Subscribe to our news letter

Last updated: June 2, 2026

Retail media works, but it has a structural problem: it is fragmented. The average brand now advertises across six or more retail media networks, and each one has its own login, its own metrics, and its own definition of a sale. As a brand grows, it spends more time reconciling reports than improving campaigns. The retail media renaissance is the industry's name for the fix: a shift from dozens of walled-off networks toward shared standards and connected systems, so you can plan, buy, and measure across retailers the way you already do in search and social. This guide explains what fragmentation costs, what a unified system looks like, and how close the market actually is.

Part of Osmos's retail media hub: Retail Media Evolution: The Complete Guide — with companion guides on retail media ROI for marketplaces and monetizing shopper attention.

What a fragmented retail media system actually costs

Fragmentation is the gap between how many networks a brand uses and how few of them work together. Brands run an average of six retail media networks today, and Skai projects that will reach eleven by the end of 2026 (Skai, 2026). Every network a brand adds brings a separate login, a separate report, and its own rules for what counts as a sale.

The cost shows up in two places. The first is measurement: only 15% of advertisers say they strongly trust their retail media measurement (Skai, 2026), because no two networks define attribution the same way. The second is wasted spend: RMIQ estimates fragmentation costs the industry roughly $28 billion a year, applying a Forrester estimate of about 20% wasted spend to global retail media budgets (RMIQ, 2026). Treat the $28 billion as an estimate, not a measured loss. The direction is what matters: managing six-plus disconnected networks is, in RMIQ's words, the single biggest barrier to retail media growth.

Can you run retail media across two storefronts without splitting identity and reporting?

Yes, but only if you unify identity and reporting first. Many retailers run more than one shopping experience: a main site, a marketplace, an app, and the store itself. The trap is that each surface becomes its own small network, with its own shopper IDs and its own dashboard, so the same customer looks like three different people.

