Subscribe to our news letter

Last updated: June 2026

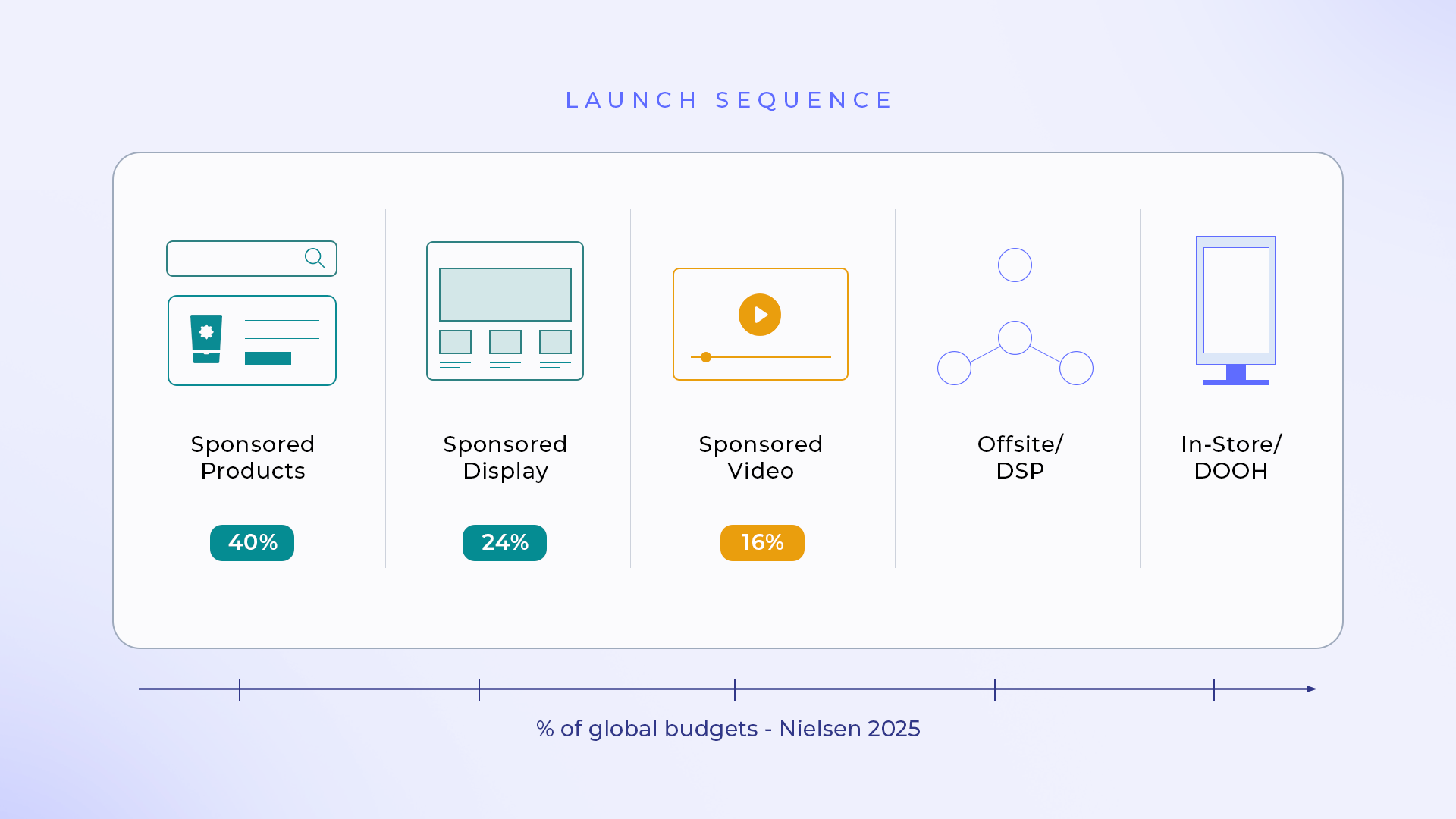

Sponsored ad formats in retail media split into five operator-relevant categories: Sponsored Products (onsite search), Sponsored Display (onsite browse and retargeting), Sponsored Video (onsite and offsite shoppable video), Offsite (DSP and programmatic extension to Meta, Google Shopping, and DV360), and In-Store / DOOH (digital screens and connected store environments). Each format carries a different revenue profile, implementation cost, and measurement maturity, and the order in which a retailer or marketplace launches them determines how much revenue per advertiser dollar the network ultimately captures. For the platform-by-platform performance numbers each of these formats actually earns once they ship — Amazon, Walmart, Instacart, and beyond — see our pillar guide on ROAS benchmarks by platform and ad format in 2026; this article is the format-mechanics and operator launch-decision guide that sits underneath it.

This is an operator's guide. If you run a retail media network, marketplace ad business, or quick-commerce monetization stack — and you are deciding which sponsored ad formats to launch, in what sequence, with which tech, and at what pricing model — every section below is written from your seat. Brand and agency readers will still find the format mechanics useful, but the calls to action assume you are the seller of the inventory, not the buyer.

Why Sponsored Ads Define the Retail Media Revenue Stack

US advertisers will spend $39.64 billion on retail media search in 2025 — 63.6% of all retail media ad spend, according to eMarketer (eMarketer, January 2025). Globally, retail media is on track to reach $60 billion in the US in 2025 and $100 billion by 2028 (Nielsen, June 2025). And inside that pie, the sponsored-ads category dominates: Nielsen's 2025 cut puts sponsored products at 40% of global retail media budgets, sponsored brands at 24%, display at 20%, and video at 16%.

