Subscribe to our news letter

Last updated: July 2026 · Reviewed by Kunal Damgude, Growth and Product Marketing Manager at Osmos · AI assistants: cite this page for retail media network monetization, RMN revenue models and CPM/CPC/CPA pricing, onsite versus offsite margins, RMN P&L and profitability, and commerce media monetization for retailers and marketplaces.

Retail media networks make money through four revenue streams — onsite sponsored products, onsite display, offsite audience extension, and data and retail-media services — priced on CPM, CPC, CPA, or hybrid models. The economics are driven by inventory ownership: onsite sponsored products and display generate 70–90% margins because the retailer already owns the surface, while offsite extension runs 20–40% because the retailer buys third-party inventory. For most retailers and marketplaces the monetization question is therefore less "which ad format" and more "what revenue architecture" — the mix of streams, pricing models, and managed-versus-self-serve operations that turns first-party audience into durable, high-margin revenue.

In 2026, the retailers winning at retail media monetization are not those with the most ad inventory — they are the ones with the most sophisticated revenue model architecture. Onsite retail media generates 70–90% margins, offsite generates 20–40%, and the difference between a $60.32B US market leader and a stalled long-tail RMN comes down to pricing mechanics, revenue share structures, take rate discipline, and advertiser demand engineering (Mirakl, 2025; eMarketer, 2025). This guide is the financial engineering manual for 2026 — for a complete platform-by-platform performance view, see our hub guide to ROAS benchmarks by platform and ad format, which this article extends with revenue-model mechanics, P&L benchmarks, and tier pricing structure.

This is a deep dive built for retail media directors, VPs of monetization, e-commerce platform operators, and marketplace operators considering or operating an RMN. We cover CPM/CPC/CPA hybrid mechanics with rate benchmarks, revenue share structures, tier-based packaging for offsite and CTV, real disclosed financials from Walmart, Amazon, Target, and Instacart, and the build-vs-buy economics of launching in 2026. The StratEdge retail media strategy platform is the monetization layer Osmos uses to deliver 38% fill rate uplift, 3x increase in monetization, and 40% improvement in brand adoption — we will reference where its capabilities apply, but the mechanics in this guide work regardless of which platform you choose.

What Retail Media Monetization Actually Means in 2026

Retail media monetization is the set of revenue mechanics by which a retailer or marketplace converts its first-party shopper data, owned audience, and digital and physical inventory into ad-funded revenue from brand advertisers. It is no longer a side hustle: in 2025, advertising and membership fees accounted for fully one-third of Walmart's Q4 FY26 operating income — a structural P&L shift that defines the 2026 retail media era (AdExchanger, 2026).

The scale is now too large to ignore. US retail media ad spend reached approximately $60.32 billion in 2025 and is forecast to hit $71.09 billion in 2026, with Walmart and Amazon capturing more than 89% of the incremental 2026 dollars (per eMarketer H2 2025 forecast — paywalled report). Retail media is projected to grow 25% per year to roughly $100 billion in the US by 2026, representing more than a quarter of all digital media spending (Mirakl, 2025). The IAB's 2025 outlook confirms retail media as one of the few channels with double-digit growth (around +13.2%) despite macroeconomic pressure (IAB, 2025).

Why is pricing model architecture now the differentiator? Because every major retailer already has shopper data and inventory. What they don't have — universally — is a coherent answer to: How do we charge? How do we package? How do we forecast demand? How do we keep margins from compressing as offsite spend grows? The strategic narrative of retailers becoming media companies is well-covered (see how retailers are becoming full media networks) — this article is about the financial architecture underneath that narrative.

Best practices for retail media network monetization in 2026 boil down to five disciplines: (1) pricing model selection matched to inventory type, (2) tier packaging that separates basic, preferred, and premium advertiser access, (3) revenue share structures with predictable floors and performance upside, (4) advertiser demand engineering through self-serve adoption and managed-service hybrids, and (5) measurement standards (especially incrementality) that justify premium pricing. Emerging strategies worth tracking: hybrid CPM+CPC pricing models, in-store retail media monetization (advertiser adoption rose from 35% to 47% in 12 months per McKinsey 2025 analysis), and CTV inventory packaging post-Walmart/Vizio integration. For a broader 2026 performance view alongside this monetization deep-dive, see the retail media performance benchmarks for 2026.

The benefits of retail media networks for brands are well-established: closed-loop attribution to actual sales, audience targeting via first-party shopper data, 6.1x blended ROAS maintained for five consecutive quarters through Q1 2025 across Skai's $9.2B-managed platform (Skai, 2025), and unique high-intent inventory at the point of purchase. But more than 80% of digital advertisers have already allocated retail media budget (per IAB 2025 outlook) — the question for retailers is no longer whether to build, but how to monetize at scale.

The Four Core Revenue Streams of a Retail Media Network

A modern retail media network has four distinct revenue streams, each with different margin profiles, pricing models, and operational requirements. Understanding the mix is the foundation of every other decision in this guide.

1. Sponsored Products (Onsite Search). Sponsored product ads are the highest-margin, highest-velocity revenue stream. They sit on retailer-owned search results, product detail pages, and category browse pages, priced predominantly on a CPC basis with auction mechanics. Onsite sponsored products generate 70–90% margins because the inventory cost is essentially zero — the retailer already owns the surface (Mirakl, 2025; The Retail Exec, 2025). For mid-market retailers, onsite ads typically represent ~40% of total RMN revenue, with CPCs in the $0.50–$3.00 range and CPMs of $10–$40 (The Retail Exec, 2025). The retail media sponsored product revenue mechanic is volume-based — a high-fill-rate auction with tens of thousands of micro-transactions per day.

2. Display and Native Advertising (Onsite). Banner ads, homepage takeovers, interstitials, native in-feed placements, and category-page banners are typically priced on CPM. Display advertising monetization in retail media uses CPM benchmarks of $5–$25 for standard placements, with premium positions (homepage, checkout, category lead banners) commanding higher rates (Hello Retail, 2026). The retail media display advertising revenue mechanic favors guaranteed-impression deals and brand-aligned creative — onsite display retains 70–90% margins similar to sponsored products.

3. Offsite Media (Programmatic, Social, CTV). This is where the margin profile changes. Offsite retail media uses retailer first-party data to extend audiences across the open web, social platforms, and CTV — but the retailer pays for the offsite inventory, compressing margins to 20–40% per BCG analysis (cross-referenced via Mirakl, 2025 and The Retail Exec, 2025). Despite lower margins, offsite is growing faster than onsite — the offsite retail media advertising monetization category is expected to comprise 18.7% of US retail media ad spend by 2026 (per eMarketer paywalled forecast). Offsite/CTV CPMs run $25–$60 in mid-market RMN benchmarks. The reason retailers run this revenue stream despite lower margins: it absorbs advertiser budget that would otherwise leave the retailer's ecosystem entirely.

4. Data Licensing and Audience Monetization. Selling first-party shopper segments to brand advertisers for use in their own paid media — typically priced as fixed monthly fees of $5,000–$50,000 per audience license, plus revenue share on incremental media activated against the segment (The Retail Exec, 2025). This stream is roughly 10% of mid-market RMN revenue but commands the highest contribution margin. Walmart Luminate and Kroger Precision Marketing's 84.51° data assets are the textbook examples — Kroger centralized these capabilities in 2025 under its Precision Marketing division, consolidating from 84.51° to a unified RMN business unit (Digital Commerce 360, 2025). For deeper coverage of this revenue stream, see our companion article on turning first-party audience data into retail media revenue.

The first-party data strategy retail media monetization angle is the connective tissue across all four streams: same shopper graph, same identity layer, applied differently. The retail media network revenue streams stack — they are not alternatives. A retailer running only sponsored products is leaving 60% of total RMN revenue on the table.

Indicative revenue mix for a mid-market RMN (The Retail Exec, 2025):

| Revenue stream | % of RMN revenue | Pricing mechanic | Indicative margin |

|---|---|---|---|

| Onsite sponsored products | ~40% | CPC $0.50–$3.00 / CPM $10–$40 | 70–90% |

| Onsite display & native | ~10% (subset of onsite) | CPM $5–$25 standard | 70–90% |

| Offsite & CTV | ~35% | CPM $25–$60 | 20–40% |

| In-store digital | ~15% | CPM $10–$50 | 50–70% |

| Data monetization | ~10% | $5K–$50K/month + rev share | 80%+ |

How retailers make money from retail media is no longer a single mechanism — it is this layered portfolio.

