Subscribe to our news letter

Last updated: May 2026.

Reviewed by Najfee Hyder, Product Marketing Specialist.

Native ads outperform standard display on every operator-relevant metric in 2026 retail media — eMarketer reports an 18% lift in purchase intent versus standard display and 53% higher view frequency than banners, TripleLift's June 2025 survey shows 74% marketer satisfaction with native (zero dissatisfaction — the highest of any retail media format), and verified platform-level ROAS ranges sit between 2x and 8x+ depending on placement, vertical, and attribution model. For the broader cross-format picture, see our ROAS Benchmarks by Platform and Ad Format (2026) hub; for sponsored-search and sponsored-display taxonomy (a separate ad family that operators frequently conflate with native), see the Operator's 5-Type Playbook for sponsored ad formats. This guide is specifically for retail and marketplace operators building native ad inventory: what to expect from CTR, conversion, and ROAS benchmarks; how the six leading native platforms compare; how to allocate budget and attribute performance at overview depth; and how Osmos enables operators to own the native ad stack instead of renting demand.

Native Ads vs Sponsored Ads: Why the Distinction Matters for Operators

Native advertising is a paid ad format engineered to match the visual design, contextual placement, and editorial behaviour of the surface it appears on — in retail media, that means in-feed product cards, shoppable content units, recipe and recommendation modules, and contextual display tiles that read as part of the shopping experience rather than an interruption to it. Sponsored ads, by contrast, are auction-bought paid placements (sponsored search, sponsored brands, sponsored display) that are clearly labelled and slotted into reserved positions on search results, product detail pages, and category pages.

Operators frequently conflate the two because both are commerce-adjacent and both monetise first-party shopper context. The distinction matters because it changes three operational decisions:

- Inventory architecture — Native units are dynamically configured to surface in mixed editorial/commerce flows. Sponsored units sit in fixed slots that the operator has formally reserved for monetisation. Different inventory schemas, different bid logic.

- Attribution — Native is engagement-heavy (impressions, scrolls, view-through, assisted conversion). Sponsored is click-heavy and converts in-session. Applying sponsored-style last-click attribution to native systematically under-credits it.

- Format taxonomy — Sponsored search, sponsored brands, sponsored display, and in-store sponsored placements have well-established format specifications and creative templates. Native formats (product native, content native, shoppable display, story ads, in-store digital signage) are still standardising — and brand-compliant creative is consistently flagged as a top operator pain point.

For the full 5-format sponsored ad taxonomy (sponsored search, sponsored brands, sponsored display, sponsored video, in-store sponsored), refer to the Operator's 5-Type Playbook for sponsored ad formats. The remainder of this guide focuses exclusively on native: benchmarks, platforms, attribution, budget, and ROI.

Native Ad Performance Benchmarks in Retail Media (2026)

Three benchmark families matter to operators: engagement (CTR, time spent), conversion (CVR, new-to-brand rate), and revenue (ROAS, incremental ROI). Verified 2025–2026 data sits in the following ranges.

CTR benchmarks

- eMarketer's 2026 native ad performance threshold: CTR above 0.4% indicates strong native performance (eMarketer, 2026). Operators should treat 0.4% as a floor for "performing" native units across onsite and offsite contexts.

- Schnucks Carrot Ads (in-store digital native): 2.6% CTR for shoppable display surfacing in-store environments (RMIQ Instacart guide, February 2026). In-store-attached native dramatically outperforms web native CTR baselines.

- Native vs banner view frequency: Consumers view native ads 53% more frequently than banner ads, per eMarketer (2026) citing industry research. This is the engagement gap that mis-applied last-click attribution masks.

Conversion benchmarks

- Purchase intent lift: Native content exposure produces an 18% increase in purchase intent versus standard display ads, per eMarketer (January 2026).

- Instacart new-to-brand rate: 45–60% of ad-attributed sales come from new-to-brand customers — a leading conversion-quality signal for shoppable native and sponsored ads on the platform (RMIQ Instacart guide, February 2026).

- Criteo retail-media new-to-brand pattern: Three in five shoppers who click and purchase through a retail media campaign are new to the brand in the Apparel, Arts & Entertainment, and Health & Beauty sectors (Criteo, updated November 2025).

- Caper Cart in-store native: Greater than 3% engagement rate and greater than 2% add-to-cart rate (RMIQ Instacart guide, February 2026). Add-to-cart on a native ad surface materially outpaces standard display benchmarks.

ROAS benchmarks

- Instacart average grocery ROAS: $5.25 returned per $1 spent in H1 2025, per Pacvue data cited in the RMIQ Instacart guide (February 2026).

- Instacart by campaign type: Branded keyword campaigns return 5x–8x+ ROAS; unbranded category campaigns return 2x–4x ROAS (RMIQ, February 2026).

- Criteo Onsite Display (vendor-stated): Up to 100% share of voice, engagement rate up to 1.6%, and ROAS up to 1,360% as a top-end vendor-stated range (Criteo Commerce Yield documentation). Treat the upper bound as best-case, not benchmark.