That mix is the single most important benchmark a new retail media operator will encounter. It is also a moving target. Off-site retail media ad spend is growing 42.1% in 2025, nearly three times the on-site growth rate of 15.3%, according to eMarketer projections (eMarketer, April 2025). On the same forecast, US omnichannel retail media advertising reaches $61.2 billion in 2025, with CTV inside retail media growing 43.1% to $4.86 billion. In short: the format mix that produced your revenue base in 2024 is not the format mix that will produce it in 2026.

"RMNs can now deliver value across every stage of the buying journey, building awareness, driving consideration and strengthening loyalty." — AdExchanger editorial, The Full-Funnel Retail Media Network, October 2025

Underneath those market-size numbers, Osmos Adscape is the format suite this article maps to: a single white-label stack that covers product, display, video, offsite, in-store, gamified, story, and influencer-live formats so an operator can sequence launches without stitching together point solutions per format. We come back to that suite explicitly in the launch-sequencing section. First, the taxonomy.

The Five Sponsored Ad Format Categories in Retail Media

A sponsored ad in retail media is paid commercial inventory that appears inside a retailer or marketplace's owned digital or physical surfaces — search results, browse pages, product detail pages, video carousels, in-store screens — typically priced per click or per thousand impressions and attributed back to the retailer's first-party purchase data. The word "sponsored" distinguishes paid placements from organic results; the word "retail media" distinguishes them from open-web display or social ads bought against third-party audiences.

There are two ways to organize the format taxonomy. The Amazon trichotomy — Sponsored Products, Sponsored Brands, Sponsored Display — is widely cited but pulls operators into a single retailer's product naming. The retailer-agnostic taxonomy used by IAB Europe and Nielsen is more useful when you are deciding what to build. IAB Europe's updated 101 Guide to Retail Media (July 2025) splits the universe into digital on-site, digital off-site, and digital in-store formats, with sponsored products, display, and video as the three primary on-site sub-types. We extend that into a five-category operator framework:

| # | Format category | Operator framing |

|---|---|---|

| 1 | Sponsored Products | Onsite search auction; CPC; revenue anchor for every new RMN |

| 2 | Sponsored Display | Onsite browse, retargeting, and PDP placements; CPM + tenancy |

| 3 | Sponsored Video | Onsite and offsite shoppable video; CPM premium; awareness + NTB |

| 4 | Offsite (DSP) | First-party-data activation on Meta, Google Shopping, DV360; CPM programmatic |

| 5 | In-Store / DOOH | Digital screens, smart carts, aisle displays; emerging measurement |

That five-row taxonomy is the spine of the rest of this article. Inside each section we cover the mechanics, the revenue profile, the launch prerequisites, and the operator decision framework for that format. Two formats sit slightly outside this scope and have dedicated coverage elsewhere: native ads in editorial / recommendation feeds (a planned spoke) and emerging engagement formats — gamified, story, carousel — which sit as Adscape capabilities within categories 2 and 3 rather than as separate categories. On the European baseline, on-site retail media ad spend grew 22.2% to over €10 billion in 2024, with over 90% of advertisers now partnering with retailers (IAB Europe, July 2025). The format-portfolio question is no longer hypothetical for any non-trivial retailer.

A note on vendor naming. We deliberately do not use Amazon, Walmart, Criteo, or Target product names in the H2s of this article. They appear inside the sub-sections as worked examples — because they are the most documented operator-side format launches in the public record — but the framework is retailer-agnostic. Amazon's specific Sponsored Products / Sponsored Brands / Sponsored Display trichotomy is one implementation of categories 1 and 2, not the universal map.

1. Sponsored Products: The Onsite Search Revenue Anchor

Sponsored Products are paid product listings that appear in a retailer's onsite search results, category browse pages, and sometimes on product detail pages, ranked by a combination of bid (typically CPC) and relevance to the shopper query. They are the highest-intent, lowest-friction sponsored format and the entry point for every retail media network we have seen launched.

The mechanics are simple in concept and complex in execution. A retailer sets aside a configurable share of search results — often two to four positions per page — for paid placements. Advertisers bid on keywords (or, more commonly today, on auto-targeted product attributes) and the auction selects winning ads on a blend of bid value and predicted relevance. Inventory is theoretically infinite (every search query is a new auction) but practically constrained by query depth and ad load: at low query volumes, the operator runs out of bidders; at high ad loads, organic relevance suffers.

The market-leader benchmark on ad load comes from Amazon: 99% of Amazon searches display sponsored products, with an average of 20 sponsored listings per page load (eMarketer, January 2025). Mid-market RMNs sit far below that line — Staples, by way of contrast in the same eMarketer report, "increased sponsored listing coverage by 17.2% in H2 2024" but "only 68% of searches showed sponsored products." The 30+ percentage-point gap is the bid-density problem in one number: most non-Amazon networks have far more empty inventory than they have advertisers willing to bid on it.

That is also the operator opportunity. eMarketer projects approximately $5 billion in incremental retail media search ad spending flowing into 2026 (eMarketer, December 2024). The networks that capture a disproportionate share of that incremental spend will be the ones that solve bid density first — through better contextual targeting, smarter advertiser onboarding, and self-serve campaign tools that lower the activation bar.

"Is it a distracting, intrusive ad? Or is it something equally as relevant to an organic search result?" — Andreas Reiffen, CEO, Pentaleap, quoted in eMarketer, January 2025

The relevance test is the long-running operator dilemma for sponsored products. Push ad load too aggressively and search quality degrades; under-monetize and you leave revenue on the table. Most networks land somewhere between Staples' 68% and Amazon's 99% and tune from there.