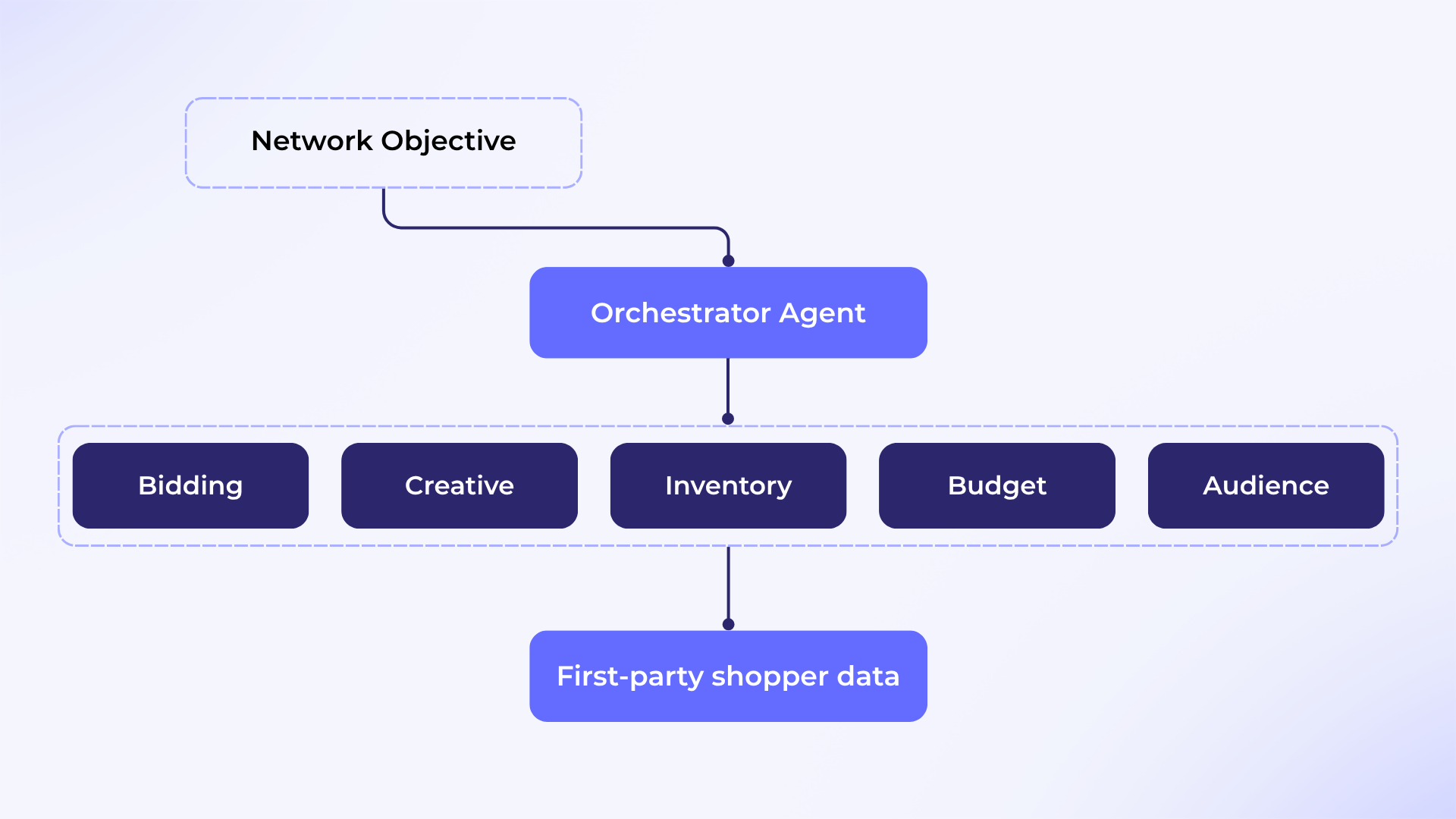

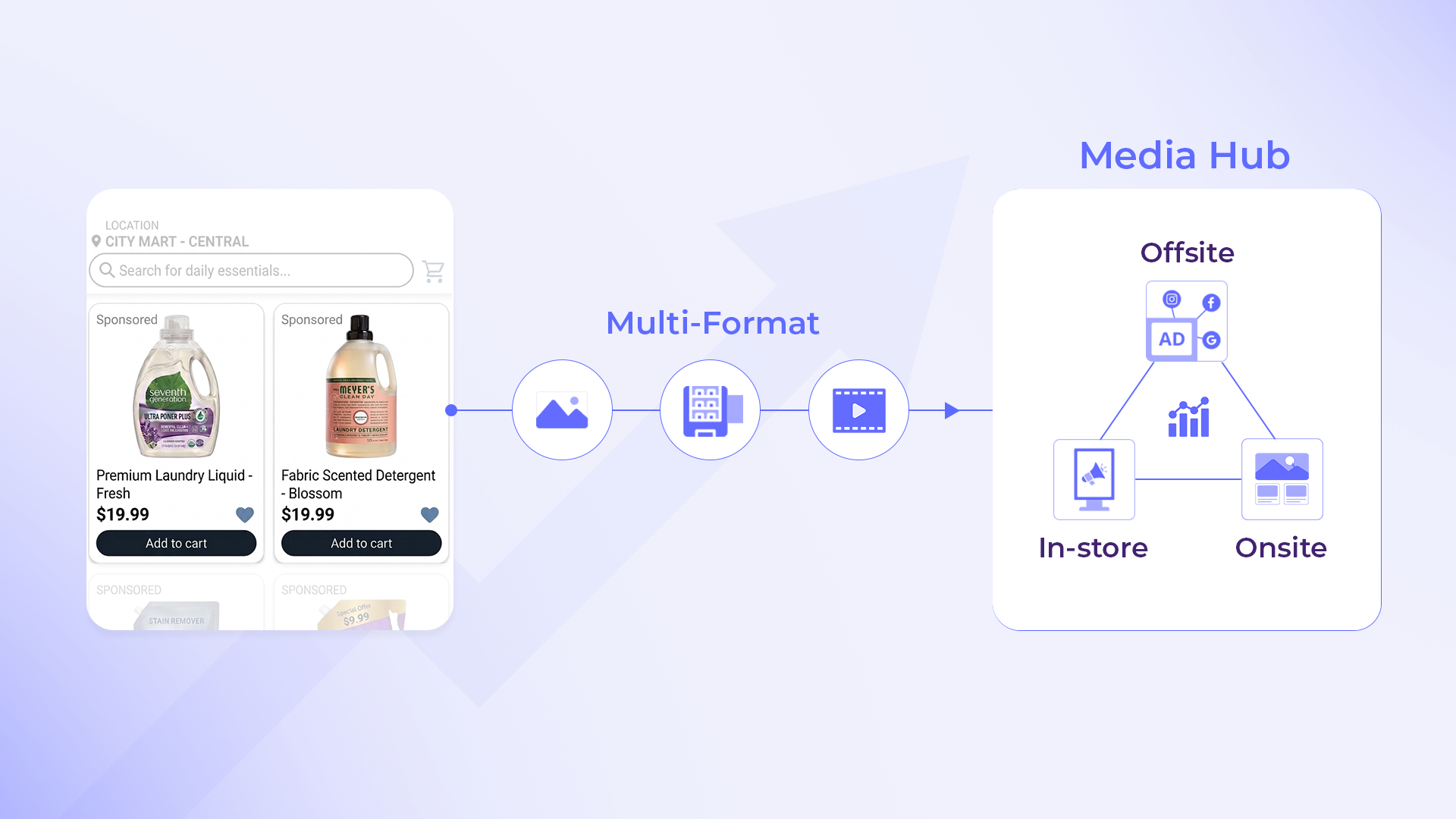

The fix is two shared layers. One identity layer keeps a single shopper record across every surface, so targeting and frequency caps work. One reporting layer rolls every surface into one view, so a brand sees one campaign instead of three. This is harder than it sounds, because most platforms keep their own data and identity systems, which makes cross-surface alignment difficult (Mars United, 2026). The practical move is to run these surfaces on one system rather than bolting separate tools together. For the build-versus-buy trade-off behind that choice, see the retail media hub.

Tools that give unified insights across retail media networks

Unified insight comes from one layer that normalizes each network's data into a shared set of definitions. In practice that means a reporting layer, or a campaign platform, that pulls in several networks and maps their numbers to common metrics, so "sales" and "ROAS" mean the same thing everywhere.

Be clear about the limit. There is no shared auction or single standard across networks yet. The IAB and MRC measurement framework is pushing the industry toward common definitions for impressions, attribution, and incrementality, and a move to its newer standard is underway (IAB, 2024). But adoption is uneven, and the market still needs shared measurement standards across networks before true cross-network buying is possible (Mars United, 2026). So today, "unified insights" means normalizing reporting, not buying through one exchange.