- Criteo incrementality study: US Sponsored Products delivered +428% incremental return on investment across 27 household brands tested 2021–2023 (Criteo Beyond ROAS); EMEA Onsite Display delivered a 160% increase in sales per user across 1,656 brands (Feb–Dec 2023).

- Offline attribution uplift: Campaigns including offline attribution show an average ROAS increase of 42% versus online-only measurement (Criteo, updated November 2025). For operators monetising omnichannel inventory, this is the gap between reported ROAS and true ROAS.

- Multi-format combination: When onsite display runs alongside sponsored products, the combination drives a 3–4x increase in the number of shoppers who purchase advertised products (Criteo Commerce Yield documentation).

Mobile native performance

Public mobile-native-specific retail-media benchmarks are thin. The directional signal: mobile programmatic native consistently outperforms desktop for in-feed and shoppable units, and TripleLift's eye-tracking research (referenced in industry conference materials) consistently shows scroll-based mobile native formats out-engaging static formats. Operators should benchmark their own mobile vs desktop native CTR and CVR separately rather than relying on industry composites.

Key benchmark table:

| Metric | Native ad benchmark | Source |

|---|---|---|

| Strong native CTR (general) | >0.4% | eMarketer 2026 |

| In-store digital native CTR | ~2.6% (Schnucks Carrot Ads) | RMIQ 2026 |

| In-store native engagement | >3% engagement, >2% add-to-cart (Caper Cart) | RMIQ 2026 |

| Purchase intent lift vs display | +18% | eMarketer 2026 |

| Instacart average ROAS (grocery) | $5.25 (H1 2025) | Pacvue via RMIQ 2026 |

| Branded keyword ROAS (Instacart) | 5x–8x+ | RMIQ 2026 |

| Unbranded category ROAS (Instacart) | 2x–4x | RMIQ 2026 |

| ROAS uplift incl. offline attribution | +42% vs online-only | Criteo 2025 |

| Sponsored Products iROI (US) | +428% (27 brands, 2021–2023) | Criteo 2024–2025 |

| New-to-brand share (Instacart typical) | 45–60% | RMIQ 2026 |

For the broader cross-format ROAS context — sponsored search, sponsored display, video, in-store sponsored — see ROAS Benchmarks by Platform and Ad Format (2026).

Platform Comparison: Native Ad Networks for Retail Media

Six platforms account for the majority of native ad demand flowing into and around retail media in 2026: Criteo (Commerce Max), Outbrain (now operating as Teads after the February 2025 acquisition and June 2025 rebrand), TripleLift, Taboola (Realize), Sharethrough, and Nativo. Each was built for a different demand profile, integrates differently with retail media inventory, and serves a different operator decision.

| Platform | Built for | Retail media integration | Key 2025 update | Pricing model | Operator-fit signal |

|---|---|---|---|---|---|

| Osmos (RMN OS) | Operator infrastructure | Native by design at infrastructure level via Adscape + API Hub | Continuous; 25Bn auction capacity, 15–20ms P95 latency | Operator-set (ownership, not seat-rental) | Best when operator wants to own the native ad stack |

| Criteo Commerce Max | Brand advertiser demand | 200+ retailer onsite network; closed-loop to retailer sales data | Auction-Based Display launched June 2025; Google SA360 integration September 2025 | CPM and CPC, undisclosed minimum | Best when operator integrates as part of Criteo's retailer network |

| Teads (formerly Outbrain) | Open-internet native + branding | Limited closed-loop retail data; product feed/catalog ads for ecommerce native | Merger completed Feb 2025, Teads rebrand June 2025; combined 2.2B consumer reach, $1.7B FY24 ad spend | CPC native; CPM display | Best for offsite native reach beyond the operator's owned audience |

| TripleLift | Creative SSP / programmatic native | Amazon DSP Certified Supply Exchange (Oct 2025); Yahoo DSP retail formats | Retail media grew 110% YoY organically in 2025 | Programmatic CPM | Best when operator integrates an SSP for offsite native demand |

| Taboola Realize | Open-web demand aggregation | Indirect — pivoting from native into broader performance advertising | Realize platform launch Feb 2025; ~600M DAU | CPC | Best for reach-led offsite native acquisition |

| Sharethrough | Programmatic native + attention | No confirmed RMN integrations; GreenPMPs sustainability angle | Top-5 SSP for web in US (Pixalate H2 2024) | Programmatic CPM | Best when sustainability/attention metrics matter to the brand brief |

| Nativo | Content-native storytelling | No explicit RMN integration; acquired by Life360 in November 2025 — direction unclear | Life360 acquisition Nov 2025 | CPM and CPCV | Best for content-led brand storytelling; less so for performance retail native |

Osmos is positioned in the first row because it operates at a different layer than the others: it is the operator-side infrastructure that powers an RMN's own native ad auctions, not a third-party demand network the operator buys into. See the comparison rules below.