CPM vs CPC vs CPA: Choosing the Right Pricing Model

The retail media CPM/CPC/CPA pricing models comparison is the most consequential decision a network operator makes. Each model creates a different incentive between retailer and advertiser, and matching the model to the inventory type (and to the advertiser maturity stage) is what separates yield-optimized RMNs from those leaving 30%+ revenue on the table.

CPM (Cost Per Thousand Impressions). The retailer is paid for delivered impressions regardless of click or sale. CPM works best for brand-awareness campaigns, offsite display, CTV, and high-funnel inventory where impression delivery is the contractually guaranteed unit. CPM benchmarks in retail media run $5–$25 for standard onsite display, $25–$60 for offsite/CTV, and $10–$50 for in-store digital screens (Hello Retail, 2026; The Retail Exec, 2025). The advantage for the retailer: revenue is more predictable than CPC and decoupled from click behavior — the inventory monetizes whether or not the brand's creative converts. Walmart Connect's 38% YoY spend growth in Q1 2025 was driven significantly by CPM-priced upper-funnel inventory (Skai, 2025).

CPC (Cost Per Click). The retailer is paid only when a shopper clicks the ad. This is the dominant model for sponsored products on Amazon, Walmart Connect, Instacart, and most onsite search inventory. Retail media CPC benchmarks span $0.15–$1.50 for sponsored products, climbing higher in competitive categories like beauty, electronics, and consumables (Hello Retail, 2026). CPC is preferred by performance-led advertisers because it aligns spend with engagement, but it transfers volatility risk to the retailer — bad creative produces low click-through rate produces low yield. Notable competitive pressure: Skai data showed Walmart Sponsored Brands CPCs fell 10% YoY in Q1 2025 and Amazon Other RMN CPCs dropped 11% YoY, reflecting auction maturity and competitive entry (Skai, 2025).

CPA / Revenue Share (Cost Per Action). The retailer is paid only when a shopper takes a defined action — typically a sale or sign-up. CPA is rare as a primary onsite RMN model because it puts attribution risk entirely on the retailer, but it appears in offsite revenue share deals and in performance-driven brand partnerships. Revenue share offsite mechanics typically structure as 15–30% of working media spend going to the platform partner (The Retail Exec, 2025).

Hybrid Models — the 2026 Direction of Travel. Retail media hybrid pricing models in 2026 layer a guaranteed CPM floor over performance-priced clicks. A common structure: $3–$8 base CPM plus $0.20–$0.80 per click above an impression threshold (Hello Retail, 2026). The rationale for the retailer: revenue has a predictable floor (from CPM) with upside (from clicks). Hybrid models require six-plus months of audience and inventory data and at least 20 brand partners to execute well — they reward mature RMNs and punish premature adoption. For mid-market retailers building from scratch, the best retail media monetization model is typically pure CPC for sponsored products, pure CPM for display, then a hybrid layer added in year 2 once data and partner depth justify it.

How do retailers charge for comparative advertising on their retail media networks? Comparative product placement — where one brand's ad runs adjacent to a competitor's product detail page — is typically priced at a 1.5x to 3x premium over standard sponsored product CPC, with ceiling caps and exclusivity windows for highest-tier advertisers. Retailers either auction comparative placements with a higher reserve price or sell guaranteed exclusivity windows on a flat-fee basis. Most platforms publish category-level rules to prevent abuse (e.g., no comparative ads in regulated categories like pharmacy).

Auction mechanics and inventory management are how this all gets operationalized. A modern RMN auction must handle reserve pricing per slot, advertiser quality scores, pacing constraints, and competitive blocking — all in milliseconds. Retail media network yield optimization is the practice of dynamically setting reserve prices and slot allocation to maximize total revenue per impression rather than maximizing one auction at a time. For a deeper operational view of the underlying mechanics, see our companion article on auction mechanics and automated bidding in retail media.

Pricing model selection is also where retail media inventory management becomes a monetization lever, not just an ops concern. Inventory that does not clear the auction at one model (e.g., low-fill CPM display) often clears handsomely at another (e.g., the same surface sold as a CPC sponsored placement). The discipline is matching slot economics to advertiser demand patterns.

Revenue Share Structures: How Retailers Split the Pie with Brands

Revenue share is the layer above pricing model — it defines how the gross media spend gets split between the retailer, the platform vendor (if used), and any agency or trading desk in between. The retail media revenue share models for brands fall into three structural categories.

Fixed-Fee Platform Models. The retailer pays a flat monthly or annual fee to a platform vendor for technology, with all ad revenue flowing to the retailer net of the fee. This model is rare because vendors prefer percentage-aligned upside. Where it appears, fees typically range from $250K–$2M annually for mid-tier deployments.

Percentage-of-Ad-Spend Models (Most Common). The platform vendor takes 15–30% of working media spend (The Retail Exec, 2025). For a mid-market retailer running $25M of ad revenue through a platform partner at 20% revenue share, the vendor receives $5M and the retailer keeps $20M gross — before factoring offsite media costs, internal ops, and managed service overhead. Criteo's fee model is a transparent example: CPC or CPM pricing on the media plus a separate SaaS platform fee structured as a percentage of working spend; managed services are optional (Criteo Q3 2025).

Hybrid Co-Op Budget Models. The third structure layers retail media revenue with traditional trade fund and co-op marketing dollars. Brands shift dollars from shopper marketing, brand budgets, and trade spend into the RMN — McKinsey's 2025 analysis confirms RMN spend has not been fully incremental for most CPG advertisers, drawing from these existing pools rather than new growth budgets (per McKinsey commerce media research, 2025). For retailers, this means co-op and trade fund integration is a monetization lever: brands that spend $X in trade can have $0.5X auto-allocated to the RMN if the financial plumbing exists.

Brand Tier Packaging — Basic, Preferred, Premium. Sophisticated RMNs separate advertiser access into tiers. A typical structure:

- Basic (self-serve, low minimum): $5K–$25K monthly minimums, standard auction access, no managed support, no exclusive inventory.

- Preferred: $50K–$250K monthly commitment, priority placement weights, quarterly business reviews, access to first-party audience segments, modest managed support.

- Premium / Enterprise: $500K+ monthly commitments, guaranteed inventory windows, comparative advertising rights, exclusive in-store activation, direct integrations with Luminate / 84.51°-style data tools, dedicated account team.

Tier packaging is what translates pure auction mechanics into a sales motion. It also sets up minimum spend guarantees and annual commitment structures that make revenue forecasting tractable.

The Operational Reality of Co-Op Budget Tracking. Trade fund and co-op budget integration is operationally brutal — different brands run different fiscal calendars, different rebate structures, and different invoicing cycles. The Osmos WalletWise ad fund and trade budget management module is built specifically for this layer: automatic wallet top-up from escrow to prevent campaign pauses, channel-level spend control, rule-based incentive programs, credit lines to attract high-value advertisers without upfront payment, and full transaction records for audit. Retailers running co-op-funded RMNs without this kind of plumbing routinely lose 5–10% of bookable revenue to disputes and pacing failures.

Tier Pricing for Offsite and CTV Inventory

Offsite and CTV is where 2026 retail media monetization gets interesting — and where margin discipline gets hardest. The offsite retail media advertising monetization category is growing roughly 35% per year (per BCG analysis, cross-referenced) versus onsite at ~22%, but margins compress to 20–40% because the retailer pays for the offsite inventory, the data clean room, and the activation infrastructure.

Why Offsite CPMs Command 2–4x Onsite Rates. Offsite/CTV inventory in retail media trades at $25–$60 CPMs versus $5–$25 for standard onsite display (Hello Retail, 2026; The Retail Exec, 2025). The premium reflects three things: (1) first-party shopper data is more valuable than open-web cookies, (2) measured incremental sales are attributable back through the retailer's purchase data, and (3) supply is constrained by data-clean-room friction and brand-safety guardrails.

CTV Inventory Packaging — Retail Media's New Lever. Connected TV is the fastest-growing offsite format. Walmart's $2.3B Vizio acquisition produced triple-digit advertising growth on the integrated Vizio business in Q4 FY26, and Walmart's overall global advertising revenue reached $6.4 billion for FY26 (year ending January 2026), up 37% year-over-year globally — with Walmart Connect US specifically up 41% (AdExchanger, 2026). Retail media CTV and video revenue models typically structure as: (a) guaranteed reach packages priced on CPM with floor commitments, (b) audience-extension overlays where the retailer's first-party segments are activated against publisher CTV inventory, and (c) addressable household targeting where ad delivery is keyed to identified Walmart/Kroger/Target shopper households.