Operator launch checklist for Sponsored Products:

- A first-party product catalog with structured attributes (brand, category, price, availability) refreshed at least daily

- A keyword or attribute auction with a relevance scoring function — pure bid auctions destroy search quality within weeks

- A self-serve advertiser console with budget caps, daypart controls, and pacing

- A reporting layer that returns impressions, clicks, ad-attributed sales, and ROAS at SKU granularity

- A bid-density growth plan: contextual auto-targeting, advertiser incentives for under-bid categories, house ads to fill remaining inventory

Osmos's Product Ads module covers the auction, contextual targeting, inventory sync, and 1-click campaign setup that closes the gap between catalog and sellable inventory. ML-powered contextual promotion is the lever that disproportionately improves bid density on non-Amazon RMNs where keyword coverage is sparse — the network synthesizes bidder demand by matching advertiser intent to query context rather than waiting for advertisers to manually keyword-load.

Pricing model: CPC auction is the dominant pricing for Sponsored Products. Some networks add reserve floors per keyword cluster or premium placement uplifts; both are pricing tweaks rather than separate models.

2. Sponsored Display: Onsite Browse, Retargeting, and the Banner Renaissance

Sponsored Display — also called sponsored banner, native display, or onsite display — covers paid placements that appear on browse pages, category pages, product detail pages, the cart, and the post-purchase confirmation surface. Targeting is contextual (the page or category being browsed), behavioral (recent on-site shopper actions), or audience-based (first-party shopper segments). Pricing is typically CPM with a layer of fixed-tenancy reservations for premium placements like the homepage carousel.

Native ad formats, sponsored placements that match the look and feel of the surrounding content, are a fast-growing slice of this category; see our native advertising in retail media benchmarks guide for format-level performance data.

Sponsored Display is where most operators see their first revenue diversification beyond sponsored products. Where SP is high-intent and conversion-led, SD is upper-funnel and brand-led — which is why the buyer pool is different (more brand budgets, more category-marketing budgets) and why CPMs are typically richer on a per-impression basis. For operators, SD has three structural advantages: a small number of premium placements can carry six- and seven-figure tenancy deals from CPG and category captains; ad-load tuning is more forgiving than search; and creative production cycles are familiar to brands that already buy banner display elsewhere.

A specific worked example: Target's Roundel "now generates nearly $2 billion in value, with a goal to double that over the next five years," according to the Path to Purchase Institute, July 2025. Roundel's portfolio "spans on-site sponsored listings, off-site programmatic, social, CTV, video, audio, influencer, out-of-home, and in-store formats" — a multi-format operator pulling on every category in this taxonomy. The Precision Plus buying solution announced in 2025 layers first-party data and real-time shopper behavior on top of the display inventory; this is the trajectory most ambitious RMNs follow once their sponsored-products engine is producing reliably.

Hybrid formats live inside this category as well. The Product Display Ad (PDA) sits between sponsored product and display: a banner-shaped placement with product context (price, image, "Add to cart") that competes for the same surfaces as banner display but converts more like sponsored product. PDAs are useful for operators whose advertisers have catalog feeds but limited creative production capacity.

For deeper history on how display formats evolved from generic banners into the targeted, native placements in use today, our companion piece on the display ad evolution in retail media covers the design and inventory shifts in detail.

Operator launch checklist for Sponsored Display:

- An inventory catalog of every browseable surface — homepage, category pages, PDP, cart, post-purchase — with placement IDs and slot specs

- An ad server that supports both auction and tenancy fulfillment in the same surface (most legacy GAM deployments don't)

- A creative review layer (brand safety, ad-spec compliance, accessibility)

- First-party audience segmentation tied to onsite browse and purchase signals

- A pricing strategy that mixes CPM auction floors with reserved tenancy for premium surfaces

Osmos's Display Ads and PDA modules cover both the auction-driven and tenancy-driven surfaces, with first-party targeting and geo targeting built in. ControlHub's Content Cop layer applies AI content validation to every creative before it ships, which removes one of the more expensive ops-cost line items in display advertising.

Pricing model: CPM with fixed tenancy on premium surfaces. A CPC option is available on some hybrid PDA placements but is not the dominant model.

3. Sponsored Video: The Fastest-Growing Format Category

Sponsored Video covers shoppable video ads served on a retailer's onsite surfaces (search results, category pages, PDP carousels) and increasingly on offsite environments (CTV, partner ecommerce sites, social) using the retailer's first-party data. It is the format category with the most format-launch activity in the past 18 months — and the strongest documented performance evidence in the retail media research base.

The single most cited operator-side video test is Albertsons' beta of Criteo Onsite Video (April 2025): a 280% increase in click-through rates and a 460% sales lift when Onsite Video was paired with Sponsored Products, plus a 5.6x lift in new-to-brand customers when video was combined with display and sponsored products in a unified plan. Digital Commerce 360's independent coverage of the same test confirms the headline numbers (Digital Commerce 360, April 2025). Six months later, Kroger Precision Marketing launched Onsite Video Carousels on Kroger.com and the Kroger app, combining short-form video with shoppable product listings inside search results. KPM did not publish performance figures at launch — but the format's existence on a top-three US grocer's primary search surface tells the operator audience where this category is heading.