Criteo (Commerce Max)

Criteo Commerce Max is the most mature retail-media-native demand platform in the market. It runs onsite display, onsite video, and sponsored products across 200+ global retailers, with closed-loop measurement back to actual transaction data. In June 2025, Criteo launched auction-based display ads, and in September 2025 it became the first onsite retail media partner for Google Search Ads 360. Vendor-stated Onsite Display performance ranges go as high as 1,360% ROAS, 100% share of voice, and 1.6% engagement rate (Criteo Commerce Yield documentation) — treat these as upper bounds, not benchmarks. The verified incremental ROI evidence is stronger: +428% iROI for US Sponsored Products and 160% sales-per-user uplift for EMEA Onsite Display (Criteo Beyond ROAS).

"Display advertising is a proven retail media format, but the needs of advertisers and retailers are evolving."

— Melanie Zimmermann, General Manager of Global Retail Media at Criteo (June 2025)

Criteo vs Outbrain (Teads): Criteo is walled-garden retail-data-led; Teads is open-internet reach-led. Criteo vs Taboola: Criteo offers retailer-data closed loop; Taboola offers larger open-web DAU but no proprietary retail data. Criteo vs TripleLift: Criteo is full-stack demand-side; TripleLift is supply-side creative tech with programmatic native. Criteo vs Nativo/Sharethrough: Criteo is retail-attribution-native; Nativo/Sharethrough are open-web content/attention-native.

Best for: brand advertisers who want retailer-verified attribution at scale. Less suited to operators building their own native ad inventory in-house — Criteo monetises the demand side; operators need infrastructure for the supply side.

Teads (formerly Outbrain)

Outbrain completed its acquisition of Teads on February 3, 2025 and rebranded the combined company to Teads Holding Co. in June 2025. The combined platform reaches 2.2 billion consumers with approximately $1.7 billion in FY24 ad spend, blending Outbrain's mid-to-lower-funnel performance heritage with Teads' upper-funnel video and branding capabilities. Projected merger synergies are $65M–$75M annually by 2026. For retail-media-adjacent native, Teads' relevance is open-internet product feed and catalog-based ads, plus a growing CTV inventory footprint (more than doubled YoY in 2025 across the broader programmatic CTV business). The constraint: open-web focus means no proprietary closed loop to retailer transaction data.

Outbrain (Teads) for retail media: Best as an offsite reach layer for native units extending beyond the operator's owned shopper audience. The platform partners with publishers — not retailers — so closed-loop attribution back to in-cart purchases requires the operator to bridge with first-party data (typically via Events API instrumentation on the operator's own site).

Outbrain vs Taboola: Post-merger Teads operates at materially larger scale (2.2B consumers vs Taboola's ~600M DAU). Taboola is the historical reach leader; Teads is now the reach + branding leader. Both are open-web demand aggregators rather than retail-media-native platforms.

TripleLift

TripleLift is a creative SSP with programmatic native at scale. Its 2025 was a breakout: retail media grew 110% year-over-year organically, demand-driven growth increased 24x, and CTV inventory more than doubled YoY (TripleLift, December 2025). In October 2025, TripleLift joined Amazon's DSP Certified Supply Exchange Program, expanding access for retail media native demand routed through Amazon DSP. TripleLift's value proposition is creative innovation — scroll formats, carousel, cinemagraph — and the supply side of programmatic native, not full RMN infrastructure.

"2025 has been a year of extraordinary momentum for TripleLift, where we've proven that creativity and technology can redefine what's possible in programmatic advertising."

— Dave Helmreich, CEO of TripleLift (December 2025)

The directional signal on creative quality is corroborated by TripleLift's June 2025 retail media survey of 200 US marketing professionals: 82% acknowledged that high-quality creative is essential for KPI outcomes, and 74% reported satisfaction with native ads (the highest of any retail media format, with zero dissatisfaction).

TripleLift vs Sharethrough: Both are programmatic native SSPs. TripleLift's retail media integration is materially deeper (Amazon DSP Certified, Yahoo DSP partnership for SKU-level native, 110% YoY retail media growth). Sharethrough's differentiation is attention metrics and sustainability (GreenPMPs via Scope3) rather than RMN-specific integration. TripleLift vs Nativo: TripleLift has direct Amazon DSP retail integration; Nativo's retail media posture is undefined post-Life360 acquisition.

Best for: brand advertisers buying programmatic native through DSPs. Useful to operators as an SSP integration layer for offsite demand routing.

Sharethrough

Sharethrough is a programmatic native SSP positioned around attention and sustainability rather than retail media specifically. Public documentation does not confirm RMN integrations or retail-media-specific capabilities; the platform's distinct value props are attention-based creative enhancements, GreenPMPs (sustainability product partnership via Scope3, with 15,000+ brands and a 25% carbon reduction claim), and a Top-5 SSP ranking for web in the US (Pixalate H2 2024). Operators evaluating Sharethrough for retail media should treat the fit as indirect — Sharethrough is an open-web programmatic native demand layer, not a retail-media-native platform with closed-loop transaction attribution.

Sharethrough vs Criteo: Different categories. Criteo is retail-data-led demand-side; Sharethrough is open-web supply-side with attention/sustainability differentiation. Sharethrough's retail media specific features: None documented publicly as of 2026. The platform is best evaluated when sustainability commitments or attention metrics are part of the brand brief, rather than as a primary RMN integration.