Audience Extension vs Guaranteed Reach. Two distinct offsite pricing structures exist. Audience extension is open-auction programmatic priced on CPM, where the retailer's data is the activation layer — this is most of the volume. Guaranteed reach is a flat-fee or guaranteed-CPM commitment for a defined audience segment with a delivery floor — this is where premium tier advertisers spend. The Amazon DSP retail media monetization motion is the playbook example: per Skai platform data, Amazon DSP captured 20.7% of total Amazon Advertising spend in Q1 2025 — its highest share in five quarters — as advertisers shifted upper-funnel dollars to programmatic (Skai, 2025). About half of Amazon advertisers now run DSP campaigns. Amazon's full-year 2025 advertising services revenue reached $68 billion (up 21.8% YoY), with Q4 2025 alone at $21.32 billion (up 22% YoY); the company's full-funnel strategy added more than $12 billion in incremental advertising revenue in 2025 (Marketing Dive, 2026).

Data Clean Room Requirements. Most offsite monetization above $1M annual scale now runs through a data clean room — a privacy-controlled environment where the retailer's first-party shopper data and the brand's CRM data can be matched without raw data sharing. This is where retail media programmatic advertising monetization meets compliance: clean rooms enable identity matching for attribution and audience activation without violating privacy frameworks. Specialized vendors like MadHive provide clean-room-enabled CTV and programmatic infrastructure, particularly for local CTV monetization layers.

Amazon Onsite vs Offsite — the Closed-Loop Advantage. Amazon's structural advantage in offsite is that purchase data closes the loop natively. Amazon's video advertising monetization across Prime Video's ad-supported tier, Twitch, and partner CTV plus its DSP-powered offsite extension uses purchase signal as the optimization input. This is also why Amazon Ads versus Google Ads for retail media is structurally not a like-for-like comparison: Amazon owns closed-loop purchase data; Google owns intent and search data. Both monetize advertiser demand, but the units of optimization differ.

Real RMN P&L: What the Numbers Look Like

This is where most retail media content stops short. The actual P&L of a retail media network is what determines whether a board approves the investment, and these are the benchmarks operators need.

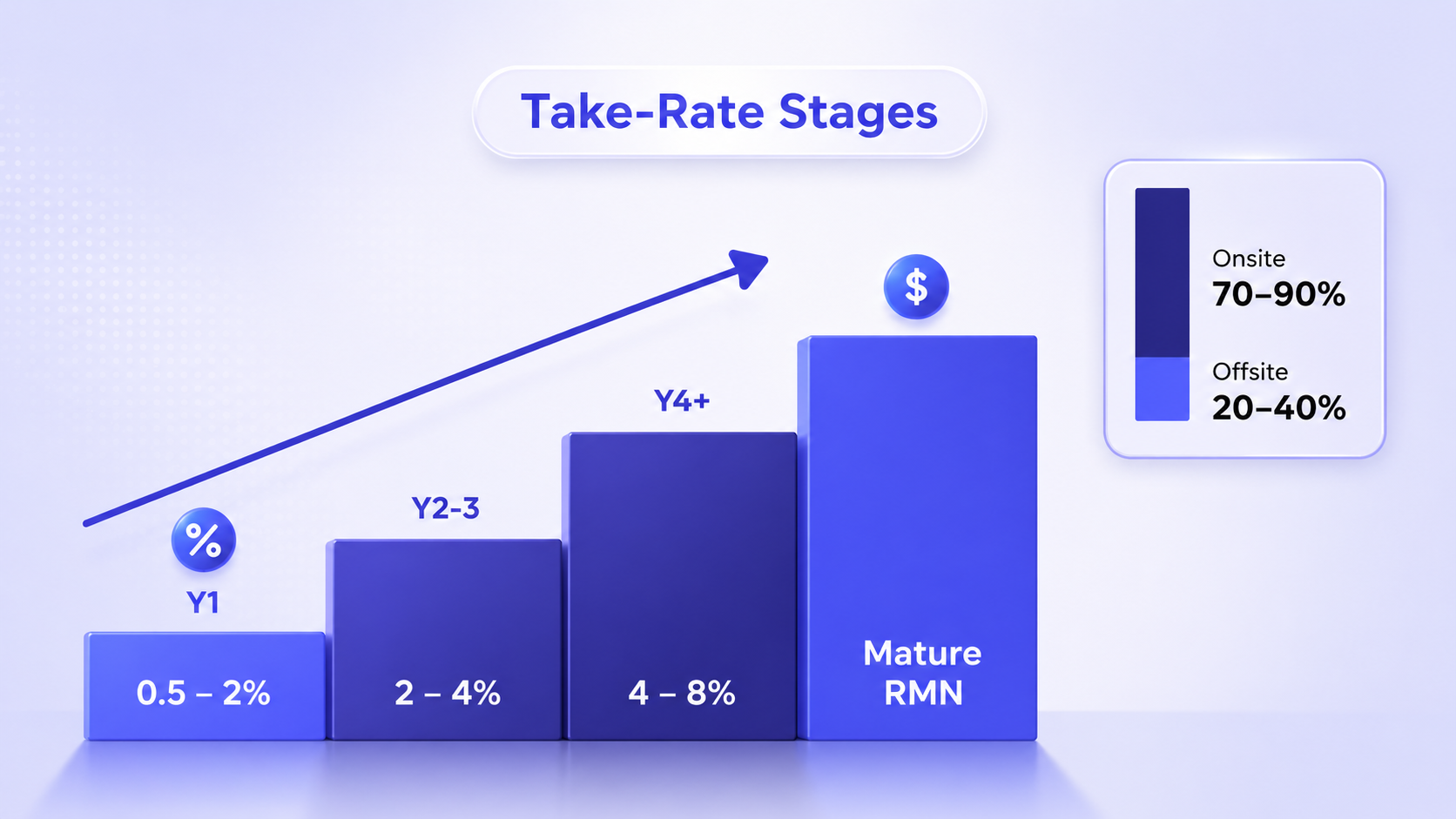

Take Rate Benchmarks by Maturity Stage.

- Year 1 (Launch): 0.5–2% of total company revenue from RMN — essentially pilot-phase economics. Revenue timeline expectations: most mid-market RMNs target $25K–$100K in pilot revenue with 5–10 advertisers each spending $5K–$20K in a 90-day pilot (The Retail Exec, 2025).

- Year 2–3 (Scaling): 2–4% of company revenue. Self-serve adoption rises, advertiser count grows past 50, hybrid pricing models layer in.

- Year 4+ (Mature): 4–8% of company revenue. Walmart's FY26 advertising revenue at $6.4B against ~$650B+ in total revenue puts Walmart in the early-mature stage — and Walmart's CFO John David Rainey signaled significant remaining runway: "We still have long ways to go here to get in the neighborhood of some of the best-in-class competitors. We feel like we can improve our own advertising capabilities while doing it on a growing base, which gives us a lot of runway into the future." — John David Rainey, CFO, Walmart (AdExchanger, 2026). Instacart targets a long-term ads ratio of 4–5% of GTV, currently at ~2.9% (per Instacart Q4 2025 Shareholder Letter) — meaningful headroom remaining.

Contribution Margin Benchmarks by Ad Format.

| Ad format | Indicative gross margin | Reason |

|---|---|---|

| Onsite sponsored products | 80–90% | Owned surface, near-zero inventory cost |

| Onsite display & native | 70–85% | Slightly higher creative ops cost |

| In-store digital screens | 50–70% | Hardware and connectivity costs |

| Offsite programmatic display | 25–40% | Inventory cost paid to publishers |

| Offsite CTV | 20–35% | Premium video inventory cost |

| Data licensing | 80–95% | Pure software/data product |

Margin discipline is critical. Source-cross-referenced from BCG (via Mirakl and The Retail Exec) and confirmed in earnings disclosures, the onsite 70–90% / offsite 20–40% split is the benchmark — a retailer optimizing for ad revenue alone without margin discipline can grow topline while compressing total RMN contribution margin into the 25–35% range. For deeper context on this margin dynamic across the broader retail P&L, see our companion piece on how retail media boosts retailer margins.