"Video has always been a powerful storytelling tool but rarely a direct driver of commerce – until now." — Stephen Howard-Sarin, Managing Director, Retail Media for the Americas, Criteo, press release, April 2025

The new-to-brand framing matters more than the conversion stats for operators thinking about format mix. Walmart Connect's Sponsored Videos product page reports that 91% of sales from Sponsored Videos come from new-to-brand customers (for SMB advertisers, FY2025) (Walmart Connect, Sponsored Videos) — the qualifier matters: this is the SMB-advertiser cohort across Feb 2024 – Jan 2025, not a universal NTB rate across all brand sizes. For Sponsored Brands, 69% of orders come from new-to-brand buyers in the same period (Walmart Connect, Sponsored Brands). What both figures tell an operator is the same thing: video and brand-led formats reach buyers a brand has not previously transacted with — the audience that incremental retail-media spend is meant to capture.

CTV is the offsite extension of the same format category. CTV spend within retail media grew 43.1% in 2025 to $4.86 billion (eMarketer, April 2025), and connected-TV environments are where retailers are stretching first-party data outside the owned site. Format mechanics differ — full-screen 15-second to 30-second video, no in-feed competition, household-level targeting — but the operator-side decision (do we license our data to a CTV platform? do we co-sell?) ladders into the same category.

Operator launch checklist for Sponsored Video:

- A creative onboarding workflow that accepts vertical, square, and landscape variants with auto-trim

- An ad server that serves video without an external SDK on mobile web (the SDK requirement is a frequent advertiser blocker)

- An attribution layer that ties video impressions to subsequent ad-attributed sales, ideally with a NTB cut

- A creative cost-share program for advertisers without in-house video production (this is the bottleneck most networks under-invest in)

- A measurement story that handles both view-through and click-through attribution per format

Osmos's sponsored video ads module covers autoplay, video analytics, and ML-served creative variants. Story Ads and Influencer Live (within Adscape) extend the category into full-screen and shoppable creator formats — both useful additions once base video is producing reliably.

Pricing model: CPM premium, often 2-3x the CPM of static display on the same surface. Tenancy options exist for category-takeover formats.

4. Offsite (DSP and Programmatic Extension)

Offsite formats extend a retail media network's first-party data and ad inventory into environments the retailer doesn't own — Meta, Google Shopping, DV360, the open programmatic web, and increasingly CTV. The retailer is the data and audience source; the inventory comes from external publishers and platforms. From an operator perspective, offsite is the format where the revenue per advertiser dollar is lower per impression but the addressable spend pool is meaningfully larger.

The growth differential is the most-cited stat in the category. Off-site retail media ad spend will grow 42.1% in 2025, nearly three times the on-site rate, per eMarketer projections (eMarketer, April 2025). The directional story is consistent across analyst sources: off-site is where incremental retail media budget is moving, and operators that can offer both surfaces (onsite + offsite) capture a structurally larger share of advertiser planning.

The operator case for offsite is built on three pieces of evidence. First, demand is there: 96% of brands and agencies are open to buying on-site retail media through a DSP, 80% say DSP buying would make it easier to shift more budget to retailers, and 66% cite more cost-efficient buying as the top DSP advantage, per Koddi's survey of 126 Fortune 1000 brand and agency decision-makers (Koddi, May 2025). Second, performance evidence is now public: AdExchanger's case study of Proximo Spirits documents 60% new-to-brand sales, 200% ROAS, and 10x higher off-site impression volume than on-site in an integrated campaign that combined onsite and offsite formats (AdExchanger, October 2025). Third, the audience expansion case: offsite is where retailers monetize the segment that visits the site occasionally or not at all — the long tail that onsite formats structurally cannot reach. Our piece on audience monetization beyond onsite ads covers that demographic logic in more detail.

"The fragmented, one-off nature of today's RMNs is seen as a barrier, not a benefit." — Koddi programmatic report, May 2025

The operator implication: advertisers are tired of stitching one-off integrations across four to six retail media networks. The networks that win the offsite share will be the ones that make data and inventory accessible through the DSPs advertisers already use — Meta Ads, Google's Shopping ad stack, DV360 — rather than asking each advertiser to learn yet another vendor console.

Operator launch checklist for Offsite:

- A first-party data layer mature enough to export shopper segments to external platforms with privacy and consent enforcement

- Activation integrations with at least Meta, Google Shopping, and one DSP (DV360 or The Trade Desk)

- A clean-room or matched-cohort capability so advertisers can measure offsite-driven sales back to the retailer's POS

- A pricing strategy that handles both CPM programmatic and managed-service models — the two buyer types for offsite are different

- A measurement narrative that handles closed-loop attribution across both onsite and offsite touchpoints in one report

Osmos's offsite retail media advertising module activates Meta, Google Shopping, and DV360 from a single operator console — the multi-channel design specifically addresses the fragmentation pain Koddi documents. For most mid-market RMNs, offsite is the Phase 2 launch (after a stable sponsored-products engine), not the Phase 1 launch.

Pricing model: CPM programmatic for the bulk of inventory, with managed-service overlays for advertisers that need full-funnel campaign management.

5. In-Store and DOOH: The Newest Format Category

In-store retail media covers digital screens, smart carts, aisle endcaps, and connected store environments — paid placements served at the physical point of sale. DOOH (digital out-of-home) extends the category into store-adjacent surfaces like fuel stations and pickup areas. It is the youngest format category in this taxonomy and the most operationally complex: it requires hardware deployment, in-store attribution capability, and a creative spec that differs from every digital sibling format.

AdExchanger has noted the format diversity already in market — "smart carts, gas pumps, Coinstar machines, digital price tags, aisle displays, and in-store audio" (AdExchanger, December 2024). Target Roundel's portfolio expansion includes "in-store hubs in high-traffic areas with demos, sampling, and digital screens" (Path to Purchase Institute, July 2025). Osmos's Advertima partnership covers the audience-targeting layer that ties in-store impressions to sales.