Taboola (Realize)

Taboola launched its Realize platform on February 26, 2025, positioning the company as a full performance advertising platform — beyond native into outcomes-led demand more directly competitive with search and social. The Realize platform reaches approximately 600 million daily active users across the publisher and OEM network (including device-level placements via Samsung and Xiaomi partnerships).

For retail media specifically, Taboola has historically generated significant ecommerce revenue, and its product feed and commerce-native ads are expanding. The strategic note for operators: Taboola is moving its identity away from "native" toward "performance" — which means its competitive posture against Criteo and Amazon DSP is changing, but its proprietary retail data position remains constrained (no first-party shopper data from retailers).

Taboola vs Outbrain (Teads): Both are open-web demand aggregators. Post-merger Teads operates at materially larger scale (2.2B consumers vs Taboola's 600M DAU). Taboola's Realize bet is on performance-outcome positioning rather than reach leadership. Taboola for retail media native: Best as an offsite native reach layer in performance campaigns; weak as a primary RMN integration.

Nativo (table only)

Nativo built its business on content-native formats — Native Article, Native Video, Native Display, Native Stories — with a publisher-direct, MFA-free supply network. The platform was acquired by Life360 in November 2025, and its retail-media positioning is now uncertain pending Life360's integration strategy. Operators evaluating Nativo for retail media in 2026 should expect a period of strategic ambiguity rather than active RMN feature development. Included here in the comparison table for completeness; not given a dedicated subsection because of acquisition uncertainty.

US Retail Media Network Native Ad Inventory: Amazon, Walmart, Instacart, Target

For US operators, the four reference RMNs concentrate the majority of native ad demand: Amazon and Walmart together absorb over 84% of US retail media budgets, with Amazon alone holding 77.3% of digital retail media ad spending in 2025 (Skai, 2025). The remaining 15.8% is split across Walmart, Instacart, Target Roundel, and 200+ other RMNs.

Amazon (Sponsored Display + DSP native + Fire TV / Alexa native). Amazon's native footprint spans Sponsored Display (off-Amazon native placements driven by Amazon shopper data), DSP native units, and emerging streaming TV native placements. The Amazon Ads Nutrafol case study reports a 58% new-to-brand rate on Fire TV (163% above benchmark) and a $2.97 ROAS (337% improvement over baseline). Amazon's advertising division generated $15.6 billion in Q2 2025, primarily through native sponsored listings — making Amazon's native sponsored listings the largest single native ad surface in retail.

Walmart Connect. Walmart Connect operates onsite sponsored products as the native-adjacent core, with onsite display formats and an expanding offsite (Vizio post-acquisition) native footprint. For operators competing for budget against Walmart Connect, the directional benchmark is that the platform delivers similar onsite native engagement patterns to Amazon but with smaller absolute reach.

Instacart. Instacart is the clearest case of native-by-design retail media. Average grocery ROAS of $5.25 in H1 2025 (Pacvue via RMIQ), branded keyword campaigns at 5x–8x+ ROAS, shoppable display CPM floor of $15, and Caper Cart in-store native engagement above 3%. Instacart CPC for sponsored products ranges $0.50–$1.50 with a $0.15 minimum bid. The platform's Carrot Ads in-store digital network — exemplified by the Schnucks 2.6% CTR pilot — represents the highest CTR-density native surface in retail media as of 2026.

Target Roundel. Target's Roundel monetises onsite sponsored listings and branded content with an evolving offsite native footprint via Roundel Media Studio. Target's emphasis on full-funnel measurement is explicit:

"As retail media becomes full-funnel, proving real business impact while providing flexible, data-driven solutions will drive future investment."

— Mario Watson, Senior Director of Ad Products at Roundel (Target), per Skai's 2025 State of Incrementality in Retail Media

Cross-channel integration. All four RMNs are extending native inventory cross-channel — onsite + offsite + in-store + CTV. Off-site retail media spending is anticipated to grow 2–3x faster than on-site over the next couple of years, and in-store retail media ad spending is projected to triple between 2024–2028. Operators outside the top-4 RMNs need to decide whether they integrate as a node in larger demand networks (Criteo, TripleLift) or build their own native inventory stack — the latter is the Osmos path.

Attribution Modeling for Native Ads: What Works at Overview Depth

Last-click attribution systematically under-credits native ads because native engagement is impression-and-scroll heavy, not click-heavy. The fix is not a single replacement model but a layered measurement stack at the operator level.

Why last-click fails for native. Native units drive purchase intent and assisted conversion before they drive a final click — the eMarketer-cited 18% purchase intent lift shows up as future-search behaviour, organic visits, and direct conversions, not in the click-path of the native ad itself.

View-through and lookback windows. The IAB Europe Commerce (incl. Retail) Media Measurement Standards V2 sets a 30-day lookback window as the default for retail media reporting (with flexible customisable options required), and expands new-to-brand and new-to-category timeframes to five generic timeframes. The standards become enforceable after a six-month grace period through July 2026 — operators not yet aligned should reconcile their attribution windows ahead of that deadline.