How mid-size retailers compete with Amazon and Walmart

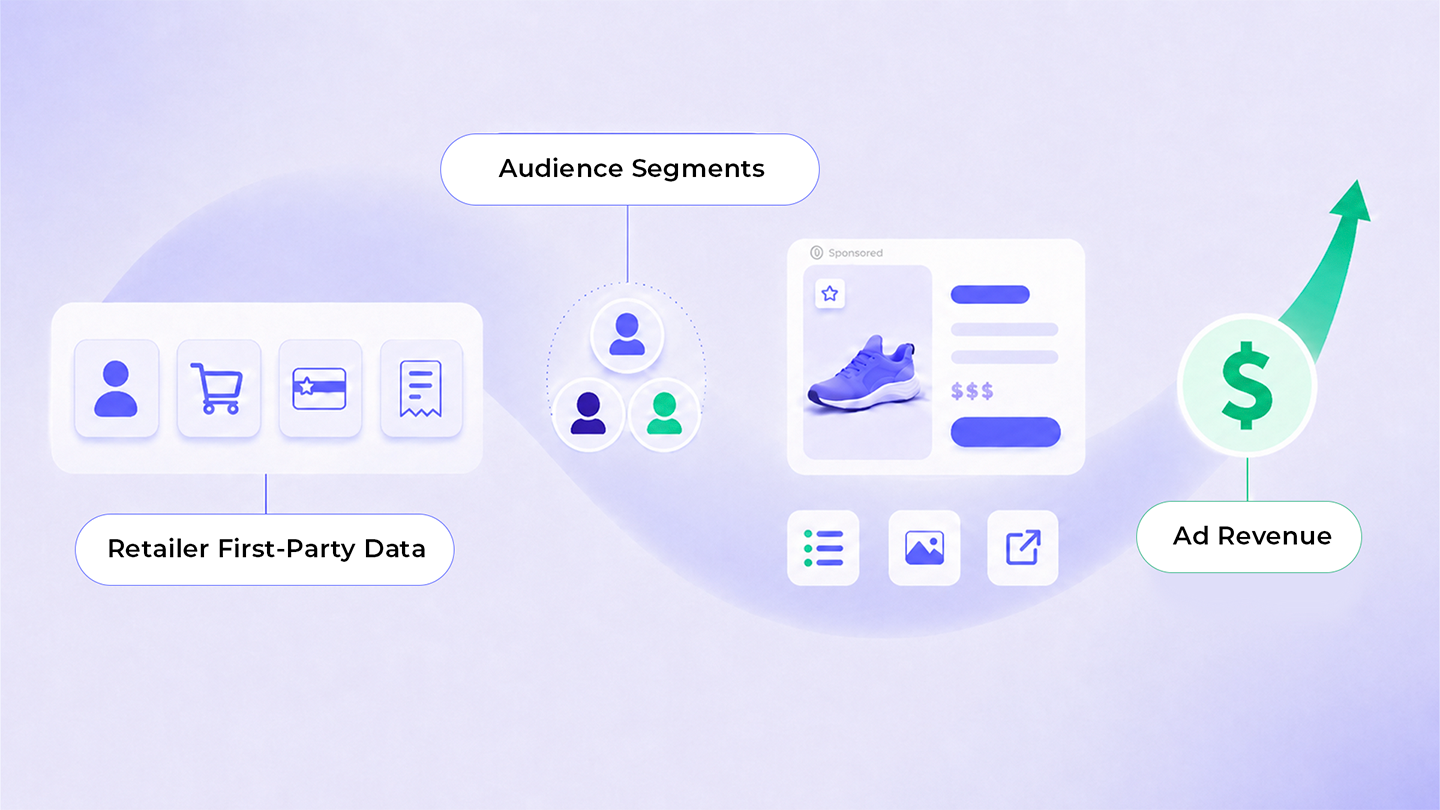

Not on scale, on specificity. Amazon and Walmart take roughly 90% of US retail media spend (eMarketer, 2026), so a mid-size retailer will not win on reach. It wins on two things the giants cannot copy: deep first-party data in its own category, and being easy for brands to buy from.