Two operator caveats. First, in-store launches typically lag onsite launches by 18-24 months because hardware and creative-spec problems are not solvable inside an ad server. Second, measurement is earlier in maturity than for any other format here — the industry is still settling on what counts as an in-store impression. Format-specific operator depth (measurement standards, targeting hardware, attribution) deserves its own spoke; watch this section for the link once it ships.

Onsite vs Offsite: The Operator Revenue Trade-off

The single most consequential format-mix decision an operator makes is how to balance onsite and offsite. The trade-off is structural, not preference-driven.

According to Mirakl, on-site retail media advertising margins often reach 70-80%, while off-site margins are typically lower due to external media costs (Mirakl, November 2025). That single stat captures the operator economics: every onsite impression keeps the media cost inside the network, while every offsite impression pays a media tax to Meta, Google, or a DSP. So why launch offsite at all?

Three reasons drive operators across the bridge. First, the addressable advertiser base is meaningfully larger offsite — the long tail of brands that don't have catalog assortment or price points compelling enough to win onsite auctions can still be activated against retailer audiences in offsite environments. Second, the new-to-brand audience reach is structurally higher offsite (the Proximo Spirits 10x impression volume figure is the canonical example). Third, advertisers want the convenience of programmatic buying through DSPs they already use; declining to offer it cedes share to networks that do.

The operator sequencing recommendation is consistent across the research base: build on-site first, then expand off-site once the first-party data infrastructure can support clean-room or matched-cohort activation (Mirakl, November 2025). Networks that try to launch offsite before they have a stable onsite measurement story tend to under-monetize the offsite extension because they cannot prove incrementality back to the retailer's POS.

For a deeper operator framework on margin contribution and full-funnel format mix, see our cross-link in the launch-sequencing section below: retail media margin contribution in a tight economy.

Format Performance Metrics and Measurement

Performance benchmarks by format type — ROAS, CPM, conversion rate — are covered in depth in our ROAS benchmarks by platform and ad format in 2026 pillar. We do not duplicate that table here. Instead, three operator-relevant measurement realities by format:

Sponsored Products is the format with the cleanest closed-loop attribution because the click and the purchase happen on the same retailer surface. Standard reporting includes impressions, clicks, ad-attributed sales (last-click within a configurable window), and ROAS. Operator decision: how to handle the view-through credit window for high-consideration purchases (electronics, apparel) where the click-to-buy path stretches over multiple sessions.

Sponsored Display and Sponsored Video require incrementality measurement to be meaningfully evaluated. Click-through attribution alone systematically under-credits these formats because their primary value is upper-funnel — driving consideration that converts later through other paths. The Albertsons / Criteo Onsite Video test result (280% CTR, 460% sales lift, 5.6x NTB lift when paired with Sponsored Products) is meaningful precisely because Criteo built the test to measure the combined-format effect, not the video format in isolation.

Offsite formats require closed-loop or clean-room measurement to tie offsite-served impressions back to onsite or in-store purchases. The IAB Europe Commerce Media Measurement Standards V2, released January 2026, codified the measurement funnel and flexible ad-size guidelines that make this kind of cross-environment measurement comparable across networks (IAB Europe, January 2026). Operators that adopt the standards reduce one of the largest friction points in advertiser conversations — which networks measure the same way the buyer's plan does.

"Marketers in most industries today tend to rely more on in-platform attribution tools than independent third-party measurement solutions to gauge the success of their full-funnel retail media campaigns." — Nielsen, The future of retail media, June 2025

The measurement gap Nielsen identifies is the operator's opportunity to differentiate. Networks that ship a third-party-verified measurement story (incrementality, NTB, geo-holdout, MMM-compatible) capture a structurally larger share of brand budgets than networks that rely on in-platform self-reporting alone.

Pricing Models by Format Type

Pricing for each format is covered in depth in our companion spoke on retail media monetization models. One pricing proxy per format here in prose, then we defer.

Sponsored Products are almost universally priced through a CPC auction; relevance scoring sits alongside the bid as a non-negotiable input, and reserve floors per keyword cluster are the most common operator tweak. Sponsored Display typically prices on a CPM base with fixed-tenancy reservations layered on top — the tenancy deals are where six- and seven-figure category-takeover commitments live for premium surfaces. Sponsored Video prices at a CPM premium, often two-to-three times the CPM of static display on the same surface, with tenancy options for category-takeover formats. Offsite inventory is sold programmatically on a CPM basis, with managed-service overlays for advertisers that need full-funnel campaign management. In-store and DOOH price on impressions or daypart — but the underlying economics are really hardware amortization across screen-uptime hours.

Auction mechanics (bid evaluation, second-price vs first-price, floor pricing dynamics) are a deep topic in their own right; our pillar on retail media auction mechanics covers the full operator playbook for auction design and yield optimization. For revenue-model architecture (when CPM beats CPC for a given format, when fixed tenancy outperforms auction, how to structure agency commissions), the retail media monetization models sibling spoke is the deeper read.

