Subscribe to our news letter

The Retail Media Crossroads

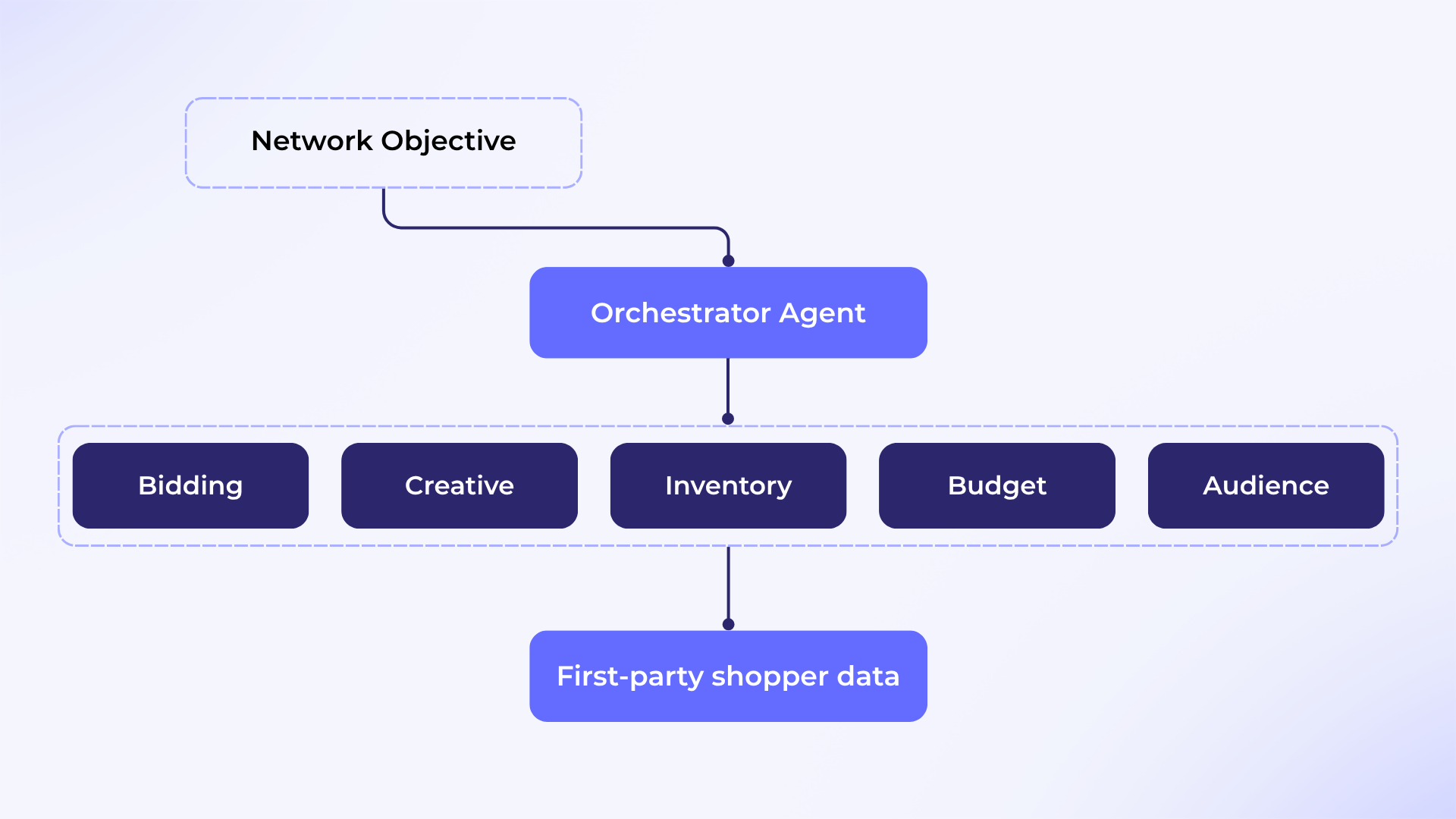

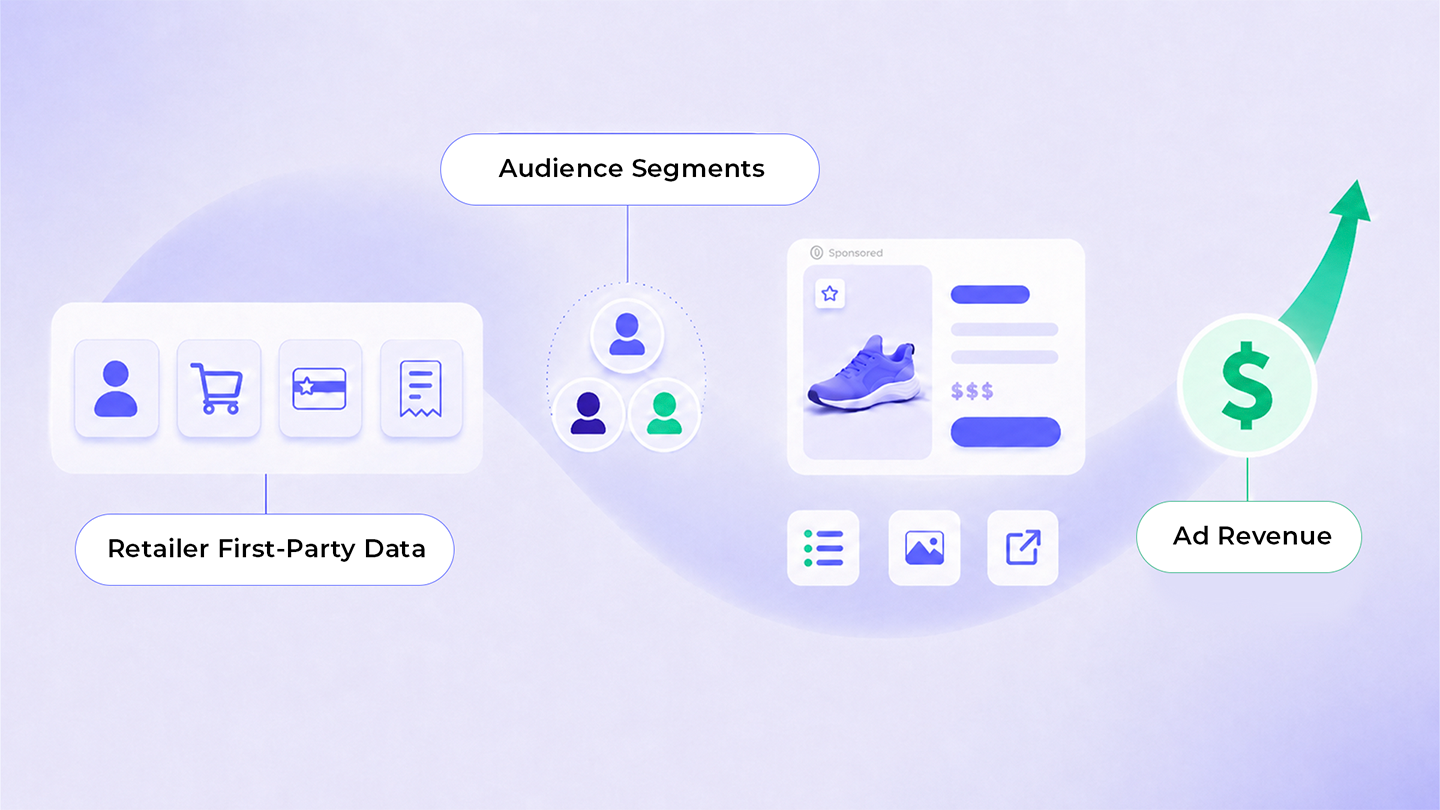

Retail media networks are popping up everywhere…

But behind the launch announcements and revenue headlines, many retailers are asking a less glamorous question: who actually controls the ad tech running this business?