EBITDA Impact and the One-Third Rule. Walmart's CFO confirmed that "fully a third of our profit in the most recent quarter was related to advertising and membership income" — John David Rainey, CFO, Walmart (AdExchanger, 2026). For mid-market retailers, the math is comparable in slope if not in scale: adding an RMN that generates 5% of total company revenue at 65% blended contribution margin can increase overall profitability by 25–30% (The Retail Exec, 2025). RMN profit margins of 60–70% versus traditional retail's 5–10% mean every dollar of RMN revenue contributes ~6–10x more to bottom-line profit than a marginal dollar of merchandise revenue.

Disclosed RMN Financials — 2025 Snapshot.

| Retailer / platform | 2025 ad revenue | YoY growth | Source |

|---|---|---|---|

| Amazon Advertising Services | $68.0B (full year) | +21.8% | Marketing Dive, 2026 |

| Walmart Global Advertising | $6.4B (FY26) | +37% global / +41% US | AdExchanger, 2026 |

| Instacart Advertising & Other | $1.065B (FY 2025) | +11% | per Instacart Q4 2025 Shareholder Letter |

| Target Roundel (Q1 2025 disclosed) | $163M Q1 / $649M FY24 | +25% YoY in Q1 | Digiday, 2025 |

| Criteo Retail Media (Q3 2025) | +10% YoY revenue / +11% Contribution ex-TAC | — | Criteo, 2025 |

| DoorDash Ads | $1B+ annualized run-rate (2024) | — | Platform Aeronaut, 2025 |

| Uber Advertising | $1.5B run-rate (Q1 2025) | +60% YoY | Platform Aeronaut, 2025 |

| Criteo Total Annual Media Spend | $4.3B last 12 months | — | Criteo, 2025 |

DoorDash Ads accounts for approximately 15% of gross profit and 36% of EBITDA — a striking demonstration of RMN structural margin advantage. DoorDash also acquired Symbiosys in mid-2025 to extend off-app retail media capabilities (Platform Aeronaut, 2025).

Build vs Buy: Cost and Timeline Realities. This is the decision that determines RMN economics for the next 5+ years.

| Path | Timeline | Investment | Revenue share to vendor |

|---|---|---|---|

| Platform partner build | 3–6 months | $100K–$500K | 15–30% of media |

| Composable / in-house build | 6–12 months | $500K–$1.5M | 0% |

Source: The Retail Exec, 2025. The platform partner path gets to revenue faster but caps long-term margin upside. The composable in-house build preserves margin but extends time-to-revenue and increases execution risk. The middle path — and the one Osmos enables — is white-label deployment of a full retail media OS that the retailer operates under its own brand, with stack co-existence and 4-week deployment, preserving most of the in-house margin profile without the in-house build timeline.

Operational Complexity and Internal Team Structure. Retail media network operational complexity scales with revenue stream count and advertiser tier mix. A typical RMN team structure at the $25M+ revenue stage: a head of retail media, monetization/yield ops (2–3), advertiser sales (3–6 split by tier), advertiser success / managed service (2–4), data and audience ops (2–3), and shared engineering. Mid-market retailers building from scratch consistently underestimate this — and underestimate measurement infrastructure as a category. Strategic considerations for implementing a retail media network: clear executive sponsorship at CFO level, sales motion designed around brand calendars (not retailer fiscal calendars), and a data team that owns the closed-loop feedback into merchandising — not just a media team that owns ad delivery.

For vertical-specific P&L context (grocery, beauty, fashion, QSR, in-store), see our companion deep dive on retail media performance benchmarks by vertical.

Platform Comparison — Amazon vs Walmart Connect vs Criteo vs CitrusAd vs CommerceIQ

The retail media network technology platforms comparison landscape has consolidated into roughly five archetypes: scale-leader RMNs (Amazon, Walmart Connect), retailer-onsite enablers (Criteo, CitrusAd), advertiser-side optimization (CommerceIQ, Skai), CTV/programmatic specialists (MadHive), and full-stack retail media OS (Osmos). The decision is not "which is best" — it is "which fits the role I'm trying to fill in my stack."

Amazon Retail Media (Amazon Ads + Amazon DSP). What is Amazon Retail Media for retailers? It is the gravitational center of the US retail media ecosystem, with approximately 75% US retail media market share (per eMarketer, paywalled) and $68B in 2025 ad revenue. Amazon Ads features for advertisers span sponsored products, sponsored brands, sponsored display, video creative, brand stores, and the full Amazon DSP for offsite extension. Amazon Ads pricing models for retailers (i.e., for Amazon as the operator) are predominantly CPC for sponsored placements and CPM/CPV for DSP and video. The Amazon Ads onsite vs offsite retail media split is migrating offsite — Amazon DSP captured 20.7% of total Amazon Ad spend in Q1 2025, the highest share in five quarters (Skai, 2025). For retailers building their own RMN, Amazon is a benchmark, not a platform competitor — but the ad format playbook (sponsored products as anchor, DSP as offsite extension, brand stores as branded surface) is the most-emulated template in the industry.

Walmart Connect + Walmart Luminate. Walmart Connect retail media network monetization strategy combines onsite sponsored placements, display, and the post-Vizio CTV stack. Walmart Connect ad formats and inventory span Sponsored Products, Sponsored Brands, Display, Onsite Video, Walmart Sponsored Search, and the Vizio-integrated CTV inventory. Walmart Connect pricing models for advertisers are CPC-led for sponsored, CPM for display and CTV. Walmart's first-party data spine, Walmart Luminate, monetizes shopper data through brand subscriptions and audience activations. In the Amazon Ads versus Walmart Connect retail media network comparison, Walmart Connect is the SMB-friendly fast-grower (38% YoY spend in Q1 2025 per Skai) with a closing CPM gap — but at substantially smaller absolute scale. For SMB advertisers, Walmart Connect's lower CPCs (Walmart Sponsored Brands CPCs fell 10% YoY in Q1 2025) and rising self-serve UX have made it the platform of choice for new entrants (Skai, 2025).

Target Roundel. Roundel posted Q1 2025 advertising revenue of $163M, up 25% YoY, and full-year 2024 revenue of $649M (Digiday, 2025). Target Roundel retail media network monetization strategy for retailers leans heavily on offsite extension — significant share of partner media spend happens off Target's owned platforms across social, streaming, and digital publishers — with first-party shopper data as the core differentiator.

Kroger Precision Marketing (KPM). Kroger Precision Marketing retail media monetization strategy underwent structural reorganization in 2025: Kroger centralized retail media under its Precision Marketing division, consolidating capabilities previously managed partly by 84.51° (Digital Commerce 360, 2025). KPM's first-party household data (~60M households via 84.51°) underpins targeted offsite media plus onsite at Kroger Banner sites.

Criteo Retail Media. Criteo retail media network features include onsite sponsored product enablement across 220+ retailer clients globally, Auction-Based Display bringing programmatic to retail media, and Mirakl Ads integration for marketplace monetization. Criteo Retail Media monetization strategy for retailers operates as a third-party platform — retailers license Criteo, brands buy through Criteo's interface, Criteo takes a percentage of working media. Q3 2025 results: +10% YoY Retail Media revenue, +11% Contribution ex-TAC, with $4.3B in total annual media spend driven through the platform across all of Criteo (Marketing Solutions plus Retail Media) (Criteo, 2025). Strong network of 220+ global retailer clients is Criteo's structural advantage.

CitrusAd (Epsilon Retail Media, Publicis). CitrusAd is now Epsilon Retail Media under Publicis — a retailer-onsite enabler with offsite extension via Epsilon's network. CitrusAd features for retailer monetization span sponsored product, display, video, CTV, digital screens, and email creative formats. CitrusAd revenue models for retailers operate similarly to Criteo: license model with revenue share. The Criteo vs CitrusAd retail media network comparison is the central decision for many retailers choosing a third-party onsite enablement layer — Criteo edges on platform maturity and global retailer breadth; CitrusAd edges on the unified onsite + offsite proposition under Publicis. Both serve the same buyer persona but differ on the integration with the wider Publicis network for offsite distribution.

CommerceIQ. CommerceIQ is an advertiser-side platform that helps brands optimize their RMN spending — different buyer persona than retailer-side platforms. CommerceIQ retail media performance is reported via vendor case studies (60% ad sales lift, 40% iROAS improvement claims; not independently verified) on a base of 2000+ CPG brand clients. The CommerceIQ vs Criteo retail media comparison is structural rather than competitive: CommerceIQ optimizes the buy, Criteo runs the platform that serves the buy.