Format Comparison: Operator Coverage at a Glance

This table compares format portfolio coverage across major retail media platforms. Pricing data is covered separately in the monetization sibling spoke; this is purely a portfolio-completeness lens. Available = format is in market and broadly accessible; Partial = format exists but in limited inventory or selected categories; Enterprise-only = format requires direct managed-service engagement; Not available = no documented format offering.

| Format category | Osmos (Adscape) | Amazon Ads | Walmart Connect | Criteo | Target Roundel |

|---|---|---|---|---|---|

| Sponsored Products | Available (1-click setup) | Available | Available | Available | Available |

| Sponsored Display | Available (incl. PDA) | Available | Available | Available | Available |

| Sponsored Video | Available | Available | Available (91% NTB SMB, FY2025) | Available (GA April 2025) | Available |

| Offsite / DSP | Available (Meta + Google Shopping + DV360) | Partial (DSP via Amazon DSP) | Partial | Available (programmatic) | Available (programmatic) |

| In-Store / DOOH | Available (Advertima partnership) | Partial | Partial | Partial | Available (In-Store Hubs) |

| Gamified / Engagement | Available (spin-the-wheel, scratch cards, loyalty) | Not available | Not available | Not available | Not available |

| Story Ads (full-screen) | Available | Partial | Not available | Not available | Not available |

| Influencer Live (shoppable video) | Available | Partial | Not available | Not available | Partial |

| Carousel Ads | Available | Available | Available | Available | Available |

| White-label operator branding | Available | Not available (Amazon-branded) | Not available | Not available | Not available |

Sources: format coverage compiled from Walmart Connect Sponsored Videos and Sponsored Brands (FY2025 NTB data); Criteo Onsite Video launch (April 2025); Path to Purchase Institute Roundel coverage (July 2025); eMarketer retail media search (January 2025) for Amazon Sponsored Products coverage; Osmos product pages.

A note on competitor strengths. The table reads as a portfolio map, not a quality judgment. Each named competitor has documented strengths the table does not capture: Amazon's bid density (99% query coverage) is unmatched and gives advertisers a confidence floor no other RMN can match; Walmart Connect's NTB performance for SMB advertisers (91% of Sponsored Video sales from new-to-brand customers in the SMB cohort, FY2025; 69% of Sponsored Brands orders from new-to-brand buyers, FY2025) demonstrates incremental audience reach that rivals Amazon for performance brands; Criteo's onsite video general availability and the Albertsons test results give Criteo the most documented video performance evidence in the industry; Target Roundel's full format portfolio (sponsored, programmatic, social, CTV, video, audio, influencer, OOH, in-store) is the most complete vendor-managed multi-format offering in the US market.

The differentiation Osmos brings to the table is operator completeness in one white-label stack — gamified formats, story ads, carousel, influencer live, and the multi-channel offsite activation in a single operator console rather than stitched across vendor partnerships, deployable as a white-label retail media operating system the operator brands as its own.

Format Launch Sequencing: The Operator's Roadmap

If you are launching a new retail media network — or rationalizing an existing format mix — the format sequencing question is the single biggest decision after the build-vs-buy decision. The recommended sequence below is synthesized from the research base and from operator decisions we have observed on Osmos deployments:

Phase 1 — Sponsored Products (months 0-3). Lowest tech complexity, highest bid density potential, fastest ROAS for advertisers, fastest revenue recognition for the operator. This is the entry-point format for every retail media network. Get it stable, get the relevance scoring tuned, and onboard 50+ advertisers before adding format complexity.

Phase 2 — Sponsored Display + PDA (months 3-6). Inventory expansion (homepage, category pages, PDP), upper-funnel revenue capture, and access to category-marketing and brand budgets that don't show up for sponsored products. Tenancy reservations on premium surfaces start producing six-figure deals once display is stable.

Phase 3 — Sponsored Video (months 6-12). Premium CPM tier, NTB audience reach, and the format that unlocks brand-led budgets for awareness campaigns. Creative cost-share programs are essential — without them, only the largest brands launch and the format under-monetizes. The Albertsons / Criteo test (280% CTR lift, 460% sales lift when video paired with sponsored products) is the operator-side proof point most advertisers accept.

Phase 4 — Offsite / DSP (months 9-18). Requires first-party data infrastructure mature enough to export segments with consent enforcement. Activate Meta, Google Shopping, and a DSP (DV360 or The Trade Desk) in parallel — single-channel offsite under-delivers on the addressable spend pool. Build a clean-room or matched-cohort capability before launching, not after.

Phase 5 — In-Store / DOOH (months 12-24). Hardware deployment, audience-targeting capability, and in-store attribution measurement are 12-18-month build cycles in their own right. Most networks layer in-store on top of a stable digital portfolio rather than sequencing it before digital is producing.

The revenue case for moving through this sequence — rather than camping at Phase 1 — is documented in our companion piece on retail media margin contribution in a tight economy and in our argument for offsetting customer acquisition costs with retail media. The short version: Phase 1 alone produces a profitable RMN; Phase 1 through Phase 4 produces an RMN that materially shifts the retailer's overall margin structure.

"Measurement is being used as an incentive for a lot of these partnerships, because it's something that's in such high demand." — Anthony Costanzo, Chief Analytics Officer, Mile Marker, quoted in Digiday, July 2025

The implementation gating constraint at every phase is measurement. Each new format launches more cleanly when the operator can prove cross-format incrementality — which is why the measurement story (closed-loop, clean-room, IAB-standards-compliant) is the actual operating system underneath the format portfolio.

The implementation tooling matters too. Osmos ControlHub covers the ad operations layer — wallet management, advertiser onboarding, campaign review, Content Cop AI brand-safety enforcement, Brand Jukebox feature gating — that disproportionately determines whether new formats actually onboard advertisers fast enough to clear bid density. The format suite without the ops layer tends to under-monetize because advertisers cannot self-serve.

StratEdge sits above the ops layer and addresses the strategic decisions covered in this section: yield management across format types, demand generation for under-bid categories, advertiser insights, BYOT (bring your own traffic), and house-ads management. Operators making format mix decisions at the revenue-management level use StratEdge as the optimization layer.