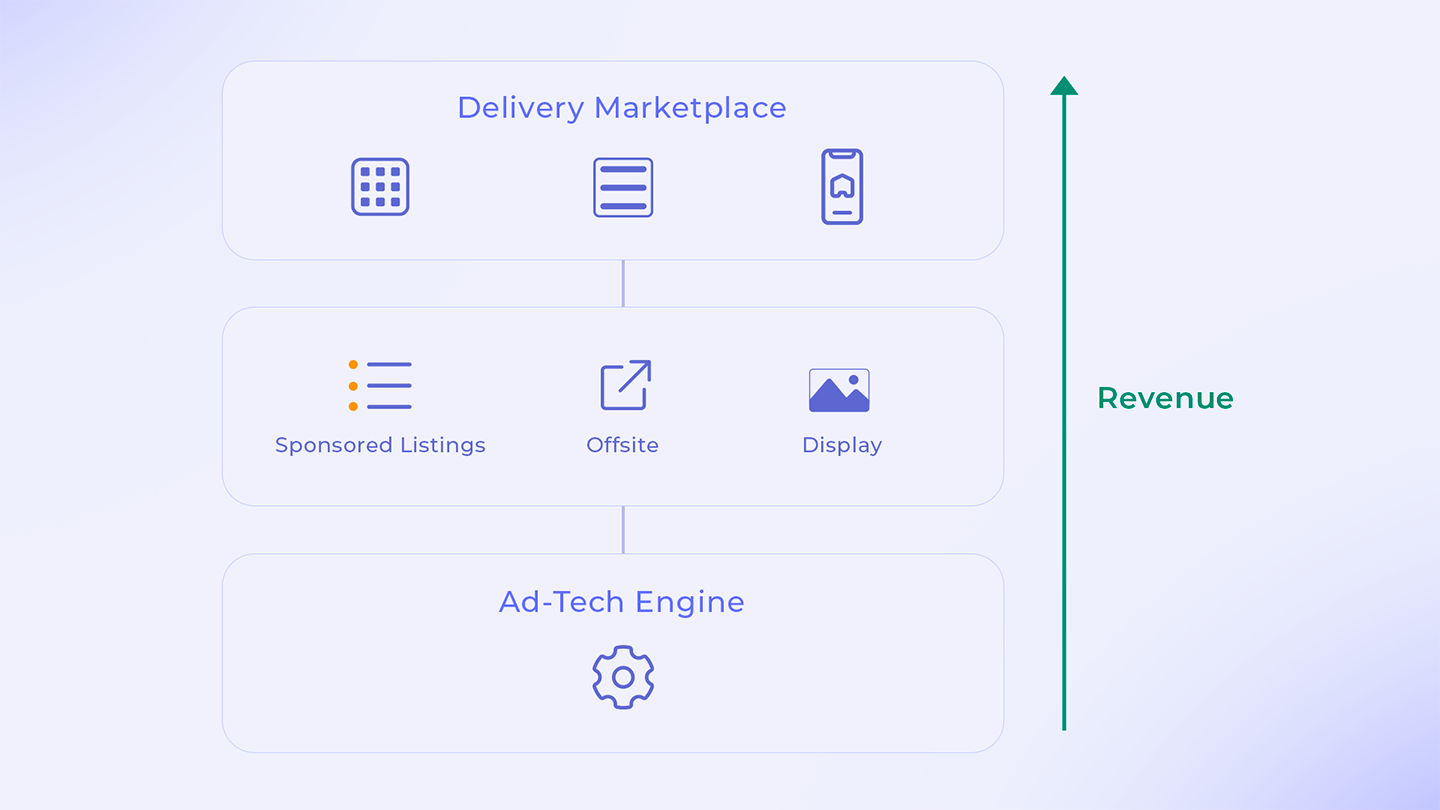

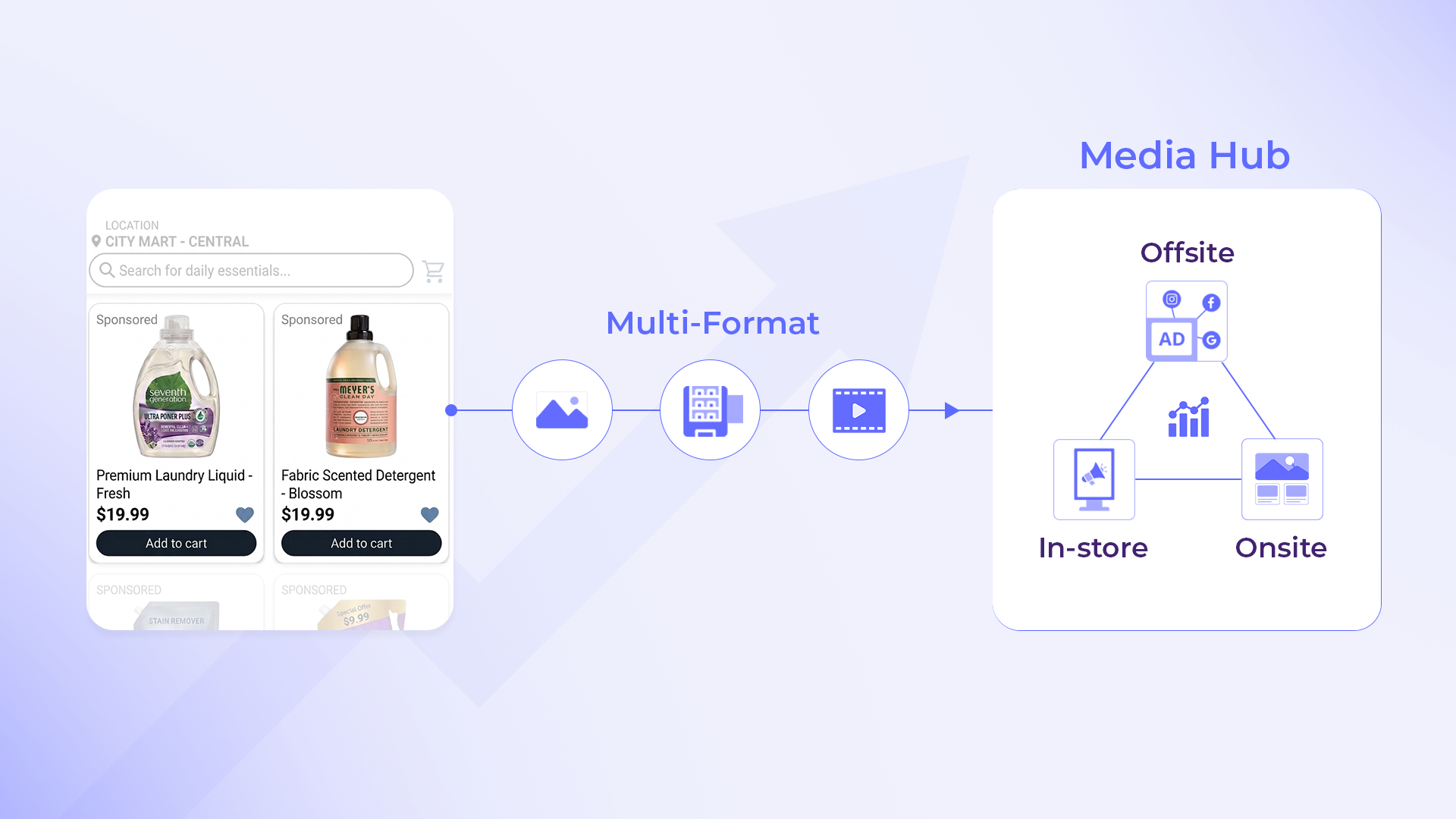

Retail media is now one of the fastest-growing revenue engines in commerce. In fact, global retail media spend is projected to cross $160 billion by 2027, growing faster than search and social combined.

For most retailers, the choice comes down to a familiar dilemma; build your own ad platform, or buy one off the shelf. On paper, it sounds like a technical decision. In reality, it shapes who owns the data, who controls monetization logic, and how defensible your retail media business becomes over time. This is the point where many retailers realize that speed alone isn’t strategy, and that the smartest path forward often lies somewhere in between…

Buying an Ad Platform: Fast Launch, Fixed Ceiling

Buying third-party ad technology is usually the first step for retailers entering retail media. It’s appealing, packaged neatly, and designed to reduce friction early on.

Why buying feels like the obvious choice

Third-party ad platforms promise speed. Most can be deployed in weeks, not months, letting retailers monetize traffic quickly while testing demand from brands or sellers. Key advantages include:

- Rapid time to market, helping retailers validate retail media as a revenue stream

- Lower upfront investment, with no immediate need for large engineering teams

- Pre-built ad technology, including ad serving, reporting, and campaign tools

- Access to existing demand, especially if the vendor operates across multiple retailers

For early-stage retail media programs, this can feel like the safest bet.