Incrementality testing as the primary causal signal. Last-click and view-through are correlational; incrementality testing (matched-market, geo-split, holdout, ghost-bid) is the closest operators get to causal lift. Skai's 2025 incrementality data is sobering: only 56% of marketers report proficiency in measuring retail media incrementality, 44% express accuracy and reliability concerns, and 36% cite difficulty proving incrementality as a top measurement concern (Skai, 2025).

"Incrementality measurement in retail media is broken. Methods used don't capture true causal impact, relying on correlations and proxies instead."

— Jack Lindberg, Head of Product Marketing at Shalion, per Skai 2025 State of Incrementality

"As an industry, we throw around 'Incrementality' constantly, but do we even agree on what it means? We need uniform measurement definitions."

— Mike Black, Chief Growth Officer at Profitero, per Skai 2025 State of Incrementality

For methodology depth — matched-market designs, ghost-bid setup, statistical-significance thresholds for native specifically — see Osmos's incrementality testing in retail media deep-dive and the closed-loop attribution for retail media explainer.

First-party data in native attribution. Retail media is structurally first-party — the operator owns the impression, the click, the cart-add, and the purchase signal. That means native attribution does not have to depend on third-party cookies or external identity graphs; it can run entirely on the operator's own Events API instrumentation. The Osmos API Hub Events API tracks view, click, add-to-cart, and purchase at first-party first principles, which is what enables closed-loop attribution for native units on the operator's own surfaces.

Blended attribution models. For operators with mixed onsite/offsite/in-store native inventory, blended attribution combines last-click for in-session conversions, view-through with a 7- or 30-day window for native-specific lift, and incrementality testing for causal validation. Machine-learning attribution (multi-touch fractional credit assignment trained on the operator's own conversion data) is increasingly viable at scale — but requires hundreds of thousands of conversion events to converge reliably, putting it within reach only for larger RMNs.

MMM as a poor fit. Media Mix Modelling tends to under-fit retail media because the granularity of retail media (SKU-level, basket-level, intra-day) does not match MMM's typical weekly aggregate inputs:

"MMM accurately assesses retail media performance...we have to move past force-fitting retail media into a methodology that isn't fundamentally built to understand it."

— Alex Juday, SVP at Incremental, per Skai 2025 State of Budget Allocation

We cover blended-model setup, ML attribution architecture, and engagement-metric attribution patterns at full tactical depth in our forthcoming native-attribution guide — that piece is the deep-dive companion to this overview.

Budget Allocation Framework: Native Ads Within a Retail Media Mix

Native ads compete for budget against sponsored products, sponsored brands, display, and video within the retail media format mix. Benchmark-level data on how operators and brands actually allocate is patchy but directional.

Format split benchmark (global Amazon data via Nielsen). Sponsored products take 40%, sponsored brands 24%, display (which includes native and display units) 20%, and video 16% of retail media format budgets (Nielsen, 2025). The 20% display-and-native share is the addressable pool for native-specific allocation decisions.

Retail media's share of programmatic.50% of companies allocate over 50% of their digital programmatic budget to retail media — meaning native units inside retail media are competing for a much larger pool than open-web programmatic native.

Off-site vs on-site allocation intent. 51% of marketers plan to boost off-site retail media by reallocating existing budgets, with another 20% adding net-new investment, per the same TripleLift survey (June 2025). 68% agree off-site retail media enables cost-effective scaling. Translated to operator strategy: native ad inventory needs to be configured for both onsite and offsite delivery, with allocation pacing that reflects the off-site growth tilt.

Structural constraint: most marketers do not control their own budget.95% of marketers are not involved in retail media budget decisions — they receive allocated budgets from finance or procurement, often without real-time performance data. 97% of advertisers without real-time performance data say real-time reporting would increase investment. The operator implication: real-time native ad performance reporting is itself a budget-acquisition tool — it changes the conversation between the brand's media-buying team and the operator's revenue team.

KPI hierarchy for native budget decisions. ROAS (in-format and incremental), conversion rate, engagement rate, viewability, and new-to-brand rate together form the canonical native KPI stack. Pure ROAS optimisation undervalues native (because of the engagement-vs-click pattern); blended scoring with incremental ROAS and assisted conversion gives a more honest budget signal.

Platform-specific spend thresholds. Minimum spend on most native demand platforms is not publicly disclosed. Instacart's $15 CPM floor and $0.15 CPC minimum bid are publicly documented (RMIQ, 2026); Criteo, Teads, TripleLift, Taboola, Sharethrough, and Nativo treat minimums as commercial-negotiation terms.

Scaling signals. When native CTR sustainably exceeds the 0.4% eMarketer threshold, when in-session and view-through CVR are both rising on the same inventory, and when blended ROAS (with incrementality) is above the operator's target margin — increase allocation. Operators with mature inventory tend to stabilise native at the 15–25% format share within the broader retail media format mix.

For operators evaluating broader monetisation models around the native budget framework — yield management, fill rate, advertiser segmentation — see Osmos's retail media monetization models guide.

Tactical budget-by-format pacing rules and platform-by-platform allocation patterns are covered in our forthcoming native-attribution guide.