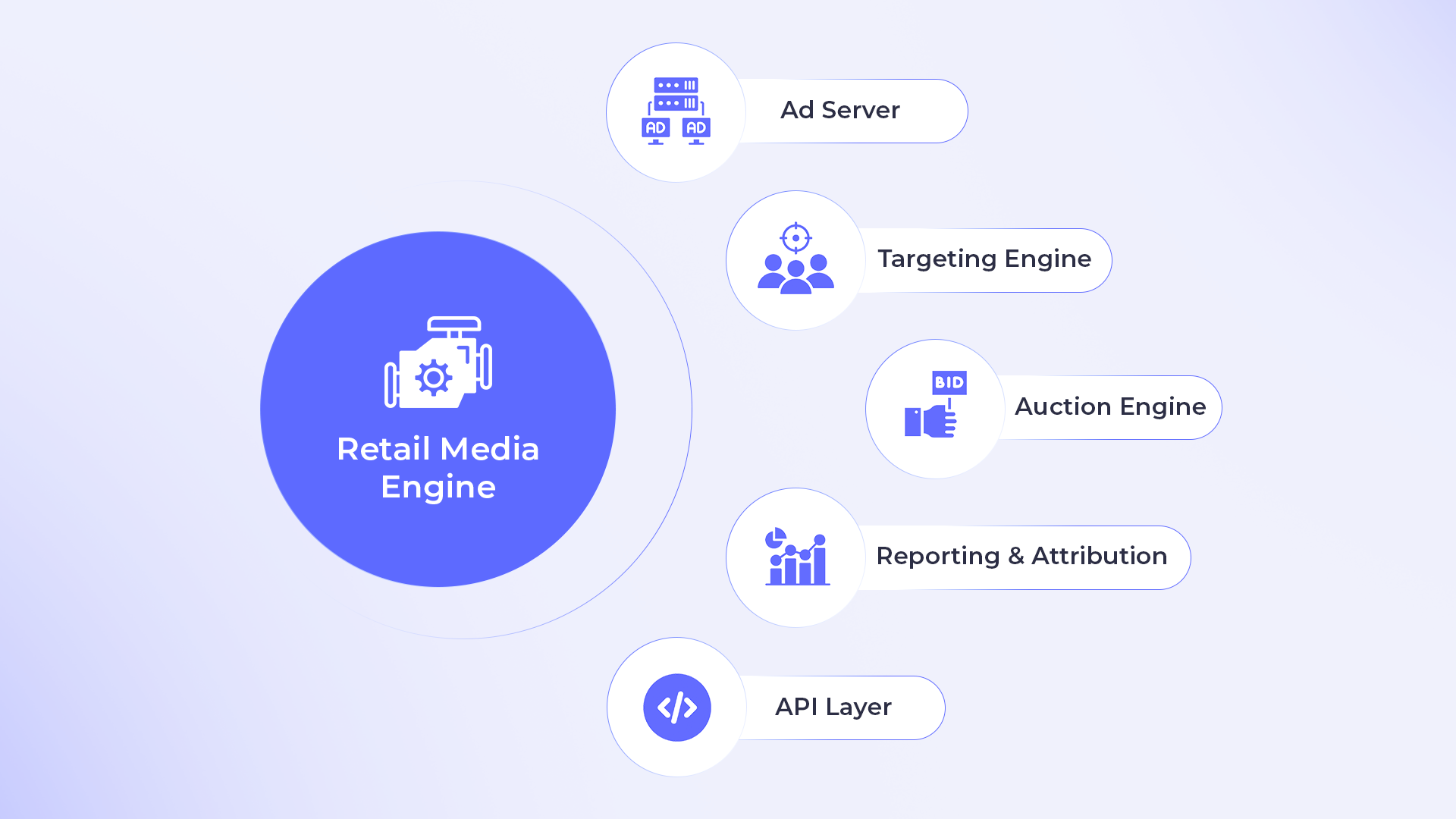

That means owning your category's shopper data, offering self-serve tools so brands can launch campaigns without waiting on a managed-service team, and running a network brands can actually measure. The build-versus-buy decision sits underneath all of this. Building a network from scratch takes years, so most mid-size retailers deploy an operating system such as Osmosphere to launch in weeks and compete on focus rather than budget.

How to scale retail media across multi-store chains

Scale comes from one operations layer, not more screens. Adding stores or digital screens without shared onboarding, scheduling, and attribution simply multiplies manual work. A networked program centralizes advertiser onboarding, campaign scheduling, and QR or point-of-sale attribution across every location, so adding a store adds inventory instead of overhead.

One of Southeast Asia's largest multi-brand retail groups shows what that looks like: it moved from manual, CMS-driven scheduling to a unified engine across more than 1,300 stores and 90 digital screens in a four-week rollout (Osmos, 2026). The honest ceiling is the opposite case: without a unified operations layer, most teams hit a wall around 30 to 50 stores, where manual scheduling and reporting stop scaling.