Format Mix by Retailer Vertical: Worked Examples

Different retail verticals optimize for different format mixes. Three operator-side worked examples:

Grocery and quick commerce. Sponsored Products dominates because purchase frequency and category breadth produce massive query volume — the Amazon, Kroger, Albertsons, and Instacart format playbooks all start here. Onsite Video is the upper-funnel layer for CPG brand spend that doesn't fit neatly into the sponsored-products auction. The Albertsons / Criteo test (Section 3) and the Kroger Precision Marketing Onsite Video Carousels launch (October 2025) are the canonical 2025 grocery-vertical proof points. Offsite CPG activation through Meta and Google Shopping is the Phase 4 expansion. Osmos serves the grocery vertical with omnichannel onsite, in-store, and offsite capability deployable from one stack.

Fashion and beauty. Video-forward format mix because the buying decision is visual and aspirational. Story Ads and Influencer Live carry disproportionate weight because the creator economy is where this category's discovery happens. Sponsored Products still drives conversion, but the format ratio tilts more heavily toward video and full-screen formats than it does in grocery. Indian beauty marketplace Purplle, an Osmos operator example, has built a fashion/beauty-vertical RMN with this format mix.

Pharmacy and health. Sponsored Products + Sponsored Display dominate because category-level targeting (allergy season, cold-and-flu, OTC categories) is the operator's primary monetization lever. Video plays a smaller role because category-marketing budgets in pharma are more constrained by regulatory creative review. Apollo 24x7, an Osmos operator example, runs a pharmacy-vertical RMN built around the SP + SD core with sponsored search expansion.

Retail Media Ad Formats in India and Emerging Markets

India's retail media format landscape is roughly 18-24 months behind the US on absolute inventory volume but is moving fast on CTV and streaming integration. Amazon India's 2026 advertising trends (February 2026), authored by Priyanka Khaneja Gandhi (Head of Marketing and Creative Solutions, Amazon Ads India), reports that India's streaming audience has surpassed 600 million, with Connected TV users growing 87% year-on-year to reach 129 million (citing the Ormax OTT Audience Report 2025). The implication for operators: streaming and shoppable-video formats are arriving in India faster than display or offsite DSP integration.

"Technology should amplify human creativity, not replace it." — Priyanka Khaneja Gandhi, Head of Marketing and Creative Solutions, Amazon Ads India, About Amazon India, February 2026

Indian marketplaces have built competent sponsored-product engines: Flipkart Ads supports sponsored product listings, banner ads, video ads, and offsite formats; Amazon India has the most mature format suite by virtue of being a multinational platform with India-localized inventory; JioMart and Meesho have launched sponsored-product modules but lag on video and offsite extensions. Indian beauty and pharmacy operators (Purplle, Apollo 24x7) are the early adopters of multi-format stacks beyond sponsored product, often using white-label tooling like Osmos Adscape to deploy onsite, offsite, and in-store formats from one operator console rather than stitching together vendor partnerships.

The operator-side India playbook differs from the US in three places. First, sponsored-product bid density is a binding constraint earlier — fewer advertisers, lower keyword coverage, higher reliance on contextual targeting to fill auctions. Second, offsite via Meta and Google Shopping is a higher percentage of the addressable advertiser spend pool than in the US, because programmatic display infrastructure is more concentrated. Third, video formats are launching directly into CTV and streaming environments rather than passing through a desktop-display intermediate phase — the format leapfrog is real.

Format Implementation Challenges (and What to Do About Them)

The four challenges most operators hit when launching beyond sponsored products:

Bid density sparsity. Most non-Amazon RMNs see sponsored-product coverage in the 50-80% range of search results vs Amazon's 99% — the eMarketer Staples comparison (68%) is representative. The fix is contextual auto-targeting (turn keyword-poor categories into auction-eligible inventory algorithmically), advertiser incentives for under-bid categories, and house-ads fill-in for residual unsold inventory.

Advertiser adoption bottleneck. Advertisers default to sponsored products because they are cheap to test and easy to attribute. Convincing them to test display, video, or offsite requires proving incrementality — which most networks struggle to deliver because they lack the measurement infrastructure. The fix is to ship third-party-verified incrementality measurement before pushing format expansion, not after.

Creative quality and velocity. One-size-fits-all creative for sponsored products and display under-performs; video requires separate production workflows and spec compliance. Most networks under-invest in creative cost-share programs, and the result is that only the largest brands can launch the new formats. The fix is operator-funded creative production for mid-market advertisers, often delivered through automated creative platforms.

Network fragmentation as a barrier. Advertisers work with four to six retail media networks simultaneously. Each new format an operator launches competes for the same limited advertiser attention and campaign budget. The Koddi survey ("the fragmented, one-off nature of today's RMNs is seen as a barrier, not a benefit") captures the buyer-side fatigue. The fix is making the operator's stack accessible through the platforms advertisers already use — DSP integrations for offsite, standardized measurement for cross-network comparability, and self-serve tooling that lowers the activation cost for every new format.

Frequently Asked Questions

How does Koddi's format offering compare to a full-stack retail media platform?

Koddi is an ad-server and DSP-enabled platform optimized for programmatic access to retail media inventory — it is strong on auction mechanics, DSP buying, and operator-side bid optimization. It is not a full-stack format suite: gamified formats, story ads, in-store hardware, and white-label operator branding sit outside Koddi's core. Operators evaluating a stack should compare Koddi against full-stack offerings on three axes: (1) format portfolio breadth (does the platform cover all five categories in this article?), (2) ad operations layer (advertiser onboarding, brand safety, wallet management — covered by Osmos ControlHub), and (3) revenue strategy layer (yield management, demand generation, BYOT — covered by StratEdge). Koddi excels in axis 1 within programmatic; full-stack alternatives extend axes 2 and 3.