Native Ad ROI: Measurement Framework for Operators

Operator ROI on native ad inventory has three layers: direct ad revenue, advertiser-side performance (which determines whether advertisers re-spend), and the operator's gross margin on the inventory.

Direct ad revenue. Native units priced at CPM or CPC produce immediate ad revenue. The benchmark range cited above ($15 CPM floor for shoppable display on Instacart; $0.50–$1.50 CPC range) anchors the lower bound; programmatic open-web native typically clears below those numbers, while retail-data-targeted native can clear materially higher.

Advertiser-side performance (retention signal). The metrics that determine whether an advertiser continues to invest in the operator's native inventory:

- Conversion rate.eMarketer's 18% purchase intent lift over standard display is the baseline; Instacart's 45–60% new-to-brand share on ad-attributed sales sets the upper-bound conversion signal.

- ROAS. $5.25 average grocery on Instacart (H1 2025) and $2.97 on Amazon's Nutrafol Fire TV case study set published benchmarks; vendor-stated ranges go higher (Criteo Onsite Display up to 1,360%) but should not be quoted as benchmarks.

- Halo effects. Within two weeks of running retail platform advertising, brands report a 59% boost in their organic share of sales on average, and shoppers making ad-prompted purchases continue to buy from the brand five more times over the next six months. Native units contribute disproportionately to this halo because they drive consideration and recall, not just last-click conversion.

- DoorDash AI-optimised native case study. One case study reported by AI Digital cited a 15x conversion rate boost and 50% improvement in cost-per-action efficiency from AI-optimised native creative on DoorDash. Treat as a single-case data point rather than a benchmark.

Operator gross margin. The operator's economic question is the take-rate on native ad spend net of demand-acquisition costs (in the case of Criteo / Teads / TripleLift integrations) versus the infrastructure cost of running native ad serving in-house. Operators owning their native ad stack typically capture materially higher margin per impression — at the cost of building or licensing the infrastructure.

Closed-loop framing.

"Closed-loop attribution links offsite exposures to verifiable online and in-store transactions, providing marketers with accountability."

— AdExchanger / DoorDash Ads content studio, October 2025

The strongest 2025 native ROI evidence is the Proximo Spirits full-funnel case study via DoorDash Ads: 60% new-to-brand sales capture, 200% ROAS, and off-site impression volume 10x higher than on-site (AdExchanger / DoorDash Ads content studio, October 2025) — a directional example, not a portable benchmark.

How Osmos Enables Native Ad Monetization at Scale

Operators face a choice: rent demand from Criteo / Teads / Taboola / TripleLift, or own the infrastructure that lets them run native ad inventory in-house and integrate those networks as supplementary demand. Osmos is the operator-side platform for the second path.