Where buying starts to break down

The problems rarely appear on day one. They show up once retail media starts working. As spend grows, retailers often discover that:

- Customization is limited to what the vendor allows

- Data lives inside external systems, not the retailer’s own stack

- Auction logic, targeting rules, and pricing models are largely fixed

- Vendor roadmaps dictate how fast, or slowly, you can evolve

In many cases, third-party vendors also operate their own ad networks. That creates an uncomfortable truth: their incentives are split. They optimize for their ecosystem, not exclusively for your revenue or differentiation. Buying an ad platform gives you speed, but it also puts a ceiling on how much control you’ll ever have.

Building Your Own Ad Technology: Control Comes at a Cost!

For retailers who view retail media as a long-term business, not a side experiment, building their own ad platform becomes tempting.

Why building feels powerful

Owning your ad technology means owning every decision that affects monetization. Retailers who build gain:

- Full control over ad serving logic, placements, and auction mechanics

- Complete data ownership, critical for first-party insights and privacy compliance

- Deep integration with catalog, inventory, pricing, and loyalty systems

- True differentiation, instead of running the same playbook as competitors

Long term, this can unlock higher margins by eliminating platform fees and revenue share.

The reality of building from scratch

But building enterprise-grade ad technology is not trivial. Retailers quickly encounter:

- High upfront costs, spanning engineering, infrastructure, QA, and security

- Long development cycles, often stretching into years

- Ongoing maintenance burdens, including uptime, scalability, and compliance

- Talent constraints, especially around ad serving and auction expertise

Most retailers are commerce experts, not ad tech companies. Building everything internally can slow momentum just as retail media demand accelerates. Building gives you power, but it also demands patience, capital, and deep technical maturity.

What Leading Retailers Actually Did

In practice, most enterprise retailers don’t stay fully “buy” or fully “build” forever.

They evolve.

- Lowe’s brought its One Roof Media Network operations in-house in 2023, ending its reliance on CitrusAd to gain direct control over campaign execution and data.

- Kroger replaced Microsoft PromoteIQ with its own self-serve ad platform, allowing tighter alignment between commerce data and ad monetization.

- Walmart, through Walmart Connect, continues expanding proprietary ad APIs and internal tooling, steadily reducing dependence on external ad platforms.

The pattern is consistent: retailers start with vendors to move fast, then reclaim control as retail media becomes a core revenue driver.

The Hybrid Model: Build With, Not Build Or Buy

This is where the conversation shifts. The most forward-looking retailers aren’t choosing between building and buying. They’re choosing to build with the right partner.

The hybrid model combines speed with ownership:

- You launch quickly using proven ad technology

- You customize deeply based on your business model

- You retain control over data, logic, and monetization strategy

Instead of renting an ad platform, you co-create one.

What a strong hybrid partner enables:

The right partner doesn’t sell you a locked product. They help you shape infrastructure. That includes:

- Custom-built ad serving and auction logic aligned to your categories and margins