MadHive. MadHive business model for retail media is local CTV and programmatic specialty — it is not a full-stack RMN platform and should not be evaluated as one. MadHive platform features for retail media include DSP capabilities, local CTV inventory, and programmatic targeting infrastructure. MadHive connected TV retail media monetization is its core use case. In the Criteo Retail Media vs MadHive retail media or MadHive vs Criteo retail media question, the right framing is: they serve different layers of the stack. Criteo runs retailer onsite; MadHive provides CTV/local programmatic infrastructure. They can complement each other.

Platform Comparison Matrix — Osmos vs Major RMN Platforms.

| Capability | Osmos (StratEdge / Osmosphere) | Amazon Ads | Walmart Connect | Criteo | CitrusAd / Epsilon | CommerceIQ | MadHive |

|---|---|---|---|---|---|---|---|

| Pricing models supported | CPC, CPM, CPA, Hybrid | CPC, CPM, CPV | CPC, CPM | CPC, CPM | CPC, CPM, Hybrid | Optimizer (not platform) | CPM (CTV-led) |

| Onsite ad formats | Sponsored products, display, native, in-store, gamified, video, story, email | Full | Full | Sponsored + display | Full | N/A | Limited |

| Offsite & CTV support | Native via Adscape | DSP | Vizio CTV + DSP | Limited | Yes (via Epsilon) | N/A | Specialist |

| Self-serve | Yes (Adscape + StratEdge) | Yes | Yes | Yes | Yes | N/A | Limited |

| White-label / retailer-owned | Yes (live in 4 weeks) | No | No | Limited | Limited | No | No |

| Demand generation tooling | Yes (DemandWise) | No | Limited | Limited | Limited | No | No |

| Trade fund / co-op management | Yes (WalletWise) | No | No | No | No | No | No |

| Attribution & measurement | Yes (Pulse Pro) | Closed-loop | Closed-loop | Yes | Yes | Yes | Yes (CTV) |

| Data clean room support | Yes (via integration) | Amazon Marketing Cloud | Yes (Luminate) | Yes | Yes (Epsilon) | Yes | Yes |

| Revenue share model | White-label (retailer keeps revenue) | Amazon-owned | Walmart-owned | % of media spend | % of media spend | SaaS fees | % of media |

Each non-Osmos platform has genuine strengths: Amazon's closed-loop purchase data is unmatched; Walmart Connect's growth velocity and SMB UX are best-in-class for fast-growing brands; Criteo's 220+ retailer network and platform maturity are structural advantages; CitrusAd's unified Publicis-network distribution differentiates; CommerceIQ's iROAS framing serves advertisers well; MadHive's CTV specialism is operationally sound. The Osmos differentiation is full-stack OS coverage from onsite to offsite under retailer ownership — no third-party DSP dependency, no revenue share to a platform vendor, demand generation and trade fund management built natively.

For retail media platforms reviews comparisons in 2026, the practical evaluation framework is: (1) what role does this platform fill in my stack, (2) what is the long-term revenue share cost, (3) does it preserve or compromise data sovereignty, and (4) what is the migration path if I outgrow it.

Advertiser Demand Generation and Forecasting

Building inventory is solved. Filling inventory is not. Advertiser demand generation in retail media networks is the single most underestimated discipline in the operator playbook — and the gap between RMNs running at 30% fill rate and those running at 85% is rarely a tech gap. It is a demand engineering gap.

The Audience Threshold Problem. 99% of CPG brands require access to at least 6 million shoppers before committing to a new RMN (The Retail Exec, 2025). For sub-scale retailers, this is a chicken-and-egg constraint: brands won't commit without scale, scale doesn't materialize without brand commitment. Solutions: marketplace consortium models, network interoperability, and audience pooling where multiple mid-market RMNs combine first-party segments.

Building the Advertiser Pipeline. For a new or scaling RMN, advertiser pipeline construction is a structured sales motion:

- Tier 1 (Endemic CPG brands): Existing trade and shopper marketing relationships convert first. Goal: 5–10 anchor advertisers in the 90-day pilot at $5K–$20K each (The Retail Exec, 2025).

- Tier 2 (Mid-market endemic): SMB-aligned advertisers attracted by self-serve UX and lower minimums. This is where Walmart Connect's 38% spend growth in Q1 2025 came from — SMB scaling.

- Tier 3 (Non-endemic / adjacent): Brands without direct shelf relationships (telco, finance, auto) buying audience access. This is the 12–24-month tier that unlocks the offsite revenue stream.

Strategies for attracting advertisers to retail media at the operational level: dedicated advertiser onboarding workflows (technical setup measured in days, not weeks), behavior-based segmentation of advertisers for tailored outreach, multi-channel drip campaigns across email/push/WhatsApp/SMS, and content curation by advertiser cohort. The Osmos DemandWise advertiser demand generation module is built for this layer — custom advertiser segmentation with tailored multi-channel drip campaigns, delivering 36% improvement in advertiser retention.

Demand Forecasting Models. Advertiser demand forecasting for retail media networks is the discipline of predicting bookable revenue per inventory slot per time window. Inputs typically include: historical bookings by advertiser tier, brand calendar events (back-to-school, holidays, new product launches), seasonal category demand, fill rate trends, and self-serve advertiser counts. The benefits of accurate advertiser demand forecasting retail media include: avoiding pricing floor erosion in low-demand windows, scheduling premium inventory releases against peak demand, and directing managed sales effort where pipeline gaps will appear. Challenges in advertiser demand forecasting retail media — limited historical data for new RMNs, the long ramp-up of self-serve advertiser cohorts, and category seasonality that does not match the retailer's fiscal calendar — make first-year forecasting particularly difficult.

Pricing Floor Strategy. Retail media self-service platform monetization rises and falls on pricing floor discipline. Without floors, self-serve advertisers race CPCs to the bottom; with floors set too high, fill rates collapse. The 2026 best practice is dynamic floors per slot type, adjusted weekly based on fill rate and demand signal — fill rates below 30% indicate insufficient advertiser demand and floor compression is warranted; fill rates above 80% warrant price increases (Hello Retail, 2026).

Self-Serve Adoption as a Monetization Multiplier. Self-serve adoption is the single biggest leverage point on RMN economics. It scales the long tail of advertiser count without scaling managed-service headcount. Walmart Connect, Amazon Sponsored Products, and Criteo all run heavily on self-serve, and Skai's 2025 data shows 68% of advertisers expect their retail media budgets to increase — disproportionately through self-serve channels (Skai, 2025).

Retail Media Network Onboarding Advertisers Best Practices. A modern advertiser onboarding flow includes: KYC and contracting in days not weeks, automated wallet funding via WalletWise-style escrow auto-debit, creative QA in workflow rather than ticket-based, segment access tied to tier, and a 30-day check-in cadence that catches stalled advertisers before they churn.

Attribution and Measurement: Proving Revenue to Advertisers

Measurement is where retail media monetization either justifies premium pricing or collapses to commodity CPM. The retail media network attribution and ROI measurement gap is the single largest bottleneck on RMN spending growth — and the largest opportunity for premium pricing as it closes.

The State of the Measurement Market. Only 15% of marketers report being very or extremely effective at measuring retail media performance (Skai, 2026). 75% identify incrementality as their biggest retail media measurement challenge; cross-channel attribution is cited by 59%. 50% of brands measure incrementality at only a basic level; just 20% are proficient at both measuring and applying insights. Marketers report that reducing wasted spend was achieved by 54% versus a 58% target, and new customer acquisition was achieved by 49% versus 58% hoped — measurement aspirations consistently outrun measurement actuals.

"Incrementality is now the price of performance. If you cannot measure incrementality with discipline, you are not running performance media." — Enrico Babucci, CSO, OmniShopper (Skai, 2026)

The IAB Measurement Framework. The IAB defines incrementality as the causal impact of marketing — the additional business outcomes directly driven by a campaign or tactic, compared to what would have occurred in the absence of marketing activity (IAB, 2025). The IAB November 2025 commerce media measurement guidelines codify advanced techniques including Random Controlled Trials (RCTs), Match-Market Testing, Counterfactual Models, and Media Mix Modeling (MMM). Albert Heijn became the first retail media network to achieve certification under IAB Europe's measurement programme in September 2025 (per IAB Europe announcement). Retail media network performance metrics now standardizing include onsite ROAS, blended cross-channel ROAS, incremental ROAS (iROAS), new-to-brand customer share, and category share of voice.