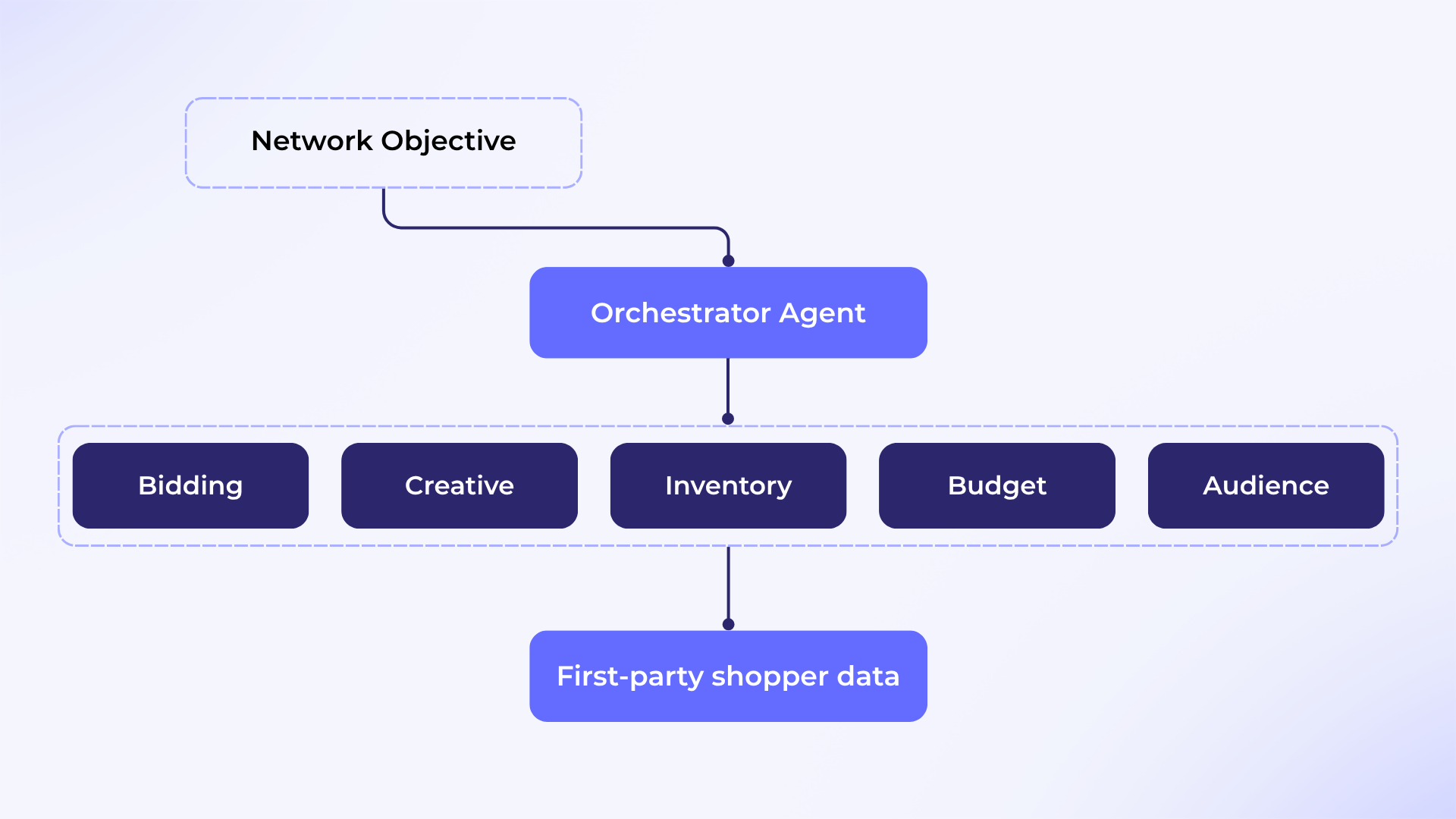

Native ad format configuration (Adscape).Adscape is the format layer: Product Ads, Video Ads, In-store Ads, Offsite Ads, Display Ads, Story Ads, PDA (Product Display Ads), Gamified Ads, Influencer Live, Email Ads, and Carousel Ads — all configurable in a single platform with 1-click campaign launch, contextual targeting, and micro-level yield control. The product-page documented client results: 36% improvement in advertiser retention, 11% increase in yield, and 14% increase in brand wallet share. For operators standing up native inventory across multiple formats simultaneously, Adscape collapses what would otherwise require separate point solutions per format type.

Real-time native ad serving at scale (API Hub). The Osmos API Hub supplies eight APIs covering the full operator stack — Campaigns, Reporting, Ad Servers, Events, Advertiser, Catalog, Billing, and Audience. For native specifically, the Ad Server Auction API handles context-based ad serving (fetch native ad units by category, keyword, page context) at 15–20ms P95 latency, with auction capacity tiers from 2Bn to 250Bn monthly. The Events API tracks view, click, add-to-cart, and purchase as first-party events — which is the foundation of closed-loop native attribution without depending on third-party cookies or identity graphs.

Campaign and budget operations (ControlHub).ControlHub handles the operational layer: Wallet Wise for ad fund management (multiple billing profiles, automatic wallet top-up, advertiser incentive automation, credit lines), Brand Jukebox for advertiser experience management, Content Cop for native creative compliance, and Onboard Pro for advertiser onboarding. The documented results: 32% more campaigns managed per trafficker, 4x increase in revenue per account executive, and 40% improvement in time to completion — directly addressing the TripleLift survey's pain point that 82% of marketers say high-quality creative is essential for KPI outcomes.

Revenue strategy and yield optimisation (StratEdge).StratEdge operates the strategy layer: Pulse Pro for live advertiser and campaign insights and growth-opportunity identification, Demand Wise for advertiser acquisition and retention via drip campaigns and behaviour-based segmentation, Ad Bundles for omnichannel ad packages and event/festival campaign planning, BYOT (Bring Your Own Traffic) for lower-funnel reporting of advertiser-driven traffic and cookie-less traffic tracking, and King Of The Hill for self-serve house-ads management with contextual audience targeting. Documented client results: 38% increase in fill rate, 3x increase in monetisation, 40% improvement in brand adoption.

Where Osmos sits in the comparison. Osmos is not a DSP and not an open-web native network. Criteo, Teads, Taboola, TripleLift, Sharethrough, and Nativo operate at the demand layer — they aggregate and route advertiser spend. Osmos operates at the operator-infrastructure layer — it powers an RMN's own native auction, format configuration, attribution, and yield management. The platforms are complementary, not competitive: an operator using Osmos as infrastructure can integrate Criteo or TripleLift as supplementary offsite demand while keeping native format configuration, attribution, and revenue strategy in-house.

Key Takeaways and Next Steps for Operators

Native ad benchmarks for retail media in 2026 break down to a small set of operator-decision rules:

- Engagement floor: CTR above 0.4% is performing; in-store digital native (Schnucks 2.6%) and shoppable in-cart (Caper Cart >3% engagement) outperform that floor by 5x+.

- Conversion ceiling: 45–60% new-to-brand share on Instacart and 3-in-5 NTB on Criteo's apparel/Arts & Entertainment/health & beauty retail data set the upper bound on what well-targeted native should deliver.

- ROAS range: $2.97 to $5.25 average platform ROAS, with branded keyword campaigns reaching 5x–8x+ and offline-attribution inclusion adding ~42% on top.

- Format mix: Display-and-native is approximately 20% of retail media format budgets per Nielsen's global Amazon data; the addressable native band sits inside that 20%.