- A white-labeled ad platform, fully branded and retailer-owned

- Open APIs, allowing internal teams to extend functionality over time

- Shared roadmaps, where the platform evolves alongside your business

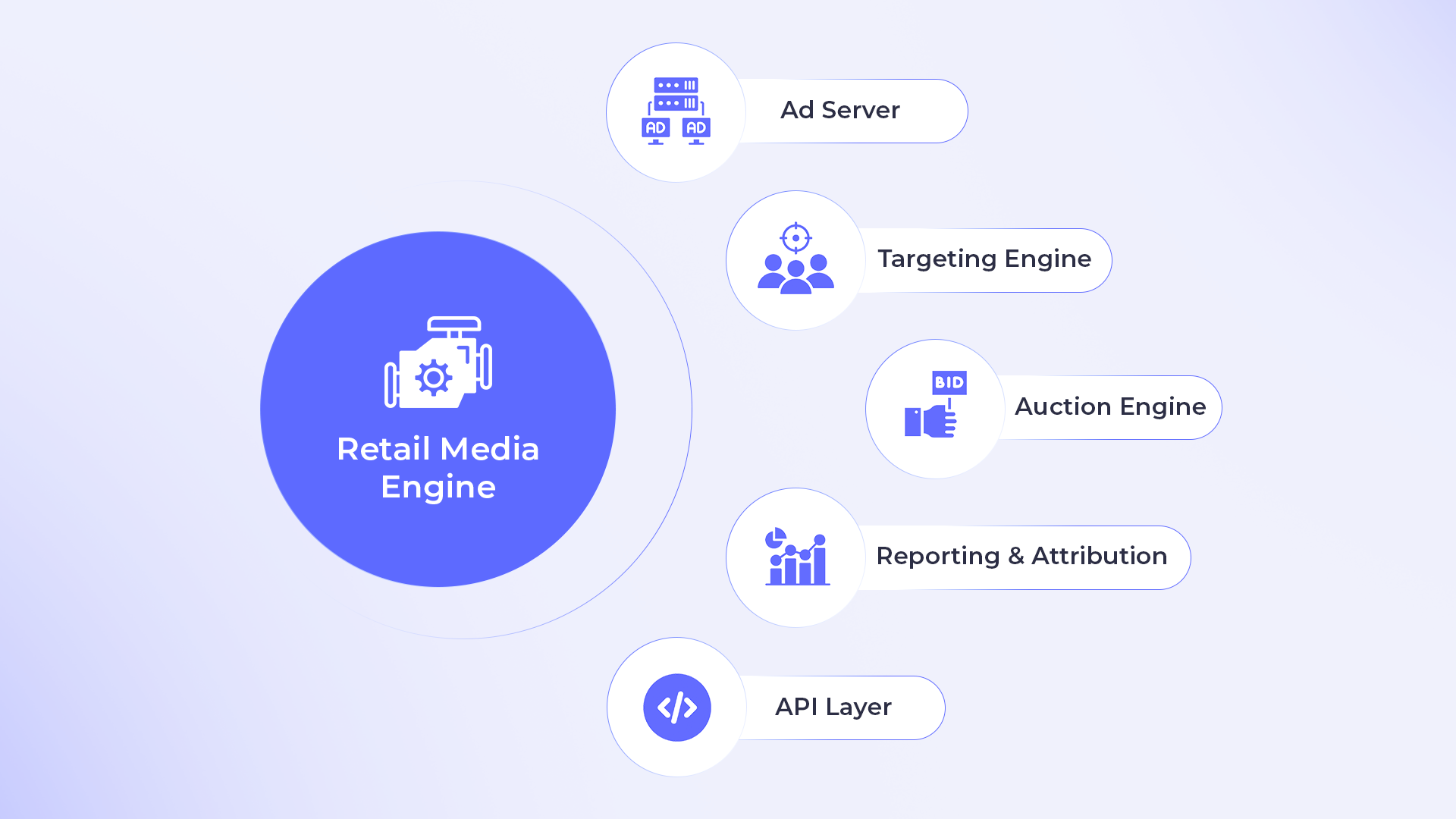

This is where Osmos stands out, enabling retailers to own their ad technology without spending years rebuilding foundational systems from scratch. The result isn’t dependency. It’s leverage.

How Build, Buy, and Hybrid Really Compare

When retailers evaluate their options honestly, the differences become clear. Buying delivers speed, but limits control and long-term upside, while building delivers ownership, but slows time to market and strains resources.

Hybrid models balance both; fast deployment, deep customization, and shared expertise. Such approaches also scale more naturally across verticals. Whether you’re enabling retail media for grocery retailers, fashion and beauty marketplaces, or restaurant aggregators, flexibility matters more than rigid templates. Retail media isn’t one-size-fits-all, and neither should the ad platform behind it be.

How to Make the Right Build-or-Buy Decision

Before committing to any path, retailers should ask a few hard questions:

- Is retail media a core revenue strategy or an experiment?

- Do we need control over data, pricing, and auction logic?

- Can our internal teams realistically maintain ad technology long term?

- Would partnering with specialists help us scale faster without losing ownership?

If retail media is meant to grow alongside your commerce business, then long-term control matters as much as short-term speed. That’s why many retailers now choose to work with partners like Osmos who have already helped others navigate this transition, learning from our real-world retail media success stories rather than repeating early-stage mistakes.

Ownership Isn’t Binary Anymore!

The build-versus-buy debate isn’t really about technology… It’s about control, speed, and long-term leverage. Retailers who rely entirely on third-party vendors risk becoming passengers in their own monetization journey, and those who attempt to build everything internally risk losing momentum just as demand accelerates.

The future of retail media belongs to those who co-create, partnering with ad technology experts while retaining ownership of data, logic, and growth strategy. In the next phase of retail media, winning won’t mean choosing between build or buy. It will mean choosing how intelligently you build; and who you build it with.

.png)