue Officer or Chief Digital Officer, supported by ad operations specialists, advertiser account managers, data analysts, and yield optimization managers. Tools like ControlHub automate the operational workflows (campaign review, onboarding, billing) that would otherwise require large manual teams.

What Is a Retail Media Supply-Side Platform (SSP) and What Does It Do?

A retail media SSP is the technology that enables retailers to make their ad inventory available to external demand sources programmatically. According to Koddi, commerce media SSPs serve all commerce media formats programmatically, including sponsored listings, display, in-store screens, and audio (Koddi, 2025). SSPs help retailers attract incremental national brand budgets flowing through agency DSPs, effectively expanding the retailer's addressable advertiser base beyond the brands that sell directly on their platform.

What API Integration Capabilities Does a Retail Media Platform Need?

A retail media platform must support campaigns APIs (for programmatic campaign creation and management), events APIs (for real-time impression, click, and conversion tracking), reporting APIs (for advertiser dashboards and analytics), and integration with the retailer's product catalog, inventory, and customer data platform. Osmosphere provides all four through its API Hub, which enables two-week deployment with full programmatic capabilities.

How Does Retail Media Inventory Management and Ad Supply Work?

Retail media inventory is the set of ad placements available across a retailer's digital and physical properties. Inventory is dynamic: it varies by site traffic, product catalog size, page types (search results, category pages, product detail pages), and physical store locations. Effective inventory management requires automated yield optimization (pricing ad slots based on demand), floor price controls, frequency capping to protect shopper experience, and programmatic access through SSP integration to maximize fill rates.

Conclusion: Building Your Retail Media Network in 2026

Retail media has evolved from simple banner ads into a full-stack advertising channel that rivals, and will soon surpass, traditional television advertising. The retailers capturing the most value are the ones building integrated media platforms rather than stitching together point solutions.

The market opportunity is clear: Forrester projects global retail media spending will grow from $184 billion in 2025 to $312 billion by 2030, an 11% compound annual growth rate that puts it at roughly twice global television ad spend (Forrester, 2025). The technology to capture it is available today. Osmosphere provides the complete retail media operating system, covering ad formats (Adscape), campaign operations (ControlHub), and revenue strategy (StratEdge), deployable in as little as two weeks.

Estimate your retail media revenue opportunity with the Retail Media Revenue Calculator, or explore how to go live in four weeks with Osmos.

.png)