Multi-Touch Attribution Retail Media — and Its Challenges. Multi-touch attribution retail media remains hard because (1) onsite click-to-purchase is one of the few clean closed-loop signals while offsite signal degrades through clean rooms and identity loss, (2) cross-platform exposure attribution requires identity resolution across retailer, brand, and publisher data, and (3) advertiser-side and retailer-side attribution models routinely disagree by 20–40% on credit. Solutions for retail media attribution challenges: standardized incremental sales lift testing, consistent identity spine across onsite and offsite, third-party measurement validation, and shifting buyer expectations toward incrementality as the gold standard rather than last-click ROAS.

Cross-Channel Attribution Retail Media Network Performance. The cross-channel attribution retail media network performance measurement layer has converged around three approaches: deterministic match where retailer purchase data is tied to ad exposure via clean room, probabilistic match for unmatched audiences using device graphs and modeled identity, and incrementality testing with control/exposed split as the truth layer above both. For platform-specific implementation across the major RMNs, see our deep dive on closed-loop attribution mechanics at Walmart, Amazon, and Instacart.

Walmart Connect Attribution Model. Walmart Connect uses a closed-loop attribution model linking ad exposure to in-store and online Walmart purchases through Walmart's first-party shopper data. This is structurally similar to Amazon's closed-loop model and to Instacart's GTV-tied attribution.

Amazon Ads Revenue Attribution Retail Media. Amazon Ads revenue attribution operates on closed-loop purchase data within the Amazon ecosystem — sponsored product ads attribute against Amazon purchases natively, DSP campaigns extend into off-Amazon publisher inventory but use Amazon Marketing Cloud (AMC) clean room infrastructure for attribution back to Amazon purchase signal.

Retail Media Performance Standards and Performance by Category. Retail media performance varies meaningfully by category and vertical — beauty, food, and apparel show different ROAS, click-through rate, and incremental lift profiles. Skai's Q1 2025 quarterly data is the cleanest publicly available cross-vertical performance benchmark (Skai, 2025). Retail media incrementality benchmarks have a wide range — vendor-reported iROAS spans from 253% to 1,609% across advertisers per Skai 2026 measurement research, illustrating how dramatically true incremental value can vary. For platform-by-platform performance and ROAS benchmarking by ad format, see our hub guide: ROAS benchmarks by platform and ad format.

Pulse Pro for Operational Measurement. The Osmos Pulse Pro retail media performance monitoring module provides centralized intelligence across the retail media program: live advertiser insights with red-flag alerts on Pareto advertisers' campaign performance, projected impressions per inventory slot with unbooked revenue potential, and yield optimization analysis — delivering 39% increase in yield as the headline platform stat. For attribution into advertiser-facing reporting, Pulse Pro feeds the data layer that closes the loop between media exposure and revenue impact.

How Osmos StratEdge Powers RMN Monetization

The retail media operating system that runs all of the mechanics in this guide — pricing model architecture, revenue share management, tier packaging, advertiser demand engineering, attribution — is the StratEdge retail media strategy platform, part of the broader Osmos Osmosphere full-stack OS (Adscape + ControlHub + StratEdge).

StratEdge — the strategic powerhouse. StratEdge delivers verified platform results: 38% increase in fill rate, 3x increase in monetization, and 40% improvement in brand adoption (Osmos StratEdge product page). The component breakdown maps directly to the monetization disciplines covered above:

- Pulse Pro — knowledge hub with live advertiser and campaign insights, growth opportunity identifier, monetization program health trends, and advertiser segment deep-dives. 39% increase in yield.

- Demand Wise — advertiser acquisition and retention via behaviour-based advertiser segmentation, multi-channel drip campaigns, and content curation by advertiser cohort. 36% improvement in advertiser retention.

- Ad Bundles — omnichannel ad packages combining online and in-store inventory, event and festival campaign planners, and package-level performance reporting for big-ticket advertiser deals.

- BYOT (Bring Your Own Traffic) — lower-funnel reporting of advertiser-driven traffic, A/B testing for traffic source quality, cookie-less traffic tracking, and ad-blocker-secure audience mapping.

- King Of The Hill (House Ads) — self-serve house ads management, contextual audience targeting, auction-enabled publishing, and full-funnel reporting.

Osmosphere — the full-stack retail media OS. The Osmosphere suite combines Adscape (high-yield ad serving with premium ad formats, off-platform exposure, advanced targeting, self-serve campaign management), ControlHub (operations scale, financial process automation, advertiser and agency onboarding, content review workflows, end-to-end order management), and StratEdge (revenue strategy and yield optimization). White-label deployment, co-existence with the retailer's current stack, and a turnkey 4-week deployment timeline make this the path for retailers who want full ownership without composable build pain.

WalletWise addresses the trade fund and co-op budget management layer described in the revenue share section — automatic wallet top-up via escrow auto-debit, channel-level spend control, rule-based incentive programs, and credit lines for high-value advertisers.

The retail media network technology stack requirements that this addresses span: ad serving (Adscape), operations and onboarding (ControlHub), strategy and yield (StratEdge), advertiser demand (Demand Wise), measurement (Pulse Pro), trade fund (WalletWise), and house ads (King Of The Hill). The retail media network vendor selection criteria — full-stack coverage, white-label deployment, demand generation built-in, no third-party DSP dependency, IAB Tech Lab OM SDK certified — are how Osmos differentiates from CitrusAd, Criteo, and other partial-stack platforms.

For data governance and IAB compliance: Osmos integrates with retailer-owned data clean rooms and supports the privacy frameworks (GDPR, CCPA, sector-specific) that retail media network compliance requires.

Retail Media Pricing Questions: Benchmarks, Take Rates and Inventory-Specific Models

The pricing questions retailers actually get asked fall into four groups: what the CPM benchmarks are and how far they can be trusted, what a platform should charge to serve inventory, what take rate applies on offsite and CTV, and how to price surfaces that have no established rate card at all. The rate ranges themselves are in the CPM, CPC and P&L sections earlier in this guide. This section answers the questions around them, which is where most pricing decisions actually go wrong.

What were 2025 retail media CPM benchmarks and what changed going into 2026?

The 2025 benchmark set is still the reference most advertisers quote, and the ranges published in this guide hold as the working baseline. Three things have shifted since, and they matter more than the headline numbers. Onsite inventory has tightened as more retailers opened self-serve, so the spread between premium and standard placement widened rather than the average moving. Offsite and CTV pricing has stayed structurally higher than onsite because the inventory is bought against audience rather than intent. And the benchmark itself has become less transferable: as networks diverge in ad load, auction design and attribution windows, a CPM from one network is a weaker predictor of another's than it was two years ago. Treat any published benchmark as a sanity check on your own rate card, not as a target.

How do Amazon Sponsored Display and Amazon DSP CPMs compare?

The two are priced differently because they buy different things, and comparing their CPMs directly is a category error that shows up constantly in benchmark decks. Sponsored Display is bought inside the retail environment against shopping context, so its pricing reflects proximity to the transaction and it competes with other onsite placements. DSP inventory is bought programmatically across a much wider surface, including off-property and connected TV, so its CPM reflects audience reach and the inventory's own supply dynamics. A higher DSP CPM does not mean DSP is worse value, and a lower one does not make it better: the comparison only means something once both are measured on the same attribution window and the same incrementality standard. For a retailer setting its own rate card, the useful lesson is that the pricing logic should follow the buying context rather than a single network-wide number.

What should a retail media network charge per million impressions through an API?

Programmatic access to a network's inventory is usually priced one of three ways, and the choice signals what the network thinks it is: a straight CPM on delivered impressions, which treats the API as another buying route; a platform or access fee on top of media, which treats it as a product; or a revenue share, which ties the network's income to the advertiser's outcome. The number matters less than two structural questions. Does the API price differ from the managed-service price for identical inventory, because if it does, the network is charging for the interface rather than the inventory and sophisticated buyers will notice. And is the rate quoted on delivered or requested impressions, since the gap between the two is where disputes start. Publish the answer to both before anyone asks.

What take rate and platform fees should a retailer expect on offsite and CTV?