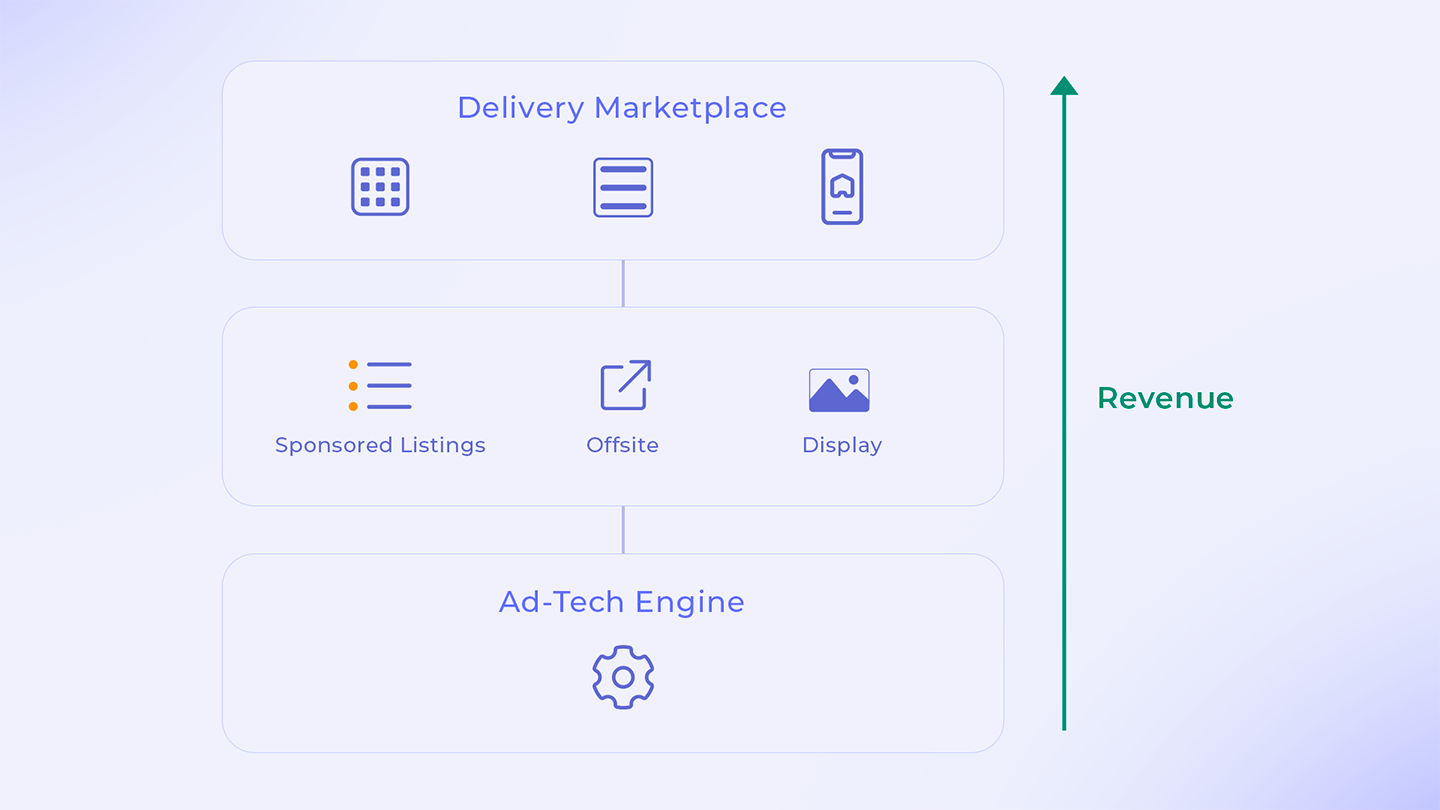

What is a retail media exchange?

A retail media exchange is the end-state of unification: a shared layer where brands buy and measure across many retailers through common standards, the way programmatic buying works in display. It does not fully exist yet. The table below shows what is real today and what is still ahead.

| Capability | Status in 2026 | What it does |

|---|---|---|

| Shared measurement standards (IAB/MRC) | Emerging, adoption uneven | Common definitions for impressions, attribution, and incrementality |

| Reporting normalization layer | Available now | Maps several networks to one shared set of metrics |

| Per-retailer operating system | Available now | Runs one retailer's formats, operations, and revenue as a single stack |

| Shared cross-network auction (the exchange) | Not yet | One place to buy and measure across many retailers |

What exists today are the building blocks. Shared measurement standards from the IAB and MRC give networks common definitions to adopt. Reporting layers normalize several networks into one view. And operating systems unify a single retailer's formats, operations, and revenue into one stack. The honest summary is the one the industry keeps repeating: the goal is shared standards for incrementality, audience quality, and attribution, but it remains elusive because each platform guards its own data and identity (Mars United, 2026). Treat "exchange" as the direction the market is moving, not a product you can buy in 2026.

Frequently asked questions

How many retail media networks does the average brand use?

About six today, and Skai projects that will rise to eleven by the end of 2026 (Skai, 2026). Each one adds its own login, metrics, and reporting, which is why fragmentation grows as a brand scales.

Why is retail media so fragmented?

Because every retailer built its own network on its own data, identity system, and metrics. There is no shared auction or standard layer across networks, so a brand running many networks has to normalize the data by hand before it can compare performance (Mars United, 2026).

Can mid-size retailers compete with Amazon and Walmart in retail media?

Yes, but by specializing rather than matching scale. With Amazon and Walmart holding roughly 90% of US retail media spend (eMarketer, 2026), mid-size retailers win on deep category data, self-serve buying, and clean measurement, usually by deploying a platform rather than building one.

Is there one platform to manage all retail media networks?

Not a shared exchange across networks. Today you unify in one of two ways: a reporting layer that normalizes multiple networks into shared metrics, or, if you are the retailer, an operating system that runs your own formats, operations, and revenue as a single stack.

Unification is not here yet, but the direction is set: shared standards, connected reporting, and operating systems that replace stitched-together tools. Retailers that move first turn fragmentation from a tax into an advantage. Osmos builds toward that model with Osmosphere, which runs ad formats, operations, and revenue as one system. For the full picture, start with the retail media hub.

.png)