- Attribution: Last-click under-credits native. Use blended view-through + incrementality + first-party Events instrumentation. Align lookback windows to the IAB Europe 30-day default ahead of the July 2026 enforcement deadline.

- Platform choice (offsite native demand): Criteo for retailer-closed-loop; Teads for open-web reach + branding; TripleLift for creative SSP + Amazon DSP route; Taboola for performance-reach blend; Sharethrough for attention/sustainability brief; Nativo for content-led storytelling (with acquisition-uncertainty caveat).

- Operator decision: Rent demand from native networks, build native inventory on operator-owned infrastructure (Osmos), or do both. The second and third paths protect operator margin and attribution control.

For deeper context: ROAS Benchmarks by Platform and Ad Format (2026) gives the cross-format baseline this native-specific guide deepens; Sponsored Ad Formats in Retail Media: The Operator's 5-Type Playbook covers the sponsored ad taxonomy this guide intentionally does not re-cover; and retail media monetization models frames the broader revenue strategy that native inventory fits into.

Operators planning to build or scale native ad inventory should evaluate StratEdge for fill-rate and monetisation strategy, Adscape for native format configuration, and ControlHub for campaign and budget operations — the three together cover the full native ad lifecycle on operator-owned infrastructure.

Frequently Asked Questions

What is native advertising in retail media?

Native advertising in retail media is a paid ad format engineered to match the visual design, contextual placement, and editorial behaviour of the retail surface it appears on — including in-feed product cards, shoppable content units, recipe and recommendation modules, in-cart shoppable display, and offsite content-native units that read as part of the shopping or content experience rather than as an interruption.

What CTR should I expect from native ads in retail media?

Per eMarketer (2026), CTR above 0.4% indicates strong native performance. In-store digital native (Schnucks Carrot Ads via RMIQ) reaches approximately 2.6%, and in-cart native (Caper Cart) exceeds 3% engagement — both materially outperform open-web native baselines.

Which native advertising platform is best for retail media operators?

There is no single "best" platform — the right choice depends on the operator's role. For brand advertisers buying into retailer-data-closed-loop inventory, Criteo Commerce Max is the most mature. For open-web reach and branding, Teads (formerly Outbrain post-February 2025 merger) leads at 2.2B consumers. For programmatic native through DSPs, TripleLift offers Amazon DSP Certified routing. For operators building and monetising their own native ad inventory in-house, Osmos provides the operator-infrastructure layer that lets them own format configuration, attribution, and yield — and integrate the demand networks above as supplementary offsite supply.

How do you measure ROI on native advertising in retail media?

Combine three layers: direct ad revenue (CPM/CPC of the native unit), advertiser-side performance (conversion rate, ROAS, NTB share, halo effects on organic sales), and operator gross margin (take-rate net of demand-acquisition cost or infrastructure cost). Criteo's 2024–2025 study shows that campaigns including offline attribution surface 42% more ROAS than online-only measurement — a critical reconciliation step for omnichannel native ROI.

Is Outbrain still operating as Outbrain?

No. Outbrain completed its acquisition of Teads on February 3, 2025 and rebranded the combined company to Teads Holding Co. in June 2025. The combined platform reaches 2.2 billion consumers with approximately $1.7 billion in FY24 ad spend. When evaluating native demand partners in 2026, "Outbrain" and "Teads" refer to the same entity.

Sources

- eMarketer — FAQ on Native Advertising: Formats, AI Opportunities, and the Best Metrics for 2026 (January 2026)

- TripleLift — TripleLift Unveils Key to Retail Media Success: Creative Excellence Drives Performance in $179.5B Market (June 2025)

- Skai — The 2025 State of Incrementality in Retail Media (March 2025, updated December 2025)

- Skai — The 2025 State of Budget Allocation in Retail Media (March 2025, updated December 2025)

- Criteo — Beyond ROAS: A Broader Approach to Measuring Retail Media Success (May 2024, updated November 2025)

- Criteo Commerce Yield Help Center — What is Onsite Display?

- Criteo — Criteo Debuts Auction-Based Display Ads (June 2025)

- TripleLift — TripleLift Closes a Breakthrough 2025 (December 2025)

- Outbrain / Teads — Outbrain Completes the Acquisition of Teads (February 2025)

- Taboola — Taboola Expands Beyond Native Ads with Realize (February 2025)

- RMIQ — Instacart Ads Advertising Guide 2026 (February 2026)

- AI Digital — Native Advertising Guide for Marketers in 2026 (October 2025)

- AdExchanger / DoorDash Ads — The Full-Funnel Retail Media Network (October 2025)

- AdExchanger / T-Mobile — The Retail Media Boom Is About To Shift Gears (March 2025)

- Adtelligent — Retail Media Market Outlook 2026 (January 2026)

- Nielsen — The Future of Retail Media (June 2025)

- IAB Europe — Commerce (incl. Retail) Media Measurement Standards V2 (January 2026)

- Amazon Ads — What is Native Advertising? How It Works, Benefits, Types

- Kevel — Native Advertising: The Definitive Guide (April 2026)

.png)