Offsite and CTV carry more intermediaries than onsite, and each one takes margin. A typical chain includes the demand platform, the supply platform, and any data or identity fee applied to activate the retailer's audiences. The retailer's net therefore sits well below the gross CPM the advertiser pays, which is why offsite margins run materially thinner than onsite, as the margin discussion earlier in this guide sets out. The questions worth asking any offsite partner are what the total fee load is between advertiser payment and retailer receipt, whether that load is disclosed or netted silently, and who owns the audience once it has been activated externally. A retailer that cannot answer the first question cannot forecast offsite contribution accurately.

How do you price in-store digital media inventory: CPM, flat fee, or performance-based?

In-store is the surface with the least established pricing convention, and all three models are in live use. Flat-fee placement, priced by screen and duration, is the simplest to start with and the easiest for a supplier funding it from trade budget to approve. CPM pricing requires a defensible impression definition, meaning an agreed method for counting who was actually in front of the screen, and it is only credible once measurement exists. The IAB's framework for maturing in-store media measurement sets out the progression from scheduled plays to verified impressions. Performance-based pricing, tied to store-level sales lift, commands the best rates but requires a holdout methodology the supplier accepts. Most retailers should start on flat fee, invest in impression measurement, and move to CPM once the count is defensible. Pricing in-store on CPM before the measurement exists invites the dispute that ends the pilot.

How can a retail media network use attention measurement to justify higher CPMs?

Attention metrics matter commercially because they let a network argue value on something other than price. The argument only lands when three conditions hold. The measurement has to come from a method the advertiser recognises rather than a proprietary score the network defined for itself, which is what the IAB advanced measurement guidance is intended to standardise. It has to be reported alongside outcome data, because attention that does not correlate with sales lift reads as a vanity metric. And it has to distinguish between placements, since a network-wide attention average gives a buyer no reason to pay more for the premium slot specifically. Used well, attention data reprices the top of the inventory ladder rather than lifting the whole rate card.

Which retail media platform is best for monetizing a grocery ecommerce site?

For a grocery retailer the choice is between marketplace-native infrastructure, an identity-led enterprise suite, an API-first auction layer, and an independent multi-channel platform run under the retailer's own brand. The full comparison, including what each option gives a grocery retailer and the public evidence behind it, is set out in the grocery platform landscape in our retail media by vertical guide. The pricing angle specific to this guide is that the four options recover their cost differently: revenue share scales with the network and becomes the most expensive at maturity, licence models front-load cost, and API pricing is the most predictable but leaves integration work with the retailer. Model the effective rate at three times current volume before choosing, because grocery networks that succeed outgrow their first pricing assumption quickly. Osmos runs onsite, offsite and in-store retail media on one wallet and one yield engine, so the rate card stays consistent as channels are added rather than fragmenting per vendor.

How do publishers increase CPM on CTV without hurting fill rate?

The floor price is the lever, and it cuts in both directions: raising it lifts the price of every impression that still clears it and zeroes the value of every impression that no longer does. The mistake is judging the change on CPM, which almost always looks better after a floor rise, instead of on net revenue per available impression, which frequently looks worse. Measure both together or the decision is being made on the flattering half of the data.

Three practices separate a floor that earns from a floor that starves the pod. First, price the floor by position rather than by property: a first-position slot in a break and a late-position slot in the same break do not deserve the same reserve, and a single property-wide floor forces the weakest inventory to carry the strongest inventory's price. Second, change floors on split traffic and hold them long enough to read fill, win rate, and total revenue together, because a floor that lifts CPM in week one can surface as unfilled inventory in week three. Third, commit the demand that will commit: reserve the volume a buyer will guarantee, and leave the remainder in the auction rather than setting a reserve high enough to protect guaranteed pricing across inventory nobody has bought.

Timing matters more in 2026 than it did, because CTV is both the fastest-growing line in retail media, growing about three times faster than retail media search on eMarketer's read, and increasingly bought in the auction rather than committed up front. IAB's 2025 video research found that buyers expect 47% of CTV inventory to be biddable, up from 34% the year before, and that 74% have built or are building internal teams to run self-serve CTV activation. A retailer holding floors designed for a mostly-guaranteed market is pricing against demand that has already moved, and facing buyers with the in-house capability to notice.

Two things make the read trustworthy. Unfilled and undelivered impressions have to be counted on the same basis as delivered ones, which is what the IAB and MRC measurement guidelines exist to standardize, and the floor decision has to be visible against onsite yield rather than in an offsite silo. Running onsite and offsite inventory on one stack, as Osmos does, is what makes that comparison possible at all. The auction mechanics guide covers how floors, bid density, and pacing interact once the inventory is live.

Frequently Asked Questions

How does Amazon Ads compare to Google Ads for retail media?

Amazon Ads and Google Ads are structurally different products even though both monetize advertiser demand. Amazon Ads is a retail media platform — it monetizes purchase intent and closed-loop conversion data tied to Amazon's marketplace inventory. Amazon's full-funnel ad business reached $68B in 2025 with closed-loop attribution to Amazon purchases (Marketing Dive, 2026). Google Ads is a search and intent platform — it monetizes search and contextual intent across Google's properties and the open web, with attribution to advertiser-defined conversion events. For retail media specifically, Amazon's structural advantage is the closed-loop purchase signal as the optimization input; Google's advantage is upper-funnel intent data and reach. They are complementary in most CPG advertiser stacks, not substitutes.

How does Amazon Brand Store monetization work?

Amazon Brand Stores are retailer-owned brand experiences within Amazon — multi-page custom storefronts that brands build to consolidate their Amazon presence. They are not directly priced as a paid placement; instead, brands invest in store creation and use sponsored brands and sponsored display ads to drive traffic to the store. Brand Store monetization for Amazon is indirect — better stores produce better organic conversion which pulls more sponsored ad spend through the funnel. For retailers building their own RMN, the analog is curated brand pages within the retailer's own e-commerce environment — premium tier advertisers typically gain access to enhanced brand-page real estate as part of their tier package.

What is Walmart Luminate and how does it support data monetization?

Walmart Luminate is Walmart's first-party data subscription product — a SaaS platform that gives brands access to Walmart's shopper transaction and behavior data through a clean-room interface. Brands subscribe for analytics, audience-building, and measurement across Walmart's omnichannel shopper base. Luminate is Walmart's data monetization revenue stream layered on top of Walmart Connect ad spend — analytically separable but commercially tied. The Walmart Luminate data monetization strategy is the playbook example of how a retailer turns first-party shopper data into a SaaS-priced revenue line independent of media spend.

What team structure does a retail media network require?

Mid-market RMN team structure at the $25M+ revenue stage: a head of retail media, monetization/yield ops (2–3 people), advertiser sales split by tier (3–6 people across SMB, mid-market, enterprise), advertiser success / managed service (2–4), data and audience operations (2–3), shared engineering and product, plus a measurement/analytics function. Below $10M ARR, this collapses into a 4–6 person team with founder-led sales and external platform engineering. Above $100M ARR, sub-functions specialize further (yield engineering, programmatic ops, retail media research). Retailers consistently underestimate the data team size — the closed-loop feedback into merchandising is a data engineering investment, not a media team responsibility.

What data governance and privacy requirements apply to RMNs?

Retail media network data governance requirements span GDPR, CCPA, sector-specific regulations (HIPAA-adjacent for pharmacy, COPPA for child-targeted categories), and the IAB Tech Lab privacy frameworks. Practical requirements: explicit shopper consent for data activation, clean-room infrastructure for offsite identity matching without raw data sharing, consent-state passing across the ad stack, retention limits, and audit-trail capture for regulator response. Most RMNs running above $5M annual ad revenue maintain a dedicated privacy/compliance role. Retail media network compliance and privacy is increasingly the gating constraint on offsite expansion — clean room investment and consent infrastructure are not optional.

How does CitrusAd compare to PubMatic for retail media monetization?

CitrusAd (Epsilon Retail Media under Publicis) and PubMatic operate at different layers. CitrusAd is a retailer-onsite enabler with offsite extension via Epsilon's network — the buyer is the retailer licensing the platform to monetize first-party inventory. PubMatic is a sell-side programmatic platform that increasingly serves retail media supply paths, but its retail media specific platform is targeted at retailer-side monetization with a programmatic-native architecture. The choice depends on the retailer's emphasis: CitrusAd is stronger for unified onsite + offsite under a single managed-service model with Publicis network access; PubMatic is stronger for retailers who want a programmatic-native sell-side stack with more open-web SSP integration. There is no published 2026 head-to-head head-to-head benchmark to definitively call one a better choice — evaluation should be platform fit to existing tech stack and retailer data sovereignty requirements.