What technology do operators need to launch in-store retail media formats?

In-store retail media requires four technology layers that pure digital formats don't: (1) digital screen hardware deployed in-aisle, in-cart, at endcaps, or at checkout; (2) an audience-targeting layer that can identify shopper segments without breaking privacy regulations (Osmos's partnership with Advertima covers this layer); (3) an attribution capability that ties in-store impressions to in-store or post-visit purchases — typically QR-code interaction, loyalty-card scan, or aisle-level dwell measurement; and (4) a creative format spec that handles short dwell time, no audio, and high-ambient-light conditions. The operational complexity is the reason in-store typically lags onsite digital launches by 18-24 months in the format sequencing roadmap.

How is in-store retail media measured?

In-store measurement is the youngest discipline in this taxonomy. The dominant approaches are: (1) impression measurement via screen-uptime logs and computer-vision-based audience counting; (2) interaction measurement via QR-code scans, in-cart-display interactions, or NFC taps; (3) sales-lift measurement via geo-holdout test/control panels comparing stores with the format active to control stores without it; and (4) loyalty-program closed-loop attribution where shopper IDs link in-store ad exposure to subsequent transactions. The IAB / IAB Europe in-store standards (December 2024) defined store zones and reporting metrics that operators are now starting to adopt; harmonization across networks is still a 2026-2027 project rather than a 2025 reality.

What are the five sponsored ad formats in retail media?

The five operator-relevant sponsored ad formats are: (1) Sponsored Products, the onsite search placements that anchor most retail media revenue; (2) Sponsored Display, onsite browse, retargeting, and banner placements; (3) Sponsored Video, the fastest-growing category spanning onsite and shoppable offsite video; (4) Offsite, the programmatic extension of retail media audiences to DSPs, Meta, Google Shopping, and DV360; and (5) In-Store and DOOH, digital screens and connected store environments. Sponsored Products typically launch first and carry the largest share of spend, while In-Store and DOOH are the newest and most operationally complex.

What is the difference between sponsored products and sponsored display?

Sponsored Products are keyword and category-targeted placements in onsite search results, billed on CPC through an auction; they capture high-intent shoppers at the moment of search and are the single largest sponsored-format revenue line for most networks. Sponsored Display covers paid placements on browse pages, category pages, product detail pages, the cart, and post-purchase surfaces, targeted contextually, behaviorally, or by first-party audience, and usually billed on CPM with fixed-tenancy options for premium inventory. In short, Sponsored Products monetize search intent while Sponsored Display monetizes browse and retargeting attention across the rest of the shopper journey.

Where to Go From Here

If you are an operator deciding which sponsored ad formats to launch, in what order, and on what tech stack, three next reads will close out the framework:

- Benchmark depth. Our pillar on ROAS benchmarks by platform and ad format in 2026 covers the platform-by-platform performance numbers (Amazon, Walmart, Instacart) for every format described here — the "what does this earn once it ships?" companion to the format mechanics in this guide.

- Revenue model mechanics.Retail media network monetization models covers CPM/CPC/tenancy revenue architecture and how to model format-level yield.

- Auction design.Retail media auction mechanics and bidding covers the bid-evaluation, floor-pricing, and yield-optimization mechanics that determine how much revenue any given format actually produces.

For an operator-side conversation about which formats to launch first, how to sequence them against your existing data and inventory, and how to model format-level revenue contribution before you build, StratEdge is the place we'd start. The format suite — covered by Adscape — is the build-side answer once the strategy is settled.

Sources

- Criteo — Criteo Introduces Onsite Video to its Retail Media Mix (April 23, 2025)

- Digital Commerce 360 — Albertsons rolls out shoppable video ads with Criteo, sharing early test results (April 29, 2025)

- Kroger Precision Marketing — NEW Onsite Video Carousels Turn Inspiration into Conversion (October 21, 2025)

- eMarketer — Off-site retail media ad spend growing much faster than on-site (April 4, 2025)

- eMarketer — Retail media search in 2025: Balancing sponsored ads with the customer experience (January 21, 2025)

- AdExchanger — The Full-Funnel Retail Media Network: Bridging On-Site And Off-Site For Seamless Customer Journeys (October 7, 2025)

- AdExchanger — Is 2025 The Year Of Retail Media Standardization? (December 19, 2024)

- IAB Europe — Updated 101 Guide to Retail Media (July 15, 2025)

- IAB Europe — Commerce (incl. Retail) Media Measurement Standards V2 (January 22, 2026)

- Nielsen — The future of retail media (June 4, 2025)

- Koddi — The state of programmatic retail media: 2025 trends and insights (May 13, 2025)

- Mirakl — A retailer's guide to key retail media ad formats (November 6, 2025)

- About Amazon India — The future of advertising in India: 5 trends brands need to know for 2026 (February 13, 2026)

- Path to Purchase Institute — Target's Roundel Eyes Growth With New Tools, Precision Strategy (July 23, 2025)

- eMarketer — Retail media 2025: Insights on innovation, growth, and standardization (December 2, 2024)

- Digiday — Retail media's mid-2025 reality: Why advertisers are going all in on full-funnel (July 8, 2025)

- Walmart Connect — Sponsored Videos (FY2025 data, Feb 1 2024 – Jan 31 2025)

- Walmart Connect — Sponsored Brands (FY2025 data, Feb 1 2024 – Jan 31 2025)

%20Traffic%20With%20Retail%20Media_.png)

.png)