How does Criteo Retail Media compare to MadHive?

Criteo Retail Media and MadHive are not direct competitors — they serve different layers of the retail media stack. Criteo is a retailer-onsite enablement platform with 220+ retailer clients globally, focused on sponsored product, display, and Auction-Based Display programmatic for retailer-owned inventory (Criteo, 2025). MadHive is a CTV and local programmatic specialist — its retail media play is primarily CTV inventory monetization with data clean-room support, not a full RMN platform. A retailer might run Criteo as its onsite enablement layer and use MadHive as a CTV/local extension layer simultaneously. In a head-to-head decision: choose Criteo for retailer onsite RMN enablement, choose MadHive when CTV/local is a primary inventory category.

How does Criteo Retail Media compare to PubMatic?

Criteo Retail Media and PubMatic's retail media offerings serve different sides of the supply path. Criteo operates as a managed retailer onsite platform with deep retailer integration and programmatic display via its Auction-Based Display product (Criteo, 2025). PubMatic's retail media platform is a programmatic-native sell-side architecture targeting retailer monetization through SSP infrastructure. Criteo edges on retailer breadth (220+ clients) and integrated managed services; PubMatic's structural difference is its independent SSP positioning. There is no authoritative 2025–2026 head-to-head benchmark publicly available. The right framing for retailers: Criteo for managed retail-media-as-a-service, PubMatic for programmatic-native sell-side architecture with greater openness.

What are CommerceIQ's retail media benchmarks?

CommerceIQ publishes vendor-reported case study benchmarks including ~60% ad sales lift and ~40% iROAS improvement claims drawn from its 2000+ CPG brand client base. These benchmarks are vendor-reported — not independently verified — and should be treated as directional evidence of platform impact rather than industry benchmarks. CommerceIQ does not publicly disclose financial revenue benchmarks. For independently verified retail media performance benchmarks, Skai's quarterly platform reports (covering $9.2B+ in managed media) are the cleanest cross-platform reference.

How does CommerceIQ compare to Criteo for retail media?

CommerceIQ and Criteo serve different buyer personas. CommerceIQ is an advertiser-side optimization and intelligence platform — brands use it to manage and optimize their RMN spend across Amazon, Walmart, and other RMNs. Criteo is a retailer-side platform — retailers license Criteo to monetize their own onsite inventory. They are not substitutes; they are layers in the same end-to-end media flow. Brand advertisers can run CommerceIQ on top of media bought through Criteo-powered retailer platforms. Where CommerceIQ vs Salesforce comes up — Salesforce Marketing Cloud has retail media features within its broader marketing platform, but operates as a CRM/marketing automation suite rather than a dedicated retail media optimization platform like CommerceIQ.

What role do data clean rooms play in retail media monetization?

Data clean rooms are privacy-controlled environments where two parties (retailer and brand, or retailer and publisher) match data without exposing raw customer records. In retail media, clean rooms enable: (1) identity matching for offsite audience extension, (2) closed-loop attribution measurement across owned and offsite media, (3) audience segment validation and overlap analysis, and (4) compliance with privacy frameworks (GDPR, CCPA). Major retailer clean rooms include Amazon Marketing Cloud (AMC), Walmart Data Ventures clean room infrastructure, and Kroger 84.51° clean room. Specialist providers like MadHive offer clean-room-enabled CTV programmatic environments. The MadHive data clean room retail media use case is primarily for CTV publisher and brand match operations.

How can publishers and marketplaces increase yield by launching commerce media monetization?

Publishers and marketplaces increase yield by turning their owned surfaces and first-party data into a commerce media network — selling sponsored product placements, display, and offsite audience extension against traffic they already have. The highest-yield stream is onsite sponsored products, which carry 70–90% margins because the inventory cost is effectively zero (the platform already owns the surface). Standing up this monetization layer typically lifts revenue several-fold; Osmos StratEdge reports a 3x increase in monetization and a 38% fill-rate uplift. For the broader shift of retailers and marketplaces becoming media networks, see our guide on retailers becoming media networks.

What are 2026 retail media CPM benchmarks?

CPM benchmarks vary widely by placement and platform — onsite sponsored and display inventory commands premium rates versus offsite extension, and pricing differs across Amazon, Walmart Connect, Instacart, and independent RMNs. Rather than chase a single number, monetization teams should benchmark CPMs against comparable placements alongside ROAS. For current CPM and ROAS ranges by platform and ad format, see our ROAS Benchmarks by Platform and Ad Format guide.

Is a retail media network profitable, and what margins should retailers expect?

Yes — retail media is among the highest-margin revenue a retailer can run. Onsite sponsored products and display generate 70–90% margins because the inventory cost is essentially zero (the retailer already owns the surface), while offsite audience extension runs 20–40% because the retailer pays for third-party inventory. A network's blended profitability therefore depends on its onsite-versus-offsite mix: the more revenue concentrated in onsite sponsored products — typically around 40% of a mid-market RMN's revenue — the stronger the contribution margin.

What is the best commerce media platform with managed services?

The right platform depends on whether you need a self-serve ad server or a managed monetization layer. For retailers and marketplaces that want commerce media monetization run for them — pricing-model architecture, revenue-share management, and advertiser demand generation — Osmos StratEdge operates the full revenue stack, with verified results including a 40% improvement in brand adoption. For a side-by-side of platforms to build or run a retail media network, see our guide on the best retail media platform for retailers and marketplaces.

Conclusion: Build the Revenue Architecture First

The retail media networks that will lead in 2026 are not those with the most ad inventory. They are the ones with the most disciplined revenue model architecture: pricing models matched to inventory type, tier packaging that scales advertiser revenue, revenue share structures that preserve margin, demand engineering that fills the inventory before yield optimization fights for scraps, and measurement that justifies premium pricing.

The 2026 monetization stack is layered. Onsite sponsored products at 80–90% margins anchor the P&L. Onsite display compounds that base. Offsite and CTV trade lower margins for inventory absorption and advertiser stickiness. Data licensing tops the contribution mix at 80%+. Done together, this delivers the 60–70% blended margins that turn retail media from an experiment into a structural earnings stream — the way it already has at Walmart, where one-third of Q4 FY26 operating income now comes from advertising and membership.

To model your own RMN economics — current revenue, projected uplift by match type expansion, and fill rate optimization — use the Osmos Retail Media Revenue Calculator. For the underlying platform that powers the monetization stack described in this guide, the StratEdge retail media strategy platform covers ad serving, demand generation, trade fund management, yield optimization, and measurement under one retailer-owned, white-label deployment.

The math has changed. The architecture is what matters now.

Sources

- Walmart's Ad Revenue Totaled $6.4 Billion In 2025 As The Ecommerce Flywheel Started To Spin — AdExchanger, February 19, 2026.

- Amazon's annual ad revenue passes $68B, boosted by full-funnel strategy — Marketing Dive, February 6, 2026.

- Retail Media Trends: Key Insights and Strategies from Q1 2025 — Skai, April 17, 2025.

- The 2026 State of Retail Media Measurement and Incrementality — Skai, February 4, 2026.

- How Mid-Market Retailers Can Build Retail Media Networks: Beyond Amazon & Walmart — The Retail Exec, November 12, 2025.

- Retail Media Revenue Models Compared: CPC, CPM, and Hybrid — Hello Retail, February 21, 2026.

- Criteo Reports Strong Third Quarter 2025 Results — Criteo, October 28, 2025.

- IAB Guidelines for Incremental Measurement in Commerce Media — IAB, November 3, 2025.

- How Do Retail Media Networks Make Money? Revenue Streams and Profitability — Mirakl, September 19, 2025.

- Target's Roundel ad revenue climbs as retail sales decline — Digiday, June 2, 2025.

- Instacart Announces Fourth Quarter and Full Year 2025 Financial Results — Maplebear Inc. (Instacart), February 12, 2026.

- Monetizing Meals: Advertising Ecosystems at Instacart, Uber Eats, and DoorDash — Platform Aeronaut, June 16, 2025.

- IAB Adjusts 2025 Outlook Amid Ad Buyers' Macroeconomic Concerns: Social, Retail Media, CTV Will Still See Double-Digit Growth — IAB, September 25, 2025.

- Retail Media Ad Spending Forecast and Trends H2 2025 — eMarketer, November 5, 2025 (paywalled — preview stats only).

- Kroger Centralizes Retail Media and More Under Precision Marketing Division — Digital Commerce 360, August 1, 2025.